The digital economy of Southeast Asia remains robust, its resilience cemented by digital financial services that have proven to be the bedrock of growth amidst the pandemic and prevailing economic turbulence. The link between revenue and gross merchandise value (GMV) has been striking, with the former surging at a rate 1.7 times the latter’s increase, embodying the region’s economic tenacity.

Investment Trends and Sectoral Dominance

In light of recent findings by the e-Conomy SEA 2023 report, curated for the eighth year by industry giants Google, Temasek, and Bain & Company, the sobering reality is that private funding in Southeast Asia has witnessed a sharp decline, hitting a six-year nadir in the aftermath of record-breaking highs in previous years.

This downturn aligns with a global paradigm shift towards a more prohibitive cost of capital as well as multifaceted funding lifecycle challenges. Despite a contraction in investments across a range of industries, digital financial services have sustained their prominence and growth trajectory, coming up as the premier segment for investments, thanks to their substantial potential for monetisation.

Financial Services Buoys the SEA Digital Economy

Southeast Asia stands out for its dual success in GMV and revenue progression, a testament to the harmonious relationship between market expansion and profitability. Digital enterprises have skilfully navigated from a phase of acquiring users towards now intensifying engagement with existing customers, underpinning the region’s digital economy.

2023 has seen the SEA digital economy’s revenue hit an impressive benchmark of US$100 billion, climbing at a compound annual growth rate (CAGR) of 27% since 2021 — a growth rate outpacing GMV by 1.7 times.

The Surge of Digital Payments and Lending

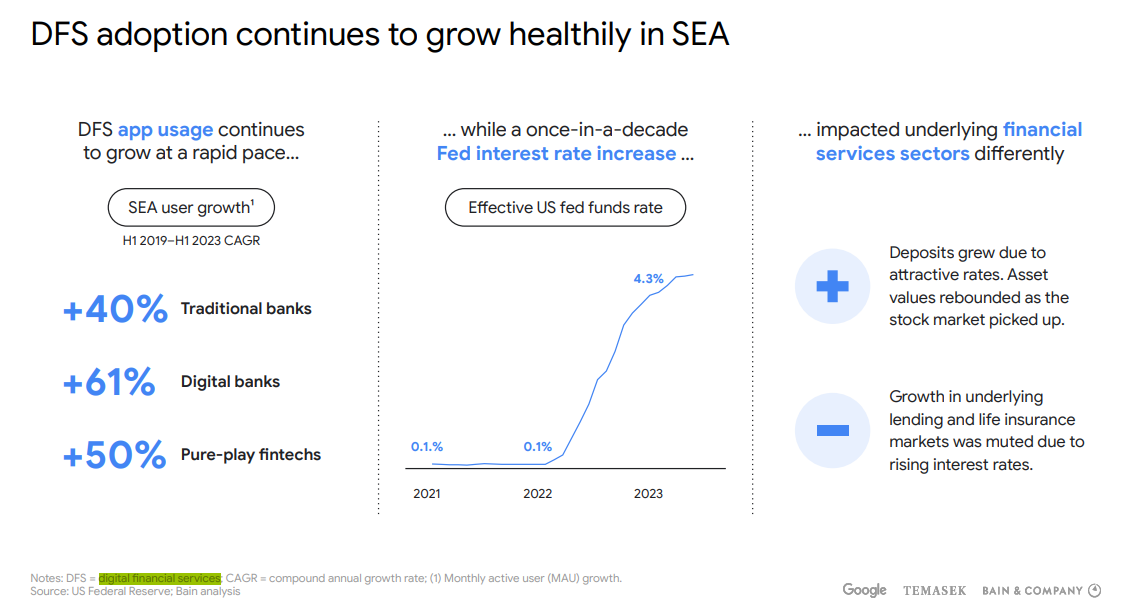

Within the digital financial services sector, the dominance of digital payments is unequivocal, comprising over half of the transaction value within the region. This growth is propelled by a steadfast shift in consumer behaviour from offline to online, marking a continued upsurge in the adoption of digital services, notably digital payments.

The competitive landscape is intensifying. Fintech startups have branched out, offering lending services to the previously underserved, while entrenched financial entities are rapidly transitioning their sizeable customer bases to digitised platforms.

The allure of digital wealth management beckons, promising a retention of affluent clients. The wealth management sector is experiencing robust growth, propelled by the expansion of digital services from established banks and the uptake of innovative fintechs and digital banking platforms.

Although the sector is still in its nascent stages, there has been a noticeable increase in fees due to a shift in the mix, given that emerging markets usually experience more rapid growth. However, as platforms continue to focus on acquiring users, the level of monetisation has remained relatively modest.

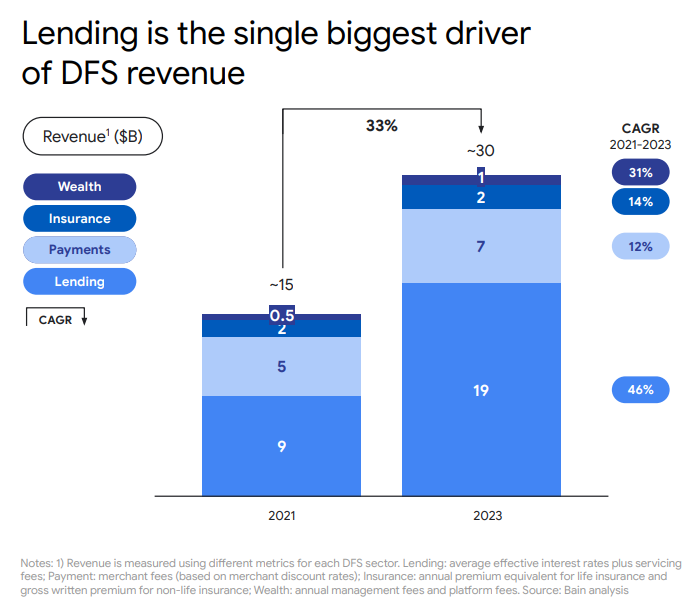

In this environment, the the e-Conomy SEA 2023 research indicates that digital lending has emerged as the juggernaut, fuelling a US$30 billion revenue stream within digital financial services, buoyed by high interest rates and a spike in demand from traditionally underbanked sectors and SMEs.

The report projects that Singapore will lead the regional digital lending sphere from 2023 to 2030, with Indonesia taking the lead in digital payments.

Consumer Adoption and the Future of Digital Financial Services

The digital financial services landscape is witnessing a monumental shift with consumers embracing digital services at an unprecedented pace, signalling a wane in the era of cash dominance.

Despite favourable conditions for deposits and wealth management due to high-interest rates, lending faces hurdles. Nevertheless, the spectre of non-performing loans remains in check.

In the midst of this, sustainable business models begin to flourish within fintech firms, as their traditional counterparts hasten digitalisation efforts, all in a bid to secure and grow their user base. This financial landscape, rapidly evolving yet sturdy, illustrates the intricate dance between innovation and reliability that digital financial services perform — a balance that Southeast Asia is leading with aplomb.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/80024/fintech/lending-is-the-single-largest-fintech-revenue-driver-in-southeast-asia/

- :has

- :is

- $UP

- 1

- 2021

- 2023

- 2030

- 27

- 610

- 7

- a

- acquiring

- across

- Adoption

- aftermath

- AI

- Aligns

- All

- allure

- amidst

- an

- and

- annual

- ARE

- AS

- asia

- At

- author

- Bain

- Balance

- Banking

- Banks

- base

- BE

- beckons

- been

- begin

- behaviour

- Benchmark

- between

- bid

- Billion

- business

- business models

- by

- CAGR

- capital

- caps

- Cash

- cemented

- challenges

- check

- clients

- Climbing

- coming

- company

- competitive

- Compound

- comprising

- conditions

- consumer

- Consumers

- content

- continue

- continued

- contraction

- Cost

- counterparts

- curated

- customer

- Customers

- dance

- Decline

- Demand

- deposits

- Despite

- digital

- Digital economy

- digital lending

- Digital Payments

- digital services

- digitalisation

- Dominance

- DOWNTURN

- driver

- due

- Economic

- economic turbulence

- economy

- economy’s

- efforts

- Eighth

- embracing

- emerged

- emerging

- emerging markets

- end

- engagement

- enterprises

- entities

- entrenched

- Environment

- Era

- established

- Ether (ETH)

- evolving

- existing

- expansion

- experience

- experiencing

- faces

- Fees

- financial

- financial services

- findings

- fintech

- fintech startups

- firms

- flourish

- Focus

- For

- form

- Former

- from

- funding

- future

- giants

- given

- Global

- gross

- Grow

- Growth

- Half

- harmonious

- Have

- High

- Highs

- Hit

- hitting

- hottest

- However

- HTTPS

- Hurdles

- illustrates

- impressive

- in

- Increase

- indicates

- Indonesia

- industries

- industry

- Innovation

- innovative

- intensifying

- interest

- Interest Rates

- intricate

- Investments

- ITS

- jpg

- landscape

- largest

- lead

- leading

- lending

- Level

- lifecycle

- light

- LINK

- Loans

- mailchimp

- management

- Market

- Markets

- marking

- max-width

- merchandise

- mix

- models

- modest

- monetisation

- Month

- monumental

- more

- multifaceted

- nascent

- Nevertheless

- news

- notably

- now

- of

- offering

- offline

- on

- once

- online

- out

- over

- Pace

- pandemic

- paradigm

- payments

- perform

- phase

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- Posts

- potential

- premier

- prevailing

- previous

- previously

- private

- profitability

- progression

- projects

- prominence

- promising

- propelled

- proven

- range

- rapid

- rapidly

- Rate

- Rates

- Reality

- recent

- region

- regional

- relationship

- relatively

- reliability

- remained

- remains

- report

- research

- resilience

- retention

- revenue

- robust

- SEA

- sector

- sectoral

- Sectors

- secure

- seen

- segment

- Services

- sharp

- shift

- since

- Singapore

- single

- SMEs

- sobering

- southeast

- Southeast Asia

- Spectre

- spike

- stages

- stands

- Startups

- steadfast

- Still

- stream

- sturdy

- substantial

- success

- surge

- surging

- sustainable

- sustained

- taking

- Temasek

- testament

- thanks

- that

- The

- The Future

- their

- There.

- this

- times

- to

- towards

- traditional

- traditionally

- trajectory

- transaction

- transitioning

- Trends

- turbulence

- underbanked

- underpinning

- underserved

- unprecedented

- User

- users

- usually

- value

- Wealth

- wealth management

- WELL

- while

- will

- with

- within

- witnessed

- witnessing

- year

- years

- yet

- Your

- zephyrnet