As digital technologies continue to transform the financial landscape, central banks worldwide are exploring the potential of Central Bank Digital Currencies (CBDCs).

Thailand, under the guidance of the Bank of Thailand (BOT), has been at the forefront of this movement, continuously studying and testing the feasibility of a Retail CBDC since 2018.

The country’s latest milestone, the Thailand Retail CBDC (RCBDC) Pilot Programme, marks a significant step forward in understanding the implications of a digital currency for the Thai economy.

Thailand’s CBDC journey

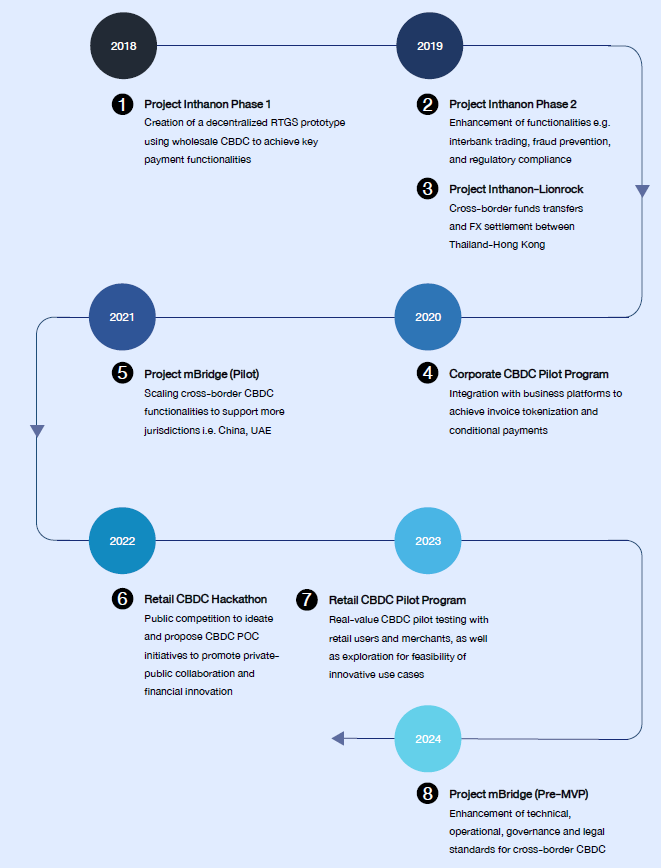

The BOT’s journey towards a CBDC began in 2018 with Project Inthanon, which focused on creating a decentralised Real-Time Gross Settlement (RTGS) prototype using wholesale CBDC.

The project evolved, incorporating enhanced functionalities, cross-border fund transfers, and a Corporate CBDC Pilot Program.

In 2022, the BOT initiated a Retail CBDC Hackathon to encourage public participation and promote private-public collaboration in developing CBDC proof-of-concept initiatives.

This led to the launch of the Retail CBDC Pilot Programme in 2023, which involved real-value CBDC testing with retail users and merchants and the exploration of innovative use cases.

Pilot objectives and design of Thailand Retail CDBC Pilot progamme

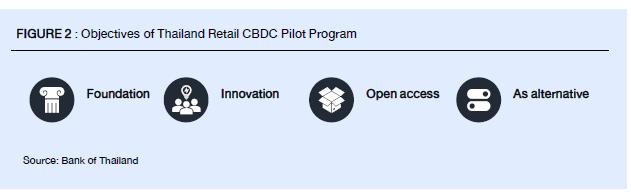

Four primary objectives drove the Thailand Retail CBDC Pilot Programme: assessing the technological readiness and fundamental functions of RCBDC, evaluating the potential of RCBDC for harnessing financial innovation, exploring the feasibility of open access to CBDC infrastructure for both banks and non-banks, and determining the viability of RCBDC as an alternative payment infrastructure for individuals and businesses.

To address these objectives, the BOT conducted the pilot test within a confined environment, divided into the Foundation Track and the Innovation Track.

The Foundation Track focused on testing CBDC’s core functionalities, open access feasibility, and potential as an alternative payment infrastructure.

This involved real-value transactions in a ring-fenced environment, with bank and non-bank participants acting as financial service providers (FSPs) and selected users and merchants. The Innovation Track consisted of public engagements and exploring CBDC for financial innovation.

The BOT invited the public and participating FSPs to showcase how RCBDC could facilitate innovation and value-added payments beyond the limits of the existing infrastructure.

Technical design and testing scope

The BOT collaborated with Giesecke + Devrient advance52 GmbH (G+D) and chose their Filia solution for the Thailand Retail CBDC pilot.

