Accustomed to the highly personalized digital experiences they get from bigtechs like Google and Amazon, banking and insurance customers are increasingly growing dissatisfied with the services they receive from their traditional financial services providers.

This suggests a gap between customers’ expectations and what’s being offered to them, and implies that financial services institutions need to step up their game to meet the expectations of an increasingly digital-first clientele, a Saleforce 2022 survey found.

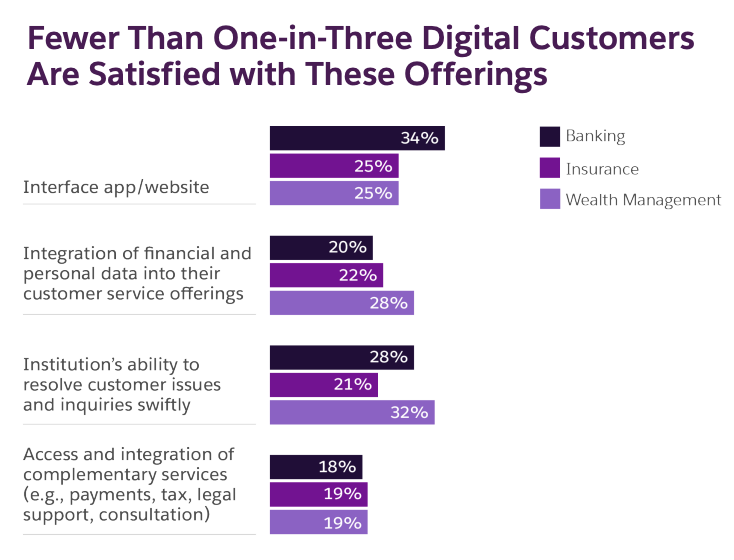

The survey, which polled 2,250 customers in North America, Europe and Asia-Pacific (APAC), found that less than one third of banking, wealth and insurance customers are satisfied with their providers’ digital interfaces, as well as their advice personalization and integration capabilities.

Banking, wealth and insurance customers’ satisfaction levels, Source: The Future of Financial Services 2022, Salesforces

Only 11% of banking customers agreed that their providers anticipate their financial needs effectively and 15% of insurance customers said their insurer are invested in their financial wellbeing, indicating that incumbents are failing to meet their customers’ needs.

Addressing customers’ needs and investing in their financial wellbeing, Source: The Future of Financial Services 2022, Salesforces

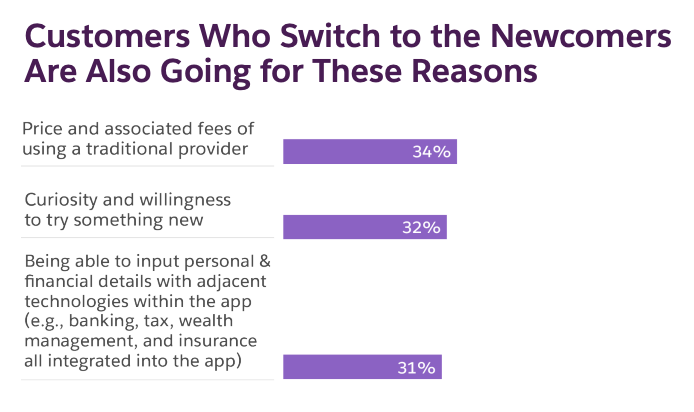

Results from the survey also revealed that bad experiences are leading customers to switch providers. 22% of banking customer indicated having changed providers in the last 12 months, a figure that rises to 33% of wealth and insurance customers. Price competitiveness, curiosity and personalization were cited as the top reasons for changing providers to a newcomer.

Reasons for choosing a digital challenger, Source: The Future of Financial Services 2022, Salesforces

According to Salesforce report, there is an urgent need for incumbents to improve their customers’ journey. By leveraging data, banks can get a comprehensive view of a customer’s activities and profile, enabling them to serve their customers more efficiently with the services they prefer at a reduced cost, the report says.

This can be done by partnering with third-party providers, and fintech companies to get supplemental data. Banks can also seek out analytics and big data vendors who will help them draw critical insights from their data, ultimately helping them understand where their customers are struggling and dropping off in the journey.

Once financial institutions have better insights into the customer journey, they should partner with experts and services providers that will help them craft a sophisticated digital interface, and well-designed digital channels.

Finally, financial institutions should consider modernizing their core banking systems and partner up with infrastructure providers to set up a flexible back end, the report says.

Digital challengers gain ground

This past decade has seen a dramatic change in the financial services landscape with a new, wider industry emerging. In this landscape, bigtech, merchants as well as data and fintech firms are increasingly gaining ground, accounting now for more 35% of the aggregate financial services industry value, according to global management consulting firm Oliver Wyman.

The remaining 65% are held by incumbent players such as banks, insurance companies, and asset managers, a figure that has shrunk significantly over the past decade. Ten years ago, incumbents accounted for 90% of the total value of the industry.

Consulting firm Simon-Kucher estimates that there are currently close to 400 neobanks around the world, together serving one billion client accounts. China’s WeBank and Aibank are two of the world’s biggest digital challenger banks by number of users, combining about 2.2 billion users as of 2020. In Japan, Rakuten Bank is the largest digital challenger, counting about 100 million users as of 2020.

Brazil’s NuBank is another neobank worth mentioning, having amassed over 50 million customers in Latin America. Revolut, which is headquartered in the UK but which operates across 200+ countries and regions, claims 20 million personal users, and 500,000 business customers.

In June, Singapore welcomed its first digital bank, Green Link Digital Bank (GLDB). Owned by Chinese developer and state-owned enterprise Greenland Holdings, as well as supply chain financing platform Linklogis Hong Kong, GLDB was granted a digital wholesale bank license in 2020, allowing it to serve micro, small and medium-sized enterprises and non-retail clients in Singapore. The digital bank specializes in supply chain financing.

Featured image credit: Edited from Unsplash

- ant financial

- Banking

- blockchain

- blockchain conference fintech

- chime fintech

- coinbase

- coingenius

- crypto conference fintech

- customer behavior

- customer expectations

- Customer Journey

- fintech

- fintech app

- fintech innovation

- Fintechnews Singapore

- OpenSea

- PayPal

- paytech

- payway

- plato

- plato ai

- Plato Data Intelligence

- PlatoData

- platogaming

- razorpay

- Revolut

- Ripple

- square fintech

- stripe

- tencent fintech

- Virtual Banking

- xero

- zephyrnet