Decarbonization efforts, aiming for Net Zero emissions, require significant changes in the energy sector. This transition requires shifting from fossil fuels to metals and critical minerals like cobalt, copper, lithium, nickel, and rare earths.

The critical minerals market will grow 7-fold by 2030, and 10-fold by 2050 to over $400 billion, per the International Energy Agency estimates. Cobalt, in particular, has a central role in reaching the global net zero target.

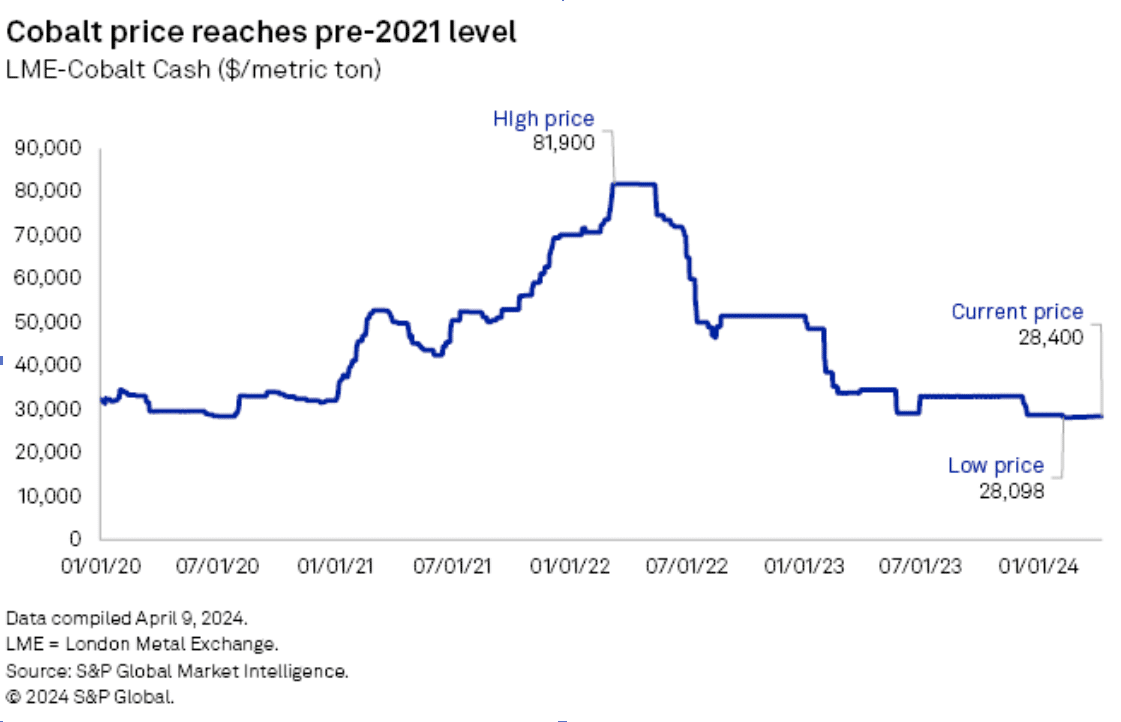

Cobalt prices have plummeted to pre-2021 levels since the beginning of the year, with analysts predicting a continued decline. As of April 8, the London Metal Exchange cobalt cash price stands at $28,400 per metric ton, marking a 65.3% drop from the 2022 high of $81,900/t in March,

This decline is attributed to the lack of expected demand from the electric vehicle sector, which has also affected demand growth in aerospace and consumer electronics.

The oversupply of cobalt in the market is exacerbated by increased output from producers in Indonesia and the Democratic Republic of Congo (DRC). Chinese production has also surged, further pressuring prices. Forecasts indicate that the cobalt market will remain oversupplied by 4,000 metric tons this year and in the forthcoming years.

Balancing Supply and Demand

Despite the price reaction to excess cobalt, producers are unlikely to cut output significantly. Cobalt production is tied to the dynamics and production costs of the copper and nickel industries, both of which continue to see robust output. While some high-cost cobalt producers may reduce output, low-cost producers are expanding production.