This decision was based on the solution’s flexible ledger choice, privacy enhancement through token-based architecture, built-in programmable payment features, and ease of integration.

The Foundation Track tested the core functionality of CBDC from late 2022 to September 2023, involving 3 FSPs, approximately 4,000 individual users, and 140 participating merchants.

Transactions tested included retail transfers among individuals and retail payments with merchants for purchasing goods and services.

The Foundation Track also covered testing of offline CBDC capabilities, which aimed to assess CBDC’s potential to enhance payment system resiliency in scenarios involving internet dead spots, temporary shortages, or disasters.

The BOT utilised a fully offline CBDC solution to support consecutive offline payments using physical smartcards and smartphones.

Pilot findings

The Thailand Retail CBDC Pilot Programme provided valuable insights into various aspects of CBDC implementation, including business, legal, technical, accounting, and operational considerations.

The pilot revealed that the CBDC design functioned well for minting, distribution, and melting of CBDC and was well-integrated and interoperable with the existing payment infrastructure.

The BOT and relevant government agencies engaged in dialogues to address legal, accounting, and AML/CFT aspects associated with CBDC implementation.

The Retail CBDC efficiently maintained the capability to handle retail payment transactions without any material system errors. The CBDC design demonstrated its potential for scaling innovation through common functionality features and token-based nature.

The pilot results showed that RCBDC could support access and integration for bank and non-bank FSPs, addressing existing pain points in the payment infrastructure. Furthermore, Retail CBDC demonstrated its capability to serve as an alternative channel for retail payments, with the potential to handle high transaction volumes.

Challenges and considerations

Despite the promising findings, the Retail CBDC Pilot Programme also revealed several challenges and considerations that must be addressed.

Non-bank business models remain a concern, as non-banks still had to rely on banks and faced transaction fees for exchanging Thai baht with RCBDC, necessitating further exploration of sustainable business models for non-banks.

In-progress transactions and double payment handling also pose a challenge, as the BOT’s role as a validator may require involvement in retail transaction management, particularly in pending or failed transactions.

Offline CBDC limitations, such as instability in connectivity between offline devices and potential cyber threats to Retail CBDC kept in offline devices for extended periods, remain challenges to be addressed.

The positioning of Retail CBDC for public use is another consideration, as the design and positioning of RCBDC should consider public needs beyond the capabilities of the existing payment infrastructure to encourage adoption.

Establishing appropriate governance models to onboard innovative features for common CBDC functionality open to all FSP players remains challenging. Additionally, relevant laws and regulations must be considered and aligned if RCBDC is to be launched.

Retail CBDC, as a public infrastructure, should consider the format of business and services together with conditions for their business models to support a variety of players and foster competition. The choice of technology solutions for CBDC implementation should also be re-evaluated in the future, considering adaptability, cyber risks, and threats.

Future of CBDC in Thailand

The Retail CBDC Pilot Programme has been a crucial step in Thailand’s journey toward understanding the potential of a digital currency.

The insights gained from the pilot, particularly regarding CBDC design and technology, will serve as a valuable reference for future initiatives in payment system development.

While the BOT has no immediate plans to officially issue RCBDC, the lessons learned from the pilot will be leveraged to support upcoming projects, such as programmable payments by the private sector and the tokenisation of assets.

As Thailand continues to explore the possibilities of CBDC, close collaboration between the BOT and the private sector will be essential in shaping the future of the country’s financial landscape.

The Retail CBDC Pilot Programme has laid the groundwork for further innovation and development in digital currencies, positioning Thailand at the forefront of this global financial revolution.

As the world watches the evolution of CBDCs, Thailand’s experiences and insights will undoubtedly contribute to the broader understanding of the potential and challenges associated with these digital assets.

Featured image credit: Edited from Unsplash

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/94883/thailand/bank-of-thailand-retail-cbdc-pilot-program-reveals-key-findings/

- :has

- :is

- 000

- 1

- 140

- 2018

- 2022

- 2023

- 4

- 7

- 750

- 900

- a

- access

- Accounting

- acting

- adaptability

- Additionally

- address

- addressed

- addressing

- Adoption

- agencies

- aimed

- aligned

- All

- also

- alternative

- among

- an

- and

- Another

- any

- appropriate

- approximately

- architecture

- ARE

- AS

- aspects

- assess

- Assessing

- Assets

- associated

- At

- baht

- Bank

- Bank of Thailand

- Banks

- based

- BE

- been

- began

- begin

- between

- Beyond

- Bot

- both

- broader

- built-in

- business

- business models

- businesses

- by

- capabilities

- capability

- caps

- cases

- CBDC

- cbdc pilot

- CBDCs

- central

- Central Bank

- central bank digital currencies

- CENTRAL BANK DIGITAL CURRENCIES (CBDCS)

