- Singapore’s weak manufacturing PMI & non-oil domestic exports for April are pointing to a risk of contraction for Q2 GDP growth.

- China’s recent lacklustre key leading macro data and inaction by PBoC may reinforce further contraction of Singapore’s economic growth in H2 2023.

- Singapore’s Straits Times Index’s underperformance against the rest of the world may persist.

More signs are pointing to a potential contraction in Singapore’s economic growth (GDP) in Q2 2023. where several key leading economic indicators have deteriorated further in the month of April.

Manufacturing activities as indicated by the Singapore Institute of Purchasing & Materials Management PMI declined to 49.7 in April from 49.9 in March which recorded a second consecutive month of contraction. In addition, the electronics sector sub-component which represented 47% of Singapore’s industrial output remained in negative territory for the ninth consecutive month at 49.2.

In addition, Singapore’s non-oil domestic exports (NODX) for April recorded a decline of -9.8% year-on-year from -8.3% printed in March and fared worst than consensus estimates of a -9.4% fall. This latest reading on NODX has marked the seventh consecutive month of contraction due to the broad-based decline in sales of both electronics and non-electronic products.

These observations suggest that global economic growth is in a slowdown mode after major developed nations’ central banks embark on a tightening monetary policy stance in the past year that sucked out prior excessive global liquidity conditions.

Weak macro data from China may further reinforce a further economic deterioration in Singapore

Also, China is one of Singapore’s largest trading partners, and recent lacklustre April’s key economic data from China such as manufacturing and services PMIs, retail sales, and industrial production have indicated that the Q1 growth spurt from the “post-Covid zero reopening” episode has dissipated.

To address this ongoing growth slowdown in China that may lead to a deflationary spiral which in turn can potentially trigger an adverse impact on countries that export goods and services to China such as Singapore, the Chinese central bank, PBoC needs to switch away from its current conservative stance to loosen its liquidity tap further to stimulate growth (Klik di sini to read our previous report, “China equities bulls in need of fresh liquidity”).

PBoC has maintained its status quo on its one-year medium-term lending facility (MLF) rate unchanged at 2.75% unchanged since August 2022 on Monday, 15 May which suggests that PBoC is still adopting a “wait and see” approach on its current targeted momentary policy stance.

The underperformance of the Singapore Straits Times Index may persist

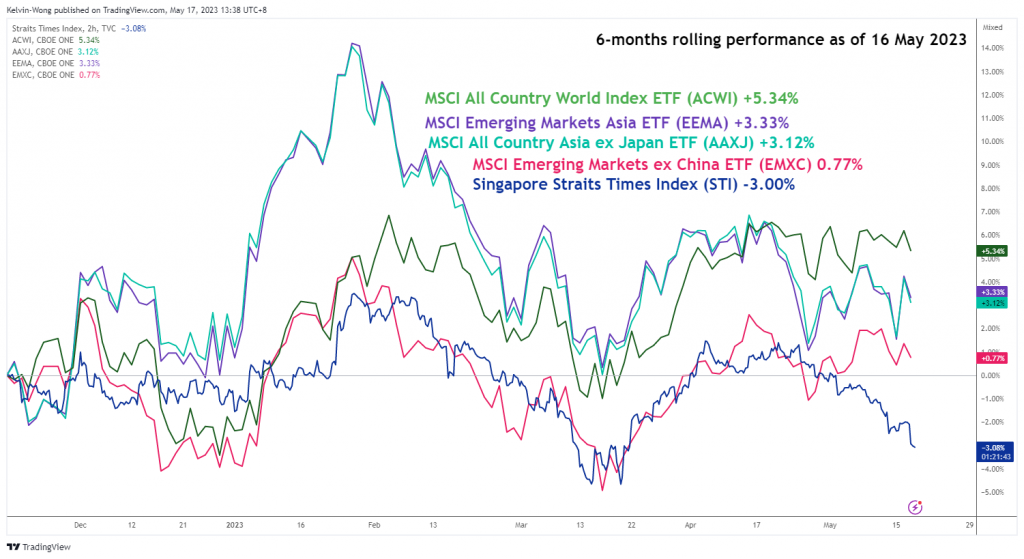

Singapore equities as measured by the benchmark Straits Times Index (STI) have underperformed against the rest of the world, the Asian region, and the regional emerging markets.

For a six-month rolling performance as of 16 May 2023, the STI has recorded a loss of -3.00% versus gains seen in the MSCI All Country World Index (+5.34%), MSCI Emerging Markets Asia (+3.33%), MSCI All Country Asia ex Japan (+3.12%), and MSCI Emerging Markets ex China (+0.77%).

