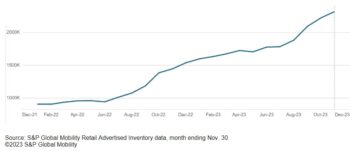

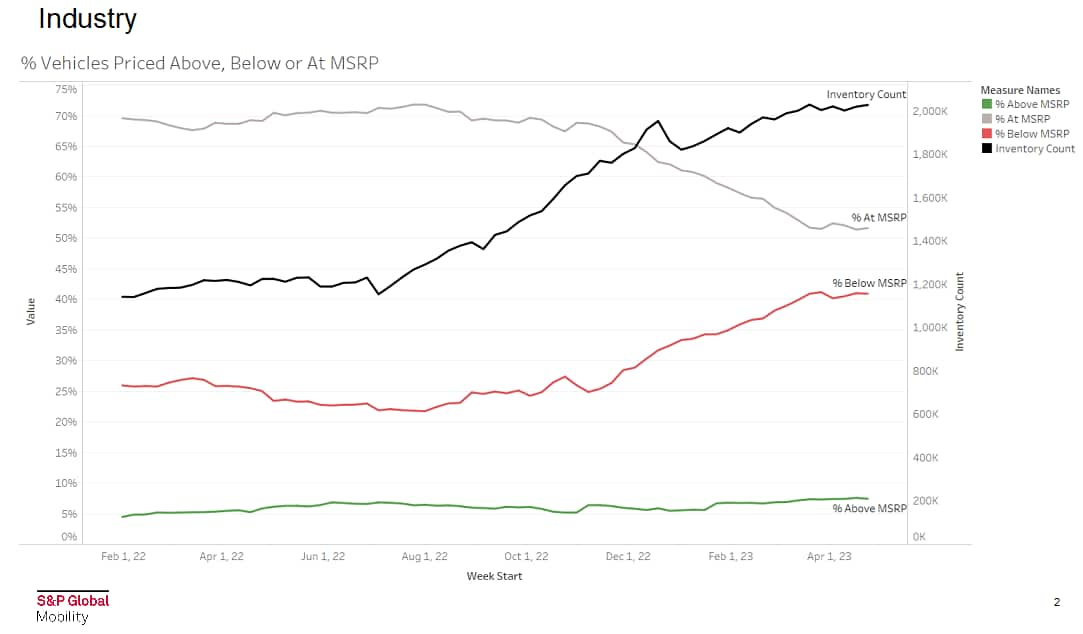

Retail advertised inventory – the availability of vehicles as

communicated by dealerships across the country – has been on the

rise from July 2022 until mid-March 2023. However, based on

month-end April data, S&P Global Mobility’s Advertised Dealer

Inventory analysis shows that inventory recovery will remain

erratic and spiky for the near term, depending on the brand and

segment.

The key takeaway on the new-vehicle purchase front for

consumers: The percentage of vehicles offered below MSRP has risen

as advertised inventory count increased. Meanwhile, the percentage

offered at sticker price has fallen and the percentage offered

above MSRP has remained basically stable.

The pace of advertised inventory growth of domestic brands is

slowing. Domestic advertised inventory rose by single digits (on an

annualized basis) in the last month, and growth slowed through the

quarter. By comparison, it grew by 25% in the last six months

overall.

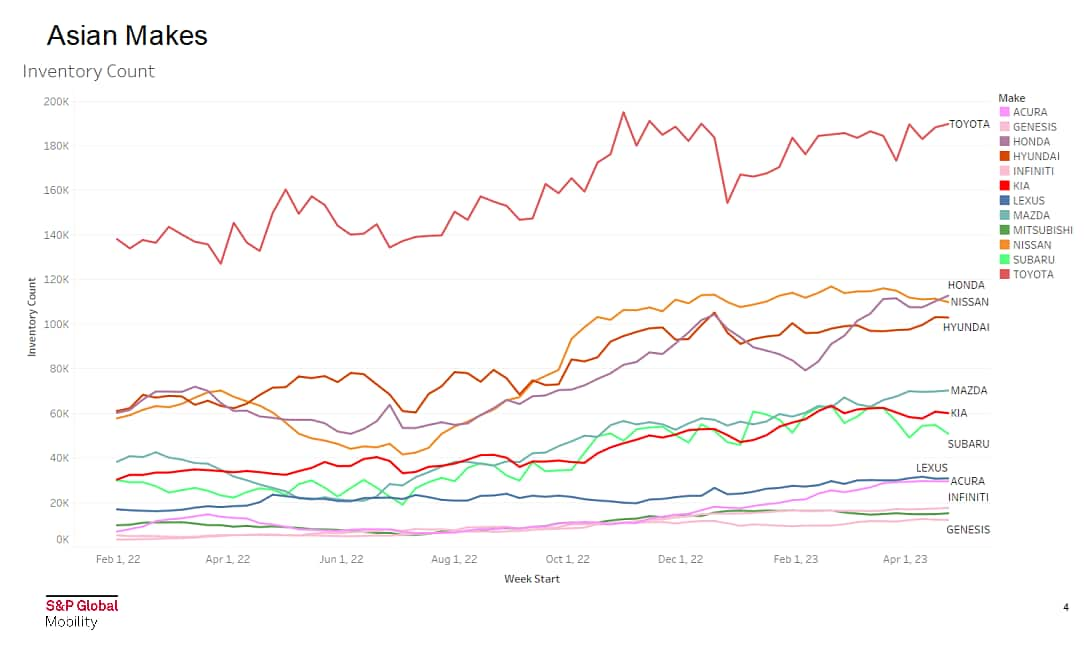

Meanwhile, Asian makes continue to struggle to gain inventory

count on dealership lots. Since the new year, volume leader Toyota

has kept on pace to have advertised inventories equivalent to one

month’s pre-pandemic sales. Honda, Nissan, and Hyundai all have

roughly the same advertised dealer inventories.

European brand advertised inventory actually shrank in the last

month and was flat in the last quarter. That masked wide

disparities among individual automakers, however. Volkswagen

advertised inventory spiked by 16% in the last quarter, while BMW

advertised inventory dropped by 22%, for example. The same erratic

trends continued in the last month.

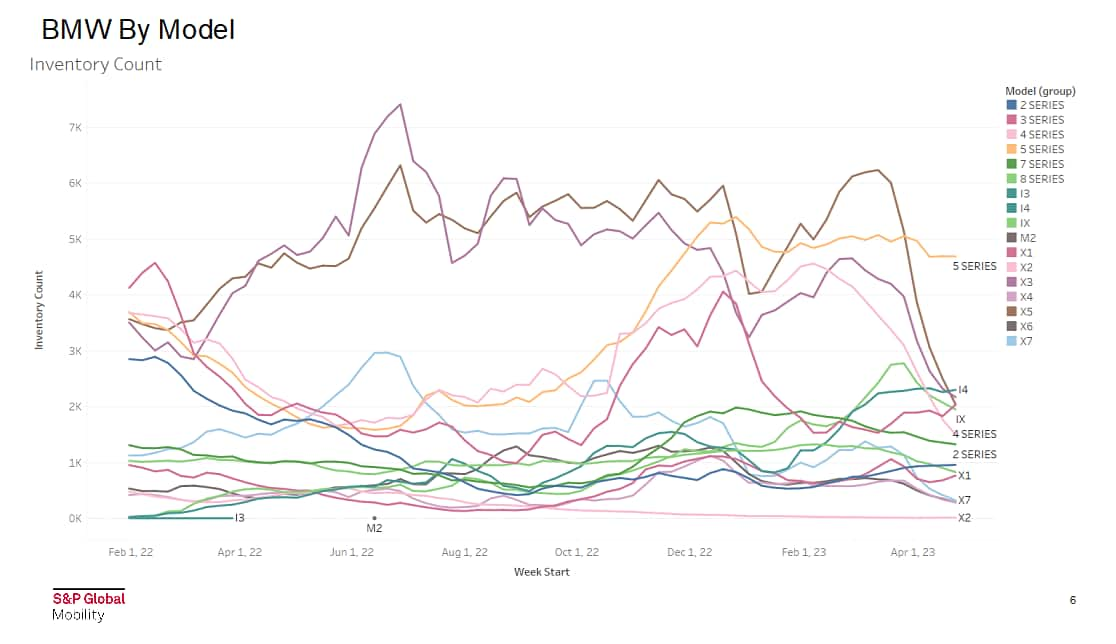

Taking a look at BMW specifically, individual model inventory

has fluctuated greatly over the last half year. The 5 Series

advertised inventory rose in the last quarter of 2022, then

remained constant. The high-volume X3, X5, and 3 Series saw

advertised inventory decrease sharply late last year and early this

year. The X5 has seen the most fluctuation.

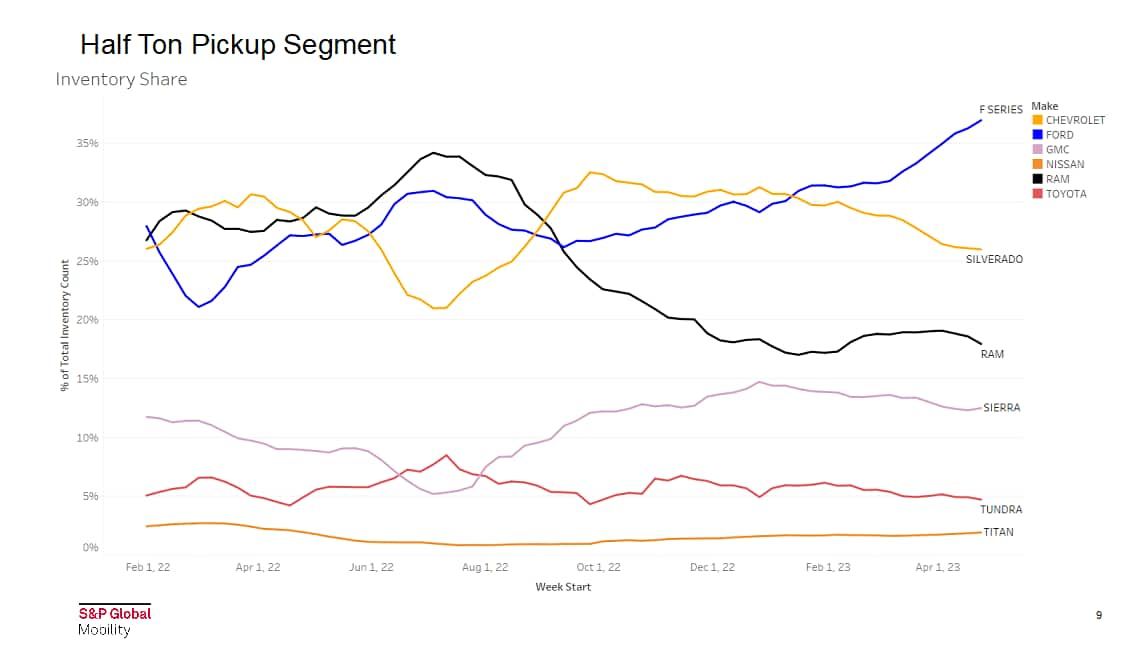

Moving to half-ton pickups, Ford, Chevrolet, and Ram trucks

were, on average, advertised below MSRP from February 2022 to April

2023, while the Toyota Tundra was advertised above MSRP for that

entire period.

In this hyper-competitive full-size segment, Ram has

consistently seen the greatest advertised discounts from MSRP,

although other domestic truck brands are more recently engaging in

a race to that discount level.

Ford’s F-Series advertised inventory increased sharply beginning

late Sept 2022 from around 47,000 units to 110,000 in April 2023.

Part of the increase can be assigned to post-build trucks parked in

giant lots awaiting essential final parts before finally being

allocated to dealers.

But while the advertised dealer inventory unit count of

Chevrolet Silverado has climbed and Ram full-size pickups have

remained steady, the sharp increase of F-150 unit count means Chevy

and Ram share of half-ton pickup inventory has fallen off and not

recovered since late summer. Only the GMC Sierra has matched the

F-150s pace of share increase.

Battery-electric and hybrid-electric vehicle advertised

inventory tripled from February 2022 to early April 2023 to some

300,000 units, a faster rate of increase than advertised

inventories of pure internal-combustion vehicles. That said, the

amount of xEV inventory remains in line with current market share

percentages for BEVs and hybrids.

As the industry continues to replenish its inventory, there will

be knock-on effects in terms of pricing and incentives. S&P

Global Mobility analysts foresee the stabilizing of inventory,

combined with economic headwinds facing consumers, to create

a more traditional retail environment in 2023 with OEMs once

again battling for market share.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/8-vehicle-inventory-trends-you-should-know-about-in-may.html

- :has

- :is

- :not

- ][p

- 000

- 110

- 2022

- 2023

- 8

- a

- About

- above

- across

- actually

- again

- All

- allocated

- Although

- among

- amount

- an

- analysis

- Analysts

- and

- annualized

- April

- ARE

- around

- article

- AS

- asian

- assigned

- At

- automakers

- availability

- average

- awaiting

- based

- Basically

- basis

- battling

- BE

- been

- before

- Beginning

- being

- below

- BMW

- brand

- brands

- by

- CAN

- Chevrolet

- Climbed

- combined

- comparison

- constant

- Consumers

- continue

- continued

- continues

- country

- create

- Current

- data

- dealer

- decrease

- Depending

- digits

- Discount

- discounts

- Division

- Domestic

- dropped

- Early

- Economic

- effects

- engaging

- Entire

- Environment

- Equivalent

- essential

- example

- facing

- Fallen

- faster

- February

- final

- Finally

- flat

- fluctuated

- fluctuation

- For

- Ford

- from

- front

- Gain

- giant

- Global

- greatest

- greatly

- Growth

- Half

- Have

- headwinds

- However

- HTML

- HTTPS

- Hyundai

- in

- Incentives

- Increase

- increased

- individual

- industry

- inventory

- IT

- ITS

- July

- kept

- Key

- Know

- Last

- Last Year

- Late

- leader

- Level

- Line

- Look

- MAKES

- managed

- Market

- matched

- May..

- means

- Meanwhile

- mobility

- model

- Month

- months

- more

- most

- Near

- New

- new year

- Nissan

- of

- off

- offered

- on

- once

- ONE

- only

- Other

- over

- overall

- Pace

- part

- parts

- percentage

- percentages

- period

- Pickup

- plato

- Plato Data Intelligence

- PlatoData

- price

- pricing

- published

- purchase

- Quarter

- Race

- RAM

- Rate

- ratings

- recently

- recovery

- remain

- remained

- remains

- retail

- Rise

- Risen

- ROSE

- roughly

- s

- S&P

- S&P Global

- Said

- sales

- same

- seen

- segment

- separately

- Series

- Share

- sharp

- should

- Shows

- since

- single

- SIX

- Six months

- Slowing

- some

- specifically

- stable

- steady

- Struggle

- summer

- term

- terms

- than

- that

- The

- then

- There.

- this

- Through

- to

- toyota

- traditional

- Trends

- truck

- Trucks

- unit

- units

- until

- vehicle

- Vehicles

- volkswagen

- volume

- was

- were

- which

- while

- wide

- will

- with

- year

- you

- zephyrnet