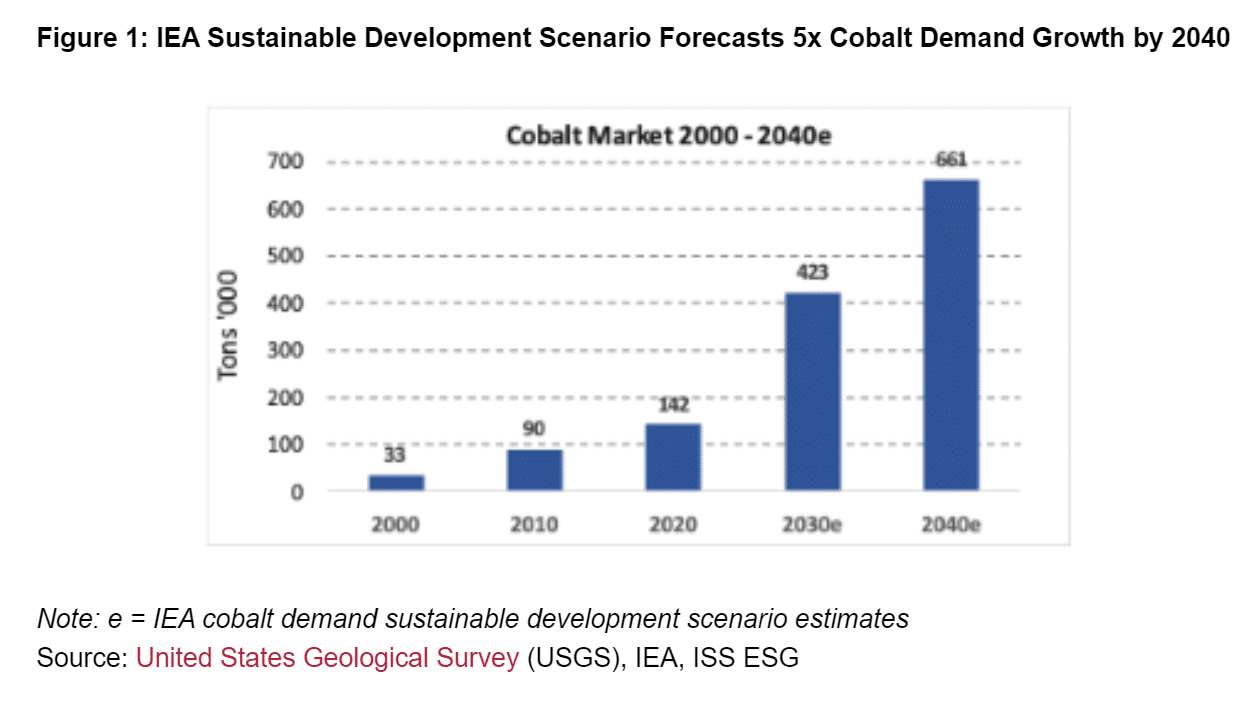

The IEA predicts a substantial increase in cobalt demand, with growth projected to be 5x higher between 2020 and 2040 under its Sustainable Development Scenario.

The expected dramatic growth in cobalt demand underscores the need for increased production, with the IEA forecasting a 3-fold increase by 2030. This growth trajectory calls for the development of new mines and deposits to meet sustainability goals and mitigate supply risks.

The agency also predicts that as early as 2030, mines will produce only 50% of the cobalt and lithium and 80% of copper required for the energy transition.