Fig 1: Singapore’s Strait Times Index 6-month rolling performance versus the rest of the world as of 16 May 2023

(Sumber: TradingView, klik untuk memperbesar grafik)

Hence, if China’s domestic demand continues to falter in the coming months without a more aggressive accommodative monetary policy stance from PBoC, Singapore’s STI may continue to see further potential downside pressure in the second half of 2023.

Based on the lens of technical analysis, the STI has traded below its key 200-day moving average for five consecutive days at this juncture and it is now acting as a resistance at around 3,255 with the intermediate support to watch at 3,090 (the swing low area of 14 March 2023) followed by the major range support of 3,040 in place since 14 May 2021 low.

MSCI Singapore Technical Analysis – Further potential short-term downside pressure below 200-day MA

Fig 2: Singapore 30 trend as of 17 May 2023 (Source: TradingView, click to enlarge chart)

Month-to-date for May 2023, the Singapura 30 Indeks (a proxy for the MSCI Singapore futures) has recorded a loss of -4.5%, its steepest monthly decline in almost a year. In the long-term, the Index is being trapped within a long-term secular range configuration in place since November 2020 high of 392.35 with a risk of a retest on its long-term secular range support at 270.40 in the coming months based on its current trajectory (see monthly chart).

In the shorter term (see 4-hour chart), the price actions have staged a steep waterfall decline since the bearish breakdown below its key 200-day moving average on Tuesday, 16 May now acting as a resistance at around 295.77.

A minor bounce cannot be ruled out due to such steep downside movement but the minor downtrend phase in place since the 4 April high of 315.06 remains intact reinforced by the bearish conditions seen in the 4-hour MACD trend indicator.

The intermediate support to watch will be at 285.70. However, clearance above the 295.77 key short-term pivotal resistance negates the bearish tone to see the next resistance coming in at 299.40.

Konten hanya untuk tujuan informasi umum. Ini bukan nasihat investasi atau solusi untuk membeli atau menjual sekuritas. Pendapat adalah penulis; tidak harus milik OANDA Business Information & Services, Inc. atau afiliasi, anak perusahaan, pejabat, atau direkturnya. Jika Anda ingin mereproduksi atau mendistribusikan ulang konten apa pun yang ditemukan di MarketPulse, analisis indeks valas, komoditas, dan global pemenang penghargaan, serta layanan situs berita yang diproduksi oleh OANDA Business Information & Services, Inc., silakan akses umpan RSS atau hubungi kami di info@marketpulse.com. Mengunjungi https://www.marketpulse.com/ untuk mengetahui lebih lanjut tentang ketukan pasar global. © 2023 OANDA Informasi & Layanan Bisnis Inc.

Posting terbaru oleh Kelvin Wong (melihat semua)

- Konten Bertenaga SEO & Distribusi PR. Dapatkan Amplifikasi Hari Ini.

- PlatoAiStream. Kecerdasan Data Web3. Pengetahuan Diperkuat. Akses Di Sini.

- Mencetak Masa Depan bersama Adryenn Ashley. Akses Di Sini.

- Beli dan Jual Saham di Perusahaan PRE-IPO dengan PREIPO®. Akses Di Sini.

- Sumber: https://www.marketpulse.com/indices/msci-singapore-under-downside-pressure-from-weak-external-demand-china/kwong

- :memiliki

- :adalah

- :bukan

- :Di mana

- 1

- 14

- 15 tahun

- 15%

- 17

- 2020

- 2021

- 2022

- 2023

- 30

- 40

- 49

- 7

- 70

- 77

- 9

- a

- Tentang Kami

- atas

- mengakses

- tindakan

- kegiatan

- tambahan

- alamat

- Mengadopsi

- merugikan

- nasihat

- Afiliasi

- Setelah

- terhadap

- agresif

- Semua

- an

- analisis

- dan

- Apa pun

- pendekatan

- April

- ADALAH

- DAERAH

- sekitar

- AS

- Asia

- Asia

- At

- Agustus

- penulis

- penulis

- avatar

- rata-rata

- hadiah

- jauh

- Bank

- Bank

- berdasarkan

- BE

- kasar

- makhluk

- di bawah

- patokan

- kedua

- Melambung

- Kotak

- Kerusakan

- berbasis luas

- Bulls

- bisnis

- tapi

- membeli

- by

- CAN

- tidak bisa

- pusat

- Bank Sentral

- Central Bank

- Grafik

- Tiongkok

- Mandarin

- Cina

- Klik

- COM

- kombinasi

- kedatangan

- Komoditas

- Kondisi

- dilakukan

- konfigurasi

- Menghubungkan

- berturut-turut

- Konsensus

- konservatif

- kontak

- Konten

- terus

- terus

- kontraksi

- negara

- negara

- Pelatihan

- terbaru

- data

- Hari

- Tolak

- deflasi

- Permintaan

- dikembangkan

- Direksi

- Domestik

- Kelemahan

- dua

- Ekonomis

- Pertumbuhan ekonomi

- indikator ekonomi

- Elektronik

- Elliott

- memulai

- muncul

- pasar negara berkembang

- memperbesar

- episode

- Ekuitas

- perkiraan

- Eter (ETH)

- Pasar Valas

- pengalaman

- ahli

- ekspor

- ekspor

- luar

- Fasilitas

- Jatuh

- keuangan

- Menemukan

- aliran

- diikuti

- Untuk

- asing

- devisa

- forex

- ditemukan

- segar

- dari

- dana

- mendasar

- lebih lanjut

- Futures

- Keuntungan

- PDB

- pertumbuhan GDP

- Umum

- Aksi

- Ekonomi Global

- pasar global

- barang

- Pertumbuhan

- Setengah

- Memiliki

- High

- Namun

- HTTPS

- if

- Dampak

- in

- kelambanan

- Inc

- indeks

- menunjukkan

- Indikator

- indikator

- Indeks

- industri

- Produksi Industri

- informasi

- Lembaga

- Menengah

- investasi

- IT

- NYA

- Jepang

- Kelvin

- kunci

- terbesar

- Terakhir

- Terbaru

- memimpin

- terkemuka

- pinjaman

- lensa

- adalah ide yang bagus

- 'like'

- Likuiditas

- jangka panjang

- lepas

- Rendah

- MACD

- Makro

- utama

- pengelolaan

- pabrik

- March

- ditandai

- Pasar

- prospek pasar

- riset pasar

- MarketPulse

- pasar

- bahan

- max-width

- Mungkin..

- minor

- MLF

- mode

- Senin

- Moneter

- Kebijakan moneter

- Bulan

- bulanan

- bulan

- lebih

- gerakan

- bergerak

- moving average

- MSCI

- perlu

- Perlu

- kebutuhan

- negatif

- wilayah negatif

- berita

- berikutnya

- November

- sekarang

- banyak sekali

- of

- petugas

- on

- ONE

- terus-menerus

- hanya

- Pendapat

- or

- kami

- di luar

- Outlook

- keluaran

- lebih

- rekan

- bergairah

- lalu

- PBOC

- prestasi

- perspektif

- tahap

- sangat penting

- Tempat

- plato

- Kecerdasan Data Plato

- Data Plato

- silahkan

- pmi

- kebijaksanaan

- posisi

- Posts

- potensi

- berpotensi

- tekanan

- sebelumnya

- harga pompa cor beton mini

- Sebelumnya

- Diproduksi

- Produksi

- Produk

- menyediakan

- wakil

- pembelian

- tujuan

- Q1

- Q2

- jarak

- Penilaian

- Baca

- Bacaan

- baru

- tercatat

- wilayah

- daerah

- memperkuat

- tetap

- sisa

- melaporkan

- diwakili

- penelitian

- Perlawanan

- ISTIRAHAT

- eceran

- Penjualan Ritel

- Pembalikan

- Risiko

- bergulir

- rss

- Diperintah

- penjualan

- Kedua

- sektor

- Surat-surat berharga

- melihat

- terlihat

- menjual

- senior

- layanan

- Layanan

- beberapa

- berbagi

- jangka pendek

- Tanda

- sejak

- Singapura

- Singapura

- situs web

- Pelan - pelan

- larutan

- sumber

- mengkhususkan diri

- Status

- Masih

- saham

- Pasar saham

- Penyiasat

- seperti itu

- menyarankan

- Menyarankan

- mendukung

- Ayunan

- Beralih

- Tap

- ditargetkan

- Teknis

- Technical Analysis

- sepuluh

- istilah

- wilayah

- dari

- bahwa

- Grafik

- Dunia

- ini

- ribuan

- pengetatan

- kali

- untuk

- NADA

- diperdagangkan

- pedagang

- Trading

- TradingView

- Pelatihan

- lintasan

- kecenderungan

- memicu

- Selasa

- MENGHIDUPKAN

- bawah

- unik

- us

- menggunakan

- v1

- Lawan

- Mengunjungi

- Menonton

- Gelombang

- BAIK

- yang

- akan

- kemenangan

- dengan

- dalam

- tanpa

- wong

- dunia

- terburuk

- akan

- tahun

- tahun

- kamu

- zephyrnet.dll

- nol