- Singapore’s weak manufacturing PMI & non-oil domestic exports for April are pointing to a risk of contraction for Q2 GDP growth.

- China’s recent lacklustre key leading macro data and inaction by PBoC may reinforce further contraction of Singapore’s economic growth in H2 2023.

- Singapore’s Straits Times Index’s underperformance against the rest of the world may persist.

More signs are pointing to a potential contraction in Singapore’s economic growth (GDP) in Q2 2023. where several key leading economic indicators have deteriorated further in the month of April.

Manufacturing activities as indicated by the Singapore Institute of Purchasing & Materials Management PMI declined to 49.7 in April from 49.9 in March which recorded a second consecutive month of contraction. In addition, the electronics sector sub-component which represented 47% of Singapore’s industrial output remained in negative territory for the ninth consecutive month at 49.2.

In addition, Singapore’s non-oil domestic exports (NODX) for April recorded a decline of -9.8% year-on-year from -8.3% printed in March and fared worst than consensus estimates of a -9.4% fall. This latest reading on NODX has marked the seventh consecutive month of contraction due to the broad-based decline in sales of both electronics and non-electronic products.

These observations suggest that global economic growth is in a slowdown mode after major developed nations’ central banks embark on a tightening monetary policy stance in the past year that sucked out prior excessive global liquidity conditions.

Weak macro data from China may further reinforce a further economic deterioration in Singapore

Also, China is one of Singapore’s largest trading partners, and recent lacklustre April’s key economic data from China such as manufacturing and services PMIs, retail sales, and industrial production have indicated that the Q1 growth spurt from the “post-Covid zero reopening” episode has dissipated.

To address this ongoing growth slowdown in China that may lead to a deflationary spiral which in turn can potentially trigger an adverse impact on countries that export goods and services to China such as Singapore, the Chinese central bank, PBoC needs to switch away from its current conservative stance to loosen its liquidity tap further to stimulate growth (کلیک اینجا کلیک نمایید to read our previous report, “China equities bulls in need of fresh liquidity”).

PBoC has maintained its status quo on its one-year medium-term lending facility (MLF) rate unchanged at 2.75% unchanged since August 2022 on Monday, 15 May which suggests that PBoC is still adopting a “wait and see” approach on its current targeted momentary policy stance.

The underperformance of the Singapore Straits Times Index may persist

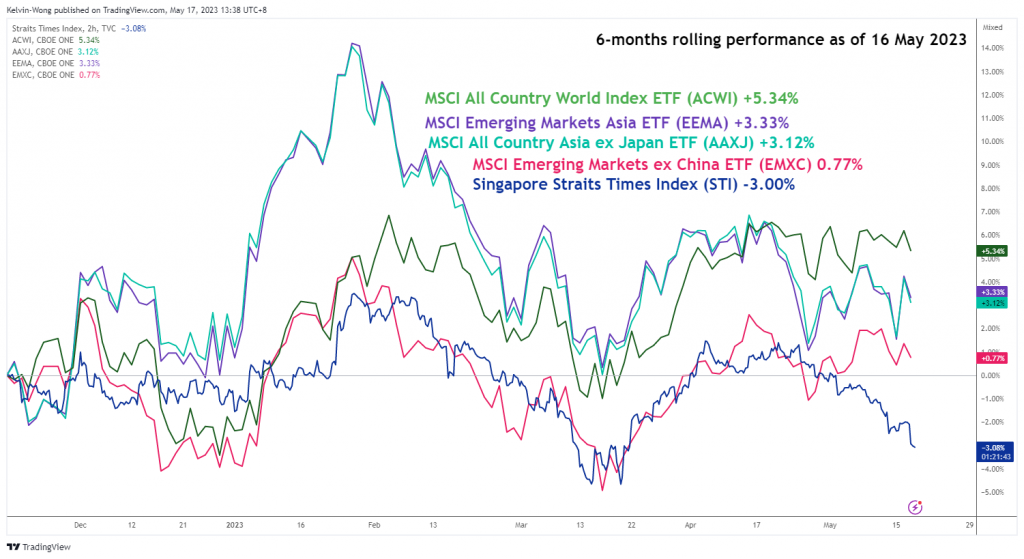

Singapore equities as measured by the benchmark Straits Times Index (STI) have underperformed against the rest of the world, the Asian region, and the regional emerging markets.

For a six-month rolling performance as of 16 May 2023, the STI has recorded a loss of -3.00% versus gains seen in the MSCI All Country World Index (+5.34%), MSCI Emerging Markets Asia (+3.33%), MSCI All Country Asia ex Japan (+3.12%), and MSCI Emerging Markets ex China (+0.77%).