The High Stakes of Cobalt Mining

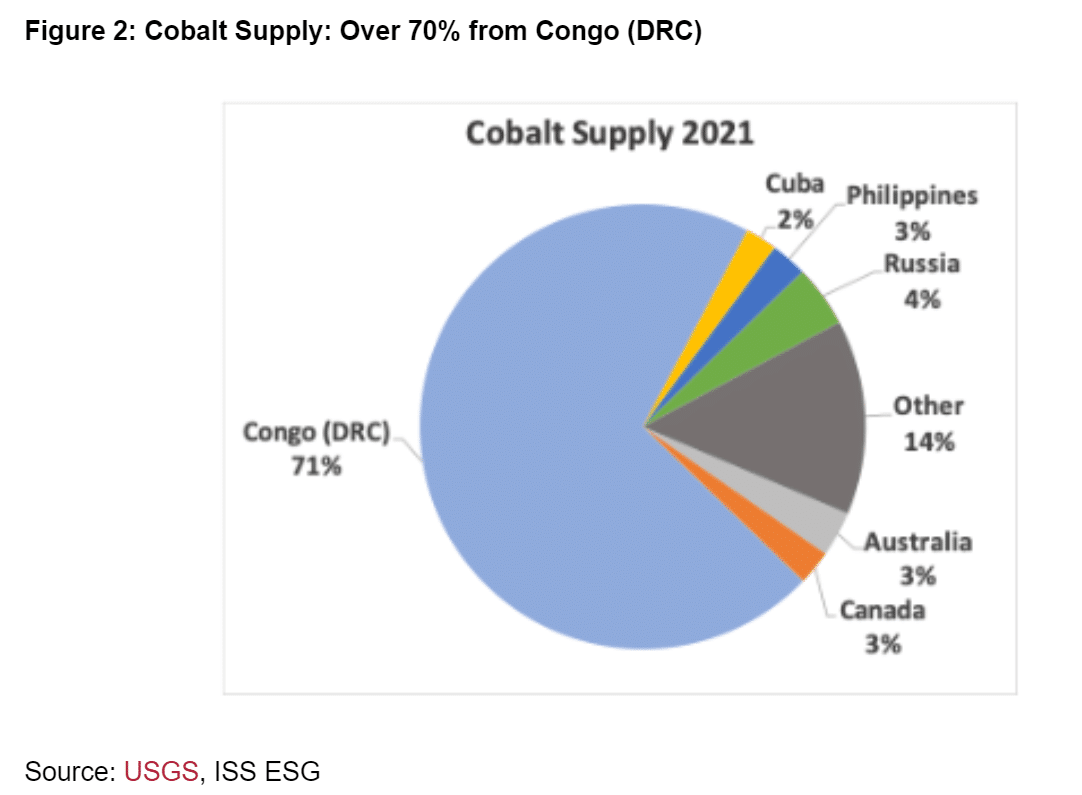

The pressure on the cobalt supply chain is already evident. This is especially considering that the Democratic Republic of Congo supplies about 70% of the world’s cobalt. This raises concerns about reliance on a single source with questionable environmental, social, and governance (ESG) credentials.

This heavy reliance on a single source also poses significant supply chain risks, as evidenced by recent challenges in the European natural gas market.

Apart from supply concentration, cobalt mining practices and related issues in the DRC raise concerns for investors. These include environmental degradation, human rights violations, and governance challenges. As a result, investors are increasingly seeking alternative cobalt sources that offer greater transparency and sustainability.

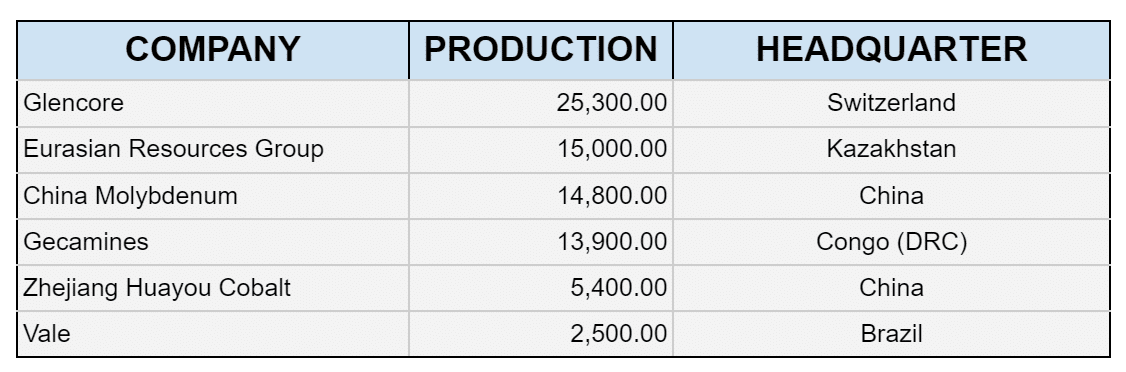

The cobalt mining industry also exhibits a degree of concentration, with the top four mining companies contributing over 40% of global production. Glencore, a diversified mining and trading company, stands out as the largest producer, accounting for over 15% of total production. Interestingly, many of these major mining companies are located in emerging markets.

However, there are challenges associated with assessing the ESG performance of these companies, particularly those that are privately held. Vale, despite having the lowest cobalt production among the top five companies, boasts the highest ESG rating of C+.

Australia and Canada are notable for their substantial cobalt reserves of critical minerals and relatively strong ESG ratings. These countries offer opportunities to diversify the global production mix of critical minerals.

While the DRC remains a dominant cobalt supplier, there are alternative sources available, although they may not be as abundant. Exploring these alternative supply options is crucial for mitigating supply chain risks and ensuring responsible cobalt sourcing practices.

Investing in Cobalt for a Greener Future

In response to the risks posed by concentration and ESG concerns in cobalt production, stakeholders, including investors and active asset owners, can play a significant role. They can advocate for greater transparency across the cobalt supply chain, incentivize sustainable practices through capital allocation, and engage with companies to improve their ESG performance.

Additionally, investors may explore opportunities to support projects in jurisdictions with stronger regulatory frameworks and environmental protections. There are tools available to assist investors in navigating these challenges and pursuing responsible investment opportunities.

