So at $3.1 Billion in ARR, Snowflake finally feels a bit … human. Like a truly epic, incredible, generational tech leader. But perhaps, no longer like it’s from another planet altogether 🙂

After years of metrics (170%+ NRR) and growth like we’ve never seen before, it hasn’t been immune from macro slowdowns, and now is growing 32% at $3.1 Billion in ARR.

That’s still incredible. It still means adding +$1B in new ARR a year! But growth is starting to normalize at scale. For the first time ever.

5 Interesting Learnings:

#1. NRR Remains World Class at 131%, But Down From the Jaw-Dropping 170% at Its Peak

High NRR really can last forever. 131% NRR is still incredible. But it’s way down from the physics-defying 160%-170% it saw for years. In fact, the decline in NRR itself is responsible for the decline in revenue growth from jaw-dropping to merely very, very good.

#2. Insanely Efficient Now. 29% Free Cash Flow Margins.

Snowflake was efficient before, but it’s gotten even more so. Free cash flow has grown from 12% of revenue in 2022 to 29% (!) today. Key to this is holding the line on Sales & Marketing, which has declined substantially as a percent of revenue. Commissions in particular are down.

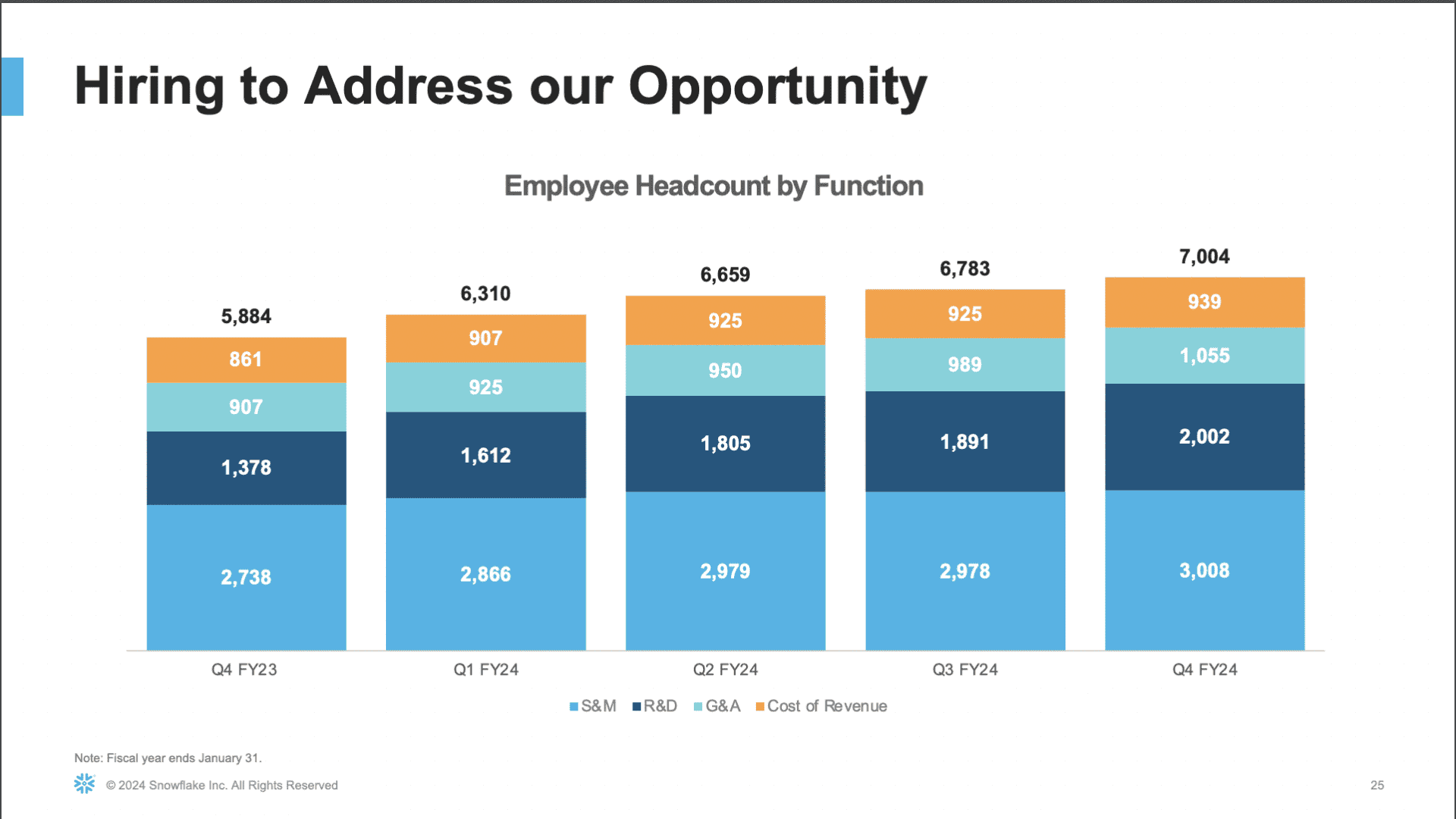

#3. Adding Headcount, Just More Slowly Than Revenue Growth

This is the story at many Cloud and SaaS leaders today and key to getting more effiicient. Snowflake grew headcount +19% the last year, from 5,884 to 7,004. But it grew revenue +32% at the same time. Put differently, it’s growing headcount and thus headcount expense 60% as fast as revenue. A healthy ratio at scale.

#4. $1M+ Customers Growing the Fastest, at +39% a Year

The story again at so many Cloud and SaaS leaders today. The biggest customers are growing the fastest, and the most immune to some of the higher churn and other issues with smaller tech customers. They now have 461 $1M+ customers, and 691 Global 2000 customers. That’s very enterprise.

#5. NPS of 67. Pretty solid!

Can NPS be gamed? Sure. Is it a formal, GAAP metric? Of course not. But 67 is still a high bar. Well done, Snowflake.