Fig 1: Singapore’s Strait Times Index 6-month rolling performance versus the rest of the world as of 16 May 2023

(منبع: TradingView، برای بزرگنمایی نمودار کلیک کنید)

Hence, if China’s domestic demand continues to falter in the coming months without a more aggressive accommodative monetary policy stance from PBoC, Singapore’s STI may continue to see further potential downside pressure in the second half of 2023.

Based on the lens of technical analysis, the STI has traded below its key 200-day moving average for five consecutive days at this juncture and it is now acting as a resistance at around 3,255 with the intermediate support to watch at 3,090 (the swing low area of 14 March 2023) followed by the major range support of 3,040 in place since 14 May 2021 low.

MSCI Singapore Technical Analysis – Further potential short-term downside pressure below 200-day MA

Fig 2: Singapore 30 trend as of 17 May 2023 (Source: TradingView, click to enlarge chart)

Month-to-date for May 2023, the Singapore 30 Index (a proxy for the MSCI Singapore futures) has recorded a loss of -4.5%, its steepest monthly decline in almost a year. In the long-term, the Index is being trapped within a long-term secular range configuration in place since November 2020 high of 392.35 with a risk of a retest on its long-term secular range support at 270.40 in the coming months based on its current trajectory (see monthly chart).

In the shorter term (see 4-hour chart), the price actions have staged a steep waterfall decline since the bearish breakdown below its key 200-day moving average on Tuesday, 16 May now acting as a resistance at around 295.77.

A minor bounce cannot be ruled out due to such steep downside movement but the minor downtrend phase in place since the 4 April high of 315.06 remains intact reinforced by the bearish conditions seen in the 4-hour MACD trend indicator.

The intermediate support to watch will be at 285.70. However, clearance above the 295.77 key short-term pivotal resistance negates the bearish tone to see the next resistance coming in at 299.40.

محتوا فقط برای اهداف اطلاعات عمومی است. این توصیه سرمایه گذاری یا راه حلی برای خرید یا فروش اوراق بهادار نیست. نظرات نویسندگان هستند. نه لزوما OANDA Business Information & Services, Inc. یا هر یک از شرکت های وابسته، شرکت های تابعه، افسران یا مدیران آن. اگر مایل به بازتولید یا توزیع مجدد هر یک از محتوای موجود در MarketPulse هستید، یک فارکس برنده جایزه، تحلیل کالاها و شاخص های جهانی و سرویس سایت خبری تولید شده توسط OANDA Business Information & Services, Inc.، لطفاً به فید RSS دسترسی داشته باشید یا با ما تماس بگیرید info@marketpulse.com. بازدید https://www.marketpulse.com/ برای کسب اطلاعات بیشتر در مورد ضربان بازارهای جهانی. © 2023 OANDA Business Information & Services Inc.

آخرین پست های کلوین ونگ (دیدن همه)

- محتوای مبتنی بر SEO و توزیع روابط عمومی. امروز تقویت شوید.

- PlatoAiStream. Web3 Data Intelligence دانش تقویت شده دسترسی به اینجا.

- ضرب کردن آینده با آدرین اشلی. دسترسی به اینجا.

- خرید و فروش سهام در شرکت های PRE-IPO با PREIPO®. دسترسی به اینجا.

- منبع: https://www.marketpulse.com/indices/msci-singapore-under-downside-pressure-from-weak-external-demand-china/kwong

- : دارد

- :است

- :نه

- :جایی که

- 1

- 14

- سال 15

- ٪۱۰۰

- 17

- 2020

- 2021

- 2022

- 2023

- 30

- 40

- 49

- 7

- 70

- 77

- 9

- a

- درباره ما

- بالاتر

- دسترسی

- اقدامات

- فعالیت ها

- اضافه

- نشانی

- تصویب

- منفی است

- نصیحت

- وابستگان

- پس از

- در برابر

- مهاجم

- معرفی

- an

- تحلیل

- و

- هر

- روش

- آوریل

- هستند

- محدوده

- دور و بر

- AS

- آسیا

- آسیایی

- At

- اوت

- نویسنده

- نویسندگان

- نماد

- میانگین

- جایزه

- دور

- بانک

- بانک

- مستقر

- BE

- بی تربیت

- بودن

- در زیر

- محک

- هر دو

- گزاف گویی

- جعبه

- تفکیک

- گسترده

- بولز

- کسب و کار

- اما

- خرید

- by

- CAN

- نمی توان

- مرکزی

- بانک مرکزی

- بانک های مرکزی

- چارت سازمانی

- چین

- چیناس

- چینی

- کلیک

- COM

- ترکیب

- آینده

- Commodities

- شرایط

- انجام

- پیکر بندی

- اتصال

- متوالی

- اجماع

- محافظه کار

- تماس

- محتوا

- ادامه دادن

- ادامه

- اختصار

- کشور

- کشور

- دوره

- جاری

- داده ها

- روز

- کاهش

- deflationary

- تقاضا

- توسعه

- مدیران

- داخلی

- نزولی

- دو

- اقتصادی

- رشد اقتصادی

- نشانگرهای اقتصادی

- الکترونیک

- الیوت

- سوار شدن

- سنگ سنباده

- بازارهای در حال ظهور

- بزرگنمایی کنید

- قسمت

- جمع حقوق صاحبان سهام

- تخمین می زند

- اتر (ETH)