Although the bottom for cobalt prices is uncertain, some analysts anticipate a gradual improvement in prices over the next few quarters. However, the market remains volatile, and the trajectory of cobalt prices will depend on various factors. These particularly include demand trends and production dynamics in related industries.

In summary, as the world moves towards Net Zero emissions, the critical role of cobalt in the energy transition highlights the importance of sustainable and diversified supply chains to meet increasing demand while addressing ESG concerns.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://carboncredits.com/cobalt-crunch-prices-plummet-supply-challenges-loom-in-the-race-to-net-zero/

- :has

- :is

- :not

- 000

- 15%

- 2020

- 2022

- 2030

- 2040

- 2050

- 4

- 400

- 65

- 8

- a

- About

- abundant

- Accounting

- across

- active

- addressing

- advocate

- Aerospace

- affected

- agency

- Aiming

- allocation

- already

- also

- alternative

- Although

- among

- Analysts

- and

- annum

- anticipate

- April

- ARE

- AS

- Assessing

- asset

- assist

- associated

- At

- available

- BE

- Beginning

- between

- Billion

- boasts

- both

- Bottom

- by

- Calls

- CAN

- Canada

- capital

- Cash

- central

- chain

- chains

- challenges

- Changes

- chinese

- Companies

- company

- concentration

- Concerns

- Congo

- considering

- consumer

- Consumer electronics

- continue

- continued

- contributing

- Copper

- Costs

- countries

- Credentials

- critical

- crucial

- crunch

- Cut

- Decline

- Degree

- Demand

- democratic

- depend

- deposits

- Despite

- Development

- diversified

- diversify

- dominant

- dramatic

- drc

- Drop

- dynamics

- Early

- efforts

- Electric

- electric vehicle

- Electronics

- emerging

- emerging markets

- Emissions

- energy

- engage

- ensuring

- environmental

- ESG

- especially

- estimates

- European

- European natural gas

- evidenced

- evident

- excess

- exchange

- exhibits

- expanding

- expected

- explore

- Exploring

- factors

- false

- few

- five

- For

- For Investors

- forecasts

- forthcoming

- fossil

- fossil fuels

- four

- frameworks

- from

- fuels

- further

- GAS

- Global

- Goals

- governance

- gradual

- greater

- greener

- Grow

- Growth

- Have

- having

- heavy

- Held

- High

- higher

- highest

- highlights

- However

- HTTPS

- human

- human rights

- IEA

- importance

- improve

- improvement

- in

- incentivize

- include

- Including

- Increase

- increased

- increasing

- increasingly

- indicate

- Indonesia

- industries

- industry

- International

- investment

- investment opportunities

- Investors

- issues

- ITS

- jurisdictions

- Lack

- largest

- levels

- like

- lithium

- located

- London

- loom

- low-cost

- lowest

- major

- many

- March

- Market

- Markets

- marking

- max-width

- May..

- Meet

- metal

- Metals

- metric

- minerals

- mines

- Mining

- Mining Companies

- Mining Industry

- Mitigate

- mitigating

- mix

- moves

- Natural

- Natural Gas

- navigating

- Need

- net

- New

- next

- Nickel

- notable

- of

- offer

- on

- only

- opportunities

- Options

- out

- output

- over

- owners

- particular

- particularly

- per

- performance

- plato

- Plato Data Intelligence

- PlatoData

- Play

- Plummet

- posed

- poses

- practices

- predicting

- Predicts

- pressure

- price

- Prices

- privately

- produce

- producer

- Producers

- Production

- projected

- projects

- pursuing

- Race

- raise

- raises

- RARE

- rating

- reaching

- reaction

- recent

- reduce

- regulatory

- related

- relatively

- reliance

- remain

- remains

- Republic

- require

- required

- requires

- reserves

- response

- responsible

- result

- rights

- risks

- robust

- Role

- sector

- see

- seeking

- SHIFTING

- significant

- significantly

- since

- single

- Social

- some

- Source

- Sources

- Sourcing

- stakeholders

- stakes

- stands

- strong

- stronger

- substantial

- SUMMARY

- supplier

- supplies

- supply

- supply chain

- Supply chains

- support

- Surged

- Sustainability

- sustainable

- Target

- that

- The

- the world

- their

- There.

- These

- they

- this

- this year

- those

- Through

- Tied

- to

- Ton

- tons

- tools

- top

- Total

- towards

- Trading

- trajectory

- transition

- Transparency

- Trends

- Uncertain

- under

- underscores

- unlikely

- various

- vehicle

- Violations

- volatile

- which

- while

- will

- with

- world

- world’s

- year

- years

- zephyrnet

- zero