Snowflake is still growing like a week, wtih NRR and NPS metrics we’d all die for. It’s an epic story and an epic platform.

It’s just in 2024, it’s finally a bit … human. It finally got a bit hard. Snowflake became a normal Top .01%, Very Very Incredibly Great, Tech Company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.saastr.com/5-interesting-learnings-from-snowflake-at-3-billion-in-arr/

- :has

- :is

- :not

- $3

- 05

- 09

- 1

- 11

- 14

- 17

- 2000

- 2022

- 2024

- 5

- 67

- 7

- a

- adding

- again

- All

- altogether

- an

- and

- Another

- ARE

- AS

- At

- bar

- BE

- became

- been

- before

- Biggest

- Billion

- Bit

- but

- CAN

- Cash

- cash flow

- class

- Cloud

- commissions

- company

- content

- course

- Customers

- data

- Decline

- Die

- differently

- done

- down

- efficient

- embedded

- Enterprise

- EPIC

- Ether (ETH)

- Even

- EVER

- expense

- fact

- FAST

- fastest

- feels

- Finally

- First

- first time

- flow

- For

- forever

- formal

- Free

- from

- GAAP

- generational

- getting

- Global

- good

- got

- great

- grew

- Growing

- grown

- Growth

- Hard

- Have

- headcount

- healthy

- High

- higher

- holding

- HTTPS

- human

- immune

- in

- incredible

- incredibly

- interesting

- issues

- IT

- ITS

- itself

- jpeg

- just

- Key

- Last

- Last Year

- leader

- leaders

- like

- Line

- longer

- Macro

- many

- margins

- Marketing

- max-width

- means

- merely

- metric

- Metrics

- more

- most

- never

- New

- no

- normal

- now

- of

- on

- Other

- particular

- percent

- perhaps

- planet

- platform

- plato

- Plato Data Intelligence

- PlatoData

- pretty

- put

- ratio

- really

- remains

- responsible

- revenue

- revenue growth

- SaaS

- sales

- Sales & Marketing

- same

- saw

- Scale

- seen

- slowdowns

- Slowly

- smaller

- So

- some

- Starting

- Still

- Story

- substantially

- sure

- tech

- Tech Company

- than

- The

- they

- this

- Thus

- time

- to

- today

- top

- true

- truly

- very

- was

- Way..

- week

- WELL

- which

- with

- world

- year

- years

- youtube

- zephyrnet