- تبادل

- تجربه

- کارشناس

- صادرات

- صادرات

- خارجی

- امکان

- سقوط

- مالی

- پیدا کردن

- جریان

- به دنبال

- برای

- خارجی

- ارز خارجی

- فارکس

- یافت

- تازه

- از جانب

- صندوق

- اساسی

- بیشتر

- آینده

- عایدات

- GDP

- رشد تولید ناخالص ملی

- سوالات عمومی

- جهانی

- اقتصاد جهانی

- بازارهای جهانی

- مغازه

- رشد

- نیم

- آیا

- زیاد

- اما

- HTTPS

- if

- تأثیر

- in

- بی عملی

- شرکت

- شاخص

- نشان داد

- شاخص

- شاخص ها

- Indices

- صنعتی

- تولید صنعتی

- اطلاعات

- موسسه

- حد واسط

- سرمایه گذاری

- IT

- ITS

- ژاپن

- کلوین

- کلید

- بزرگترین

- نام

- آخرین

- رهبری

- برجسته

- امانت دادن

- عدسی

- سطح

- پسندیدن

- نقدینگی

- دراز مدت

- خاموش

- کم

- MACD

- درشت دستور

- عمده

- مدیریت

- تولید

- مارس

- علامت گذاری شده

- بازار

- چشم انداز بازار

- تحقیقات بازار

- MarketPulse

- بازارها

- مصالح

- حداکثر عرض

- ممکن است..

- خردسال

- MLF

- حالت

- دوشنبه

- پولی

- سیاست های پولی

- ماه

- ماهیانه

- ماه

- بیش

- جنبش

- متحرک

- میانگین متحرک

- MSCI

- لزوما

- نیاز

- نیازهای

- منفی

- قلمرو منفی

- اخبار

- بعد

- نوامبر

- اکنون

- متعدد

- of

- مامورین

- on

- ONE

- مداوم

- فقط

- دیدگاه ها

- or

- ما

- خارج

- چشم انداز

- تولید

- روی

- شرکای

- احساساتی

- گذشته

- PBOC

- کارایی

- دیدگاه

- فاز

- محوری

- محل

- افلاطون

- هوش داده افلاطون

- PlatoData

- لطفا

- بعد از ظهر

- سیاست

- تثبیت موقعیت

- پست ها

- پتانسیل

- بالقوه

- فشار

- قبلی

- قیمت

- قبلا

- ساخته

- تولید

- محصولات

- ارائه

- پروکسی

- خرید

- اهداف

- Q1

- Q2

- محدوده

- نرخ

- خواندن

- مطالعه

- اخیر

- ثبت

- منطقه

- منطقهای

- تقویت کردن

- باقی مانده است

- بقایای

- گزارش

- نمایندگی

- تحقیق

- مقاومت

- REST

- خرده فروشی

- خرده فروشی

- برگشت

- خطر

- نورد

- RSS

- حکومت

- حراجی

- دوم

- بخش

- اوراق بهادار

- دیدن

- مشاهده گردید

- فروش

- ارشد

- سرویس

- خدمات

- چند

- اشتراک

- کوتاه مدت

- نشانه ها

- پس از

- سنگاپور

- سنگاپور

- سایت

- کاهش سرعت

- راه حل

- منبع

- متخصص

- وضعیت

- هنوز

- موجودی

- بازار سهام

- رزمارا

- چنین

- نشان می دهد

- حاکی از

- پشتیبانی

- تاب خوردن

- گزینه

- شیر

- هدف قرار

- فنی

- تجزیه و تحلیل فنی

- ده

- مدت

- قلمرو

- نسبت به

- که

- La

- جهان

- این

- هزاران نفر

- سفت شدن

- بار

- به

- TONE

- داد و ستد

- معامله گران

- تجارت

- TradingView

- آموزش

- مسیر

- روند

- ماشه

- سه شنبه

- دور زدن

- زیر

- منحصر به فرد

- us

- با استفاده از

- v1

- در مقابل

- بازدید

- تماشا کردن

- موج

- خوب

- که

- اراده

- برنده

- با

- در داخل

- بدون

- وانگ

- جهان

- بدترین

- خواهد بود

- سال

- سال

- شما

- زفیرنت

- صفر