- Central Banks

- challenge

- challenges

- challenging

- Channel

- choice

- chose

- Close

- collaborated

- collaboration

- Common

- competition

- Concern

- concludes

- conditions

- conducted

- Connectivity

- consecutive

- Consider

- consideration

- considerations

- considered

- considering

- content

- continue

- continues

- continuously

- contribute

- Core

- Corporate

- could

- country’s

- covered

- Creating

- credit

- cross-border

- crucial

- CSS

- currencies

- Currency

- cyber

- dead

- decentralised

- decision

- demonstrated

- Design

- determining

- developing

- Development

- Devices

- dialogues

- digital

- Digital Assets

- digital currencies

- digital currency

- digital technologies

- disasters

- distribution

- divided

- double

- ease

- economy

- edited

- efficiently

- encourage

- end

- engaged

- engagements

- enhance

- enhanced

- enhancement

- Environment

- Errors

- essential

- evaluating

- evolution

- evolved

- exchanging

- existing

- Experiences

- exploration

- explore

- Exploring

- extended

- faced

- facilitate

- Failed

- feasibility

- Features

- Fees

- financial

- financial innovation

- financial revolution

- financial service

- findings

- fintech

- flexible

- focused

- For

- forefront

- form

- format

- Forward

- Foster

- Foundation

- from

- fully

- functionalities

- functionality

- functions

- fund

- fundamental

- further

- Furthermore

- future

- G+D

- gained

- Global

- global financial

- GmBH

- goods

- governance

- Government

- government agencies

- gross

- groundwork

- guidance

- hackathon

- had

- handle

- Handling

- Harnessing

- High

- hottest

- How

- HTTPS

- if

- image

- immediate

- implementation

- implications

- in

- included

- Including

- incorporating

- individual

- individuals

- Infrastructure

- initiated

- initiatives

- Innovation

- innovative

- insights

- instability

- integration

- Internet

- interoperable

- into

- invited

- involved

- involvement

- involving

- issue

- ITS

- journey

- kept

- Key

- laid

- landscape

- Late

- latest

- launch

- launched

- Laws

- Laws and regulations

- learned

- Led

- Ledger

- Legal

- Lessons

- Lessons Learned

- leveraged

- limitations

- limits

- mailchimp

- maintained

- management

- material

- max-width

- May..

- Merchants

- milestone

- minting

- models

- Month

- movement

- must

- Nature

- necessitating

- needs

- news

- no

- objectives

- of

- Officially

- offline

- on

- Onboard

- once

- open

- operational

- or

- Pain

- Pain points

- participants

- participating

- participation

- particularly

- payment

- payment system

- payments

- pending

- periods

- physical

- pilot

- plans

- plato

- Plato Data Intelligence

- PlatoData

- players

- points

- pose

- positioning

- possibilities

- potential

- primary

- privacy

- private

- private sector

- Program

- programmable

- programme

- project

- projects

- promising

- promote

- prototype

- provided

- providers

- public

- purchasing

- Readiness

- real-time

- reference

- regarding

- regulations

- relevant

- rely

- remain

- remains

- require

- Results

- retail

- retail CBDC

- Revealed

- Reveals

- Revolution

- risks

- Role

- RTGS

- scaling

- scenarios

- sector

- selected

- September

- serve

- service

- service providers

- Services

- settlement

- several

- shaping

- shortages

- should

- showcase

- showed

- significant

- since

- Singapore

- smartphones

- solution

- Solutions

- spots

- Step

- Still

- Studying

- such

- support

- sustainable

- system

- Technical

- technological

- Technologies

- Technology

- temporary

- test

- tested

- Testing

- thai

- Thailand

- Thailand’s

- that

- The

- The Future

- the world

- their

- These

- this

- threats

- Through

- to

- together

- tokenisation

- toward

- track

- transaction

- Transaction Fees

- Transactions

- transfers

- Transform

- under

- understanding

- undoubtedly

- upcoming

- use

- users

- using

- Validator

- Valuable

- variety

- various

- viability

- volumes

- was

- watches

- WELL

- which

- wholesale

- wholesale CBDC

- will

- with

- within

- without

- world

- worldwide

- Your

- zephyrnet