Many were shocked by the Fed’s hawkish reversal (which was misconstrued on Thursday as dovish so Powell unleashed the Powell to make it abundantly clear just what the Fed’s thoughts on inflation are), but not BofA’s CIO Michael Hartnett who had long been warning that the Fed risks not only being behind the curve but losing control of inflation altogether if it did or said nothing on Wednesday, and so he was entitled a victory lap of sorts in his latest Flow Show report, in which he writes that just as “BofA FMS investors were bullishly positioned for permanent growth, transitory inflation, peaceful Fed via longs in commodities, cyclicals & financials into June FOMC” when the Fed pulled the rug from under them.

In Hartnett’s post-mortem, the BofA strategist writes that the Fed “flipped from dovish to hawkish” conceding what should be obvious to anyone with a somewhat functioning brain, that zero rates and $4BN of asset purchases every day are incompatible with

a. stocks/bonds/housing prices at all-time highs,

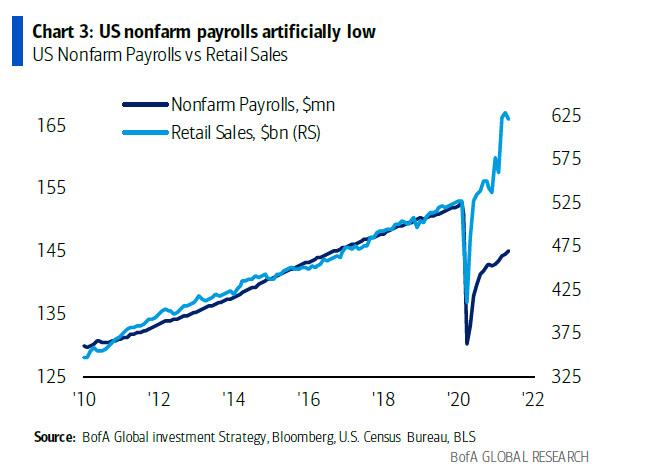

b. GDP +15%, retail sales +40%, payrolls artificially low (Chart 3), CPI annualizing 8%, and…

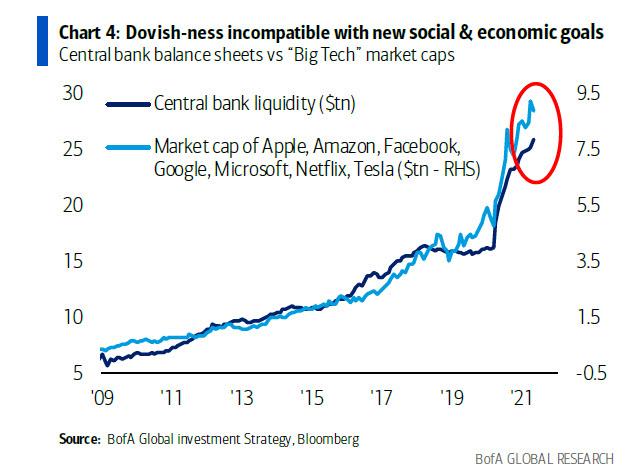

c. the new “social & economic” goal of reducing inequality (see Fed balance sheet & market cap of Big Tech).

The Fed’s hawkish capitulation, also means that what until now had been an “easy Fed” = “easy trade” and a “good news = good news” market in H1, as the shift from global QE to QT accelerates in H2, QE from the big 4 (Fed, ECB, BoJ, BOE) is set to fall $8.5tn in ‘20 to $3.4tn in ‘21 to $0.3tn in ’22.

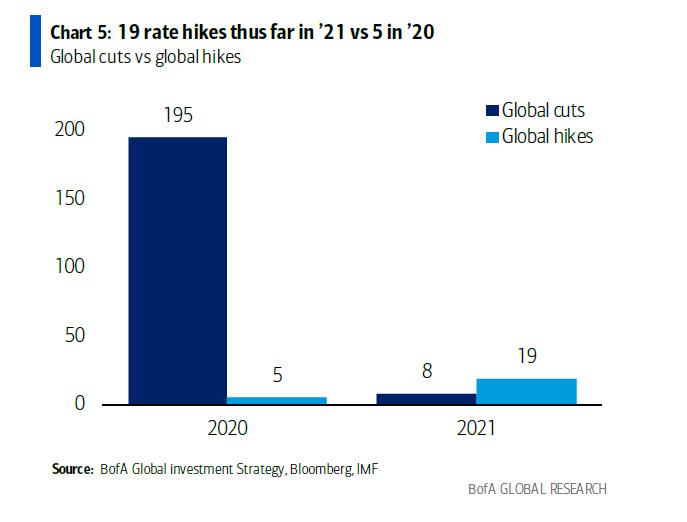

Amid this rapid slowdown in QE, we are also seeing a sharp tightening in financial conditions on the rate side with 19 rate hikes thus far in ’21 vs 5 in ’20 (8 rate cuts vs 195 last year)…

… so in H2 the market will be a nightmare for most traders, as “good news = tighter liquidity = bad news”…low/negative stock/credit H2 returns.

There’s more: not only will good news be bad news, but bad news will also be bad news, as Hartnett explains:

“peak profits” means bad news won’t translate into good news; BofA Global EPS model says global EPS peak was ≈ 40% in April (model driven by China FCI, Asia exports, global PMI, US yield curve – Chart 6), projected to decelerate to 20% by August.

But if only we had signs… Well – we did: one month ago we wrote that China’s Credit Impulse Just Turned Negative, Unleashing Global Deflationary Shockwave. Well, with the usual 1 month delay, it has now arrived much to the “shock” of everyone. Here is Hartnett explaining why China is always the tell:

China the tell: lead indicator for virus, lockdown, reopening, tech boom, tapering, tightening, and in H1…China economy has slowed (Chart 7), stocks flat, defensives (healthcare/telcos) have outperformed, banks flat, consumer/tech down hard (though have caught recent bid – big reason EM acting so well thus far despite US$ up); we say global defensives outperform H2 (staples, pharma, telco, utilities).

But if global defensives are set to outperform, well then cyclicals are in trouble, or as Hartnett puts it, “a Perfect storm for cyclicals” due to…

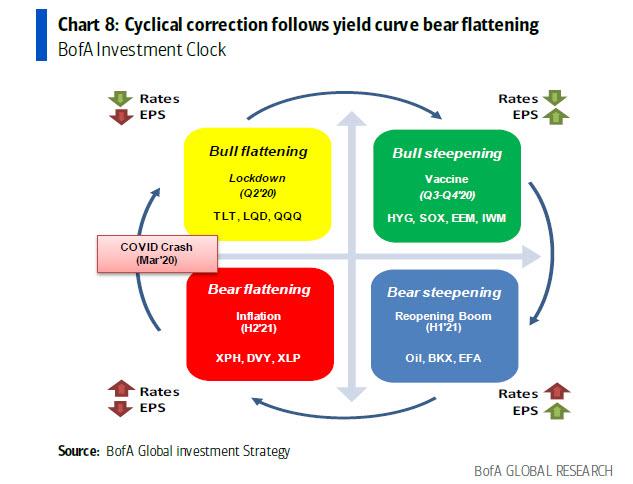

excess positioning, China tightening, US fiscal hopes fading, and now hawkish Fed; note cyclical correction now well underway (homebuilders -14%, copper -13%, materials -9%, transportation -7%…even AUD now bid on spectacular strong labor market data) which follows yield curve bear flattening prediction in BofA Investment Clock view…

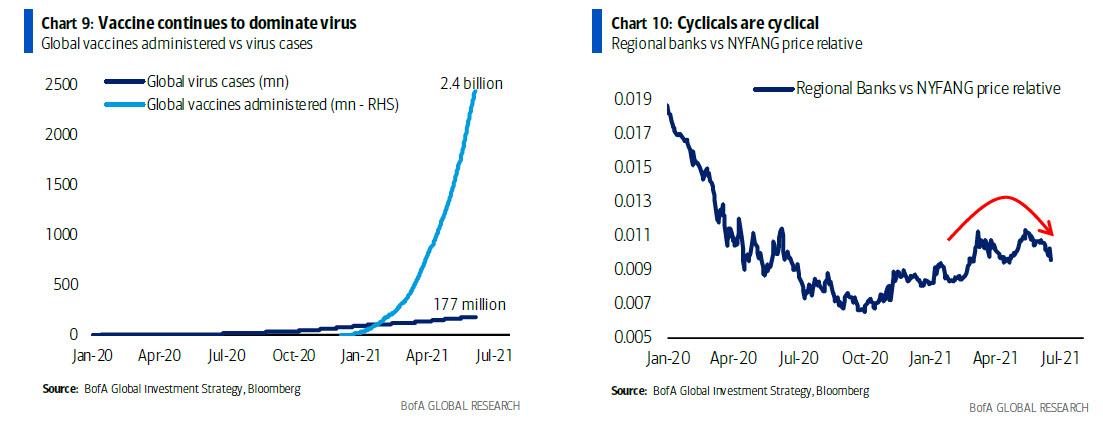

… vaccine continues to dominate virus (Chart 9) but cyclicals are cyclical, Chart 10, and Q3 correction likely (and perhaps necessary to test that secular inflation trade uptrend is for real).

Finally, is a market correction imminent?

Here Hartnett concludes, a minority “correction crew” say weaker internals always herald weaker index, and yet while it is unlikely to have a correction without IG bonds & tech (majority believe both will be bid), Hartnett says that SPW (equal-weighted S&P) & NYA (NYSE Composite) most important levels to watch coming weeks and lists 4 conditions that would suggest an imminent market breakdown:

- SPW breaks below 6000,

- NYA below 16000,

- CCMP fails to break above 14200 (3rd attempt this year),

- weaker internals will signal broader sell-off in credit & stocks in Q3.

- &

- 11

- 7

- 9

- April

- asia

- asset

- Banks

- big tech

- Bonds

- boom

- caught

- China

- CIO

- coming

- Commodities

- continues

- credit

- curve

- data

- day

- delay

- DID

- driven

- ECB

- Economic

- economy

- exports

- Fed

- Finally

- financial

- financials

- flow

- GDP

- Global

- good

- Growth

- here

- HTTPS

- image

- index

- Inequality

- inflation

- investment

- Investors

- IT

- labor

- latest

- Liquidity

- Lists

- lockdown

- Long

- Majority

- Market

- Market Cap

- materials

- minority

- model

- news

- NYSE

- Pharma

- prediction

- purchases

- Rates

- reduce

- report

- retail

- returns

- sales

- set

- shift

- shocked

- Signs

- So

- Social

- Stocks

- Storm

- tech

- Telco

- test

- trade

- Traders

- transportation

- us

- utilities

- View

- virus

- Watch

- WHO

- year

- Yield

- zero