The Securities and Exchange Commission (SEC) approved a new rule mandating publicly traded companies to disclose their direct greenhouse gas emissions. The proposal received backing with 3 votes to 2 at a recent SEC meeting.

The newly passed legislation titled “The Enhancement and Standardization of Climate-Related Disclosures for Investors” also requires US-based companies to disclose details on their use of carbon offsets, including the associated costs if the credits contribute to their emissions reduction targets. They also need to describe how climate change impacts their operations, financial condition, and strategies.

Moreover, companies must explain the risks and how they’re managing them, such as the impact on revenue and expenses.

What Emission Scopes Are Mandated?

The original SEC proposal initially required companies to disclose their Scope 1, 2, and 3 emissions. But Scope 3, which garnered controversy, was ultimately excluded in the final rule.

Scope 1 refers to emissions directly emitted by the company while Scope 2 covers emissions from the fuel and energy purchased by the company. Whereas Scope 3 pertains to emissions generated by customers and suppliers.

Scope 1 and 2 emissions are mandatory to report on, provided the company considers the information “material” to investors. Having this vital climate-related information will give investors insights to come up with informed decision-making.

Scope 3 emissions were the subject of significant controversy due to the challenges associated with calculating indirect emissions, which impose the highest compliance costs on companies. Big companies, particularly those in the fossil energy sector, opposed this reporting requirement.

Thus, following an extensive public comment period, which garnered 4,500 letters and 24,000 comments, the requirement to disclose Scope 3 emissions was ultimately dropped.

For the past 2 years, the SEC has been deliberating on formulating standardized requirements for corporate climate disclosure. The goal is to establish a minimum standard for transparency in boardrooms.

Now, the increased transparency required on the use of offsets would influence future purchases of carbon credits.

According to the final rule, companies will now be obligated to provide a detailed breakdown of the costs associated with carbon credits. Specifically, the approved proposal mandated that:

“The capitalized costs, expenditures expensed, and losses related to carbon offsets and renewable energy credits or certificates (RECs) if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals, disclosed in a note to the financial statements…”

This disclosure requirement is one of 3 main categories of information mandated in the amendments to the SEC’s final rule.

Unpacking SEC New Rule’s Key Provisions

While it’s essential for every company to thoroughly understand the SEC’s official rule, spanning almost 900 pages, 3 key provisions stand out:

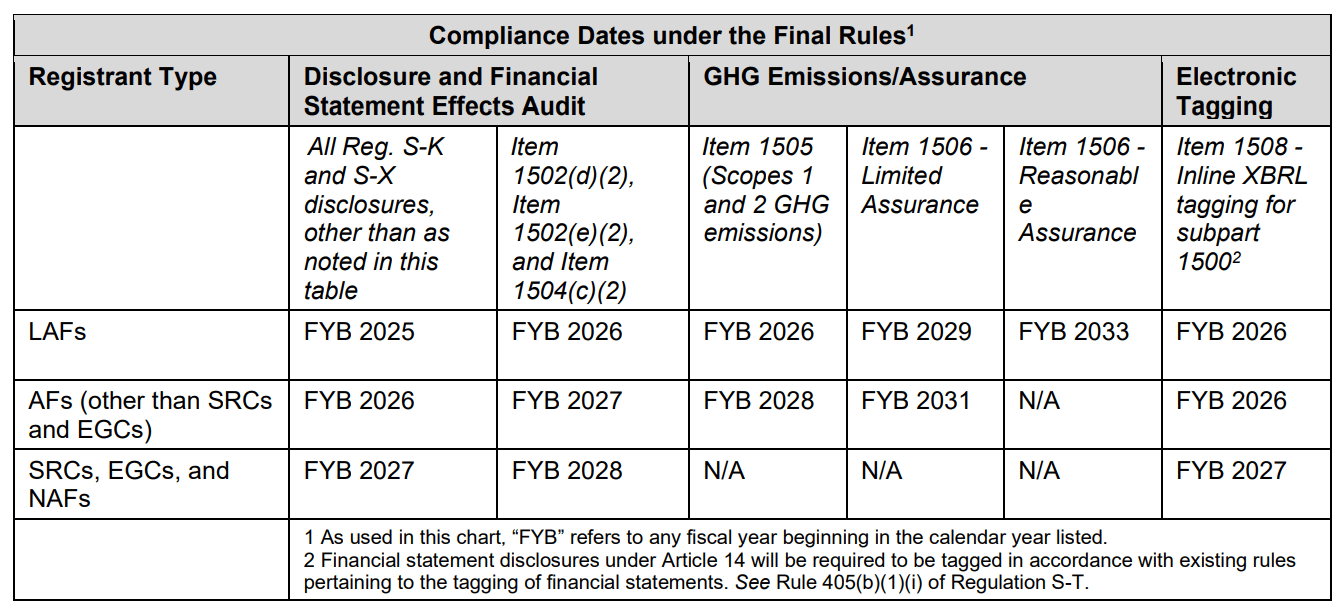

- “Accelerated filers,” which are companies with publicly traded shares valued at $75 million or more, are mandated to disclose Scope 1 and 2 emissions.

- Costs stemming from severe weather events and other natural disasters must be disclosed on financial statements.

- Companies are obligated to disclose both the actual and potential material impacts of climate-related risks on their strategy, business model, and outlook.

The SEC made a significant revision to its earlier draft by removing a requirement to disclose expenditures related to “general energy transition activities” in financial statements.

Instead, the final rule focuses specifically on disclosing expenditures related to carbon offsets and RECs, as confirmed by SEC officials.

Go over to SEC’s fact sheet that summarizes the specific rules that a registrant has to disclose.

The Commission estimates that around 2,800 companies have to prepare to report on their climate-related financial risks. That’s 40% of the 7,000 US public companies registered with the SEC.

Meanwhile, about 60% of the 900 SEC-registered foreign private issuers may also be subject to the new rule.

Accelerated filers, in particular, need to start disclosing their Scope 1 and Scope 2 emissions in 2026. Below are the compliance dates companies have to keep in mind based on their filer status:

Mixed Reactions: The Impact of SEC’s Climate Disclosure Rule

The new climate disclosure rule received both praise and criticism. Former SEC commissioner Allison Herren Lee commented that:

“The new rule, unfortunately, does little to prevent companies from making vague, untested and, most significantly, unsubstantiated, statements about their carbon footprints.”

On the other hand, supporters of the new rule noted that it’s a great milestone. For Lane Jost, head of ESG advisory at Edelman Smithfield,

“There is ample room to argue the validity of this rule on all sides, but regardless, this is a historic day for enhancing common, comparable, and credible disclosure rules on climate risks for investors and issuers.”

The SEC rule marks a significant addition to the expanding global regulatory landscape for corporate climate disclosures. International companies gear up to comply with Europe’s Corporate Sustainability Reporting Directive, which mandates climate disclosures. And with California’s carbon emissions disclosure requirements introduced last year, the SEC’s rule further underscores the increasing importance of climate-related transparency in corporate reporting.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://carboncredits.com/sec-finalizes-new-climate-disclosure-rule-heres-whats-new/

- :has

- :is

- $UP

- 000

- 1

- 2%

- 2026

- 24

- 4

- 500

- 7

- 800

- 900

- a

- About

- accelerated

- Achieve

- actual

- addition

- advisory

- All

- almost

- also

- amendments

- an

- and

- approved

- ARE

- argue

- around

- AS

- associated

- At

- backing

- based

- BE

- been

- below

- Big

- both

- Breakdown

- business

- business model

- but

- by

- calculating

- capitalized

- carbon

- carbon credits

- carbon emissions

- Carbon Offsets

- categories

- certificates

- challenges

- change

- Climate

- Climate change

- come

- comment

- commented

- comments

- commission

- commissioner

- COMMISSIONER ALLISON HERREN

- Common

- Companies

- company

- comparable

- compliance

- comply

- component

- condition

- CONFIRMED

- considers

- contribute

- controversy

- Corporate

- Costs

- covers

- credible

- Credits

- criticism

- Customers

- Dates

- day

- Decision Making

- describe

- detailed

- details

- direct

- directly

- disasters

- Disclose

- Disclosing

- disclosure

- Disclosures

- does

- draft

- dropped

- due

- Earlier

- emerging

- emission

- Emissions

- energy

- enhancement

- enhancing

- ESG

- essential

- establish

- estimates

- events

- Every

- exchange

- Exchange Commission

- excluded

- expanding

- expenses

- Explain

- extensive

- fact

- final

- finalizes

- financial

- Financial Condition

- focuses

- following

- For

- For Investors

- foreign

- formulating

- fossil

- from

- Fuel

- further

- future

- garnered

- GAS

- Gear

- generated

- Give

- Global

- goal

- Goals

- great

- greenhouse gas

- Greenhouse gas emissions

- Growth

- hand

- Have

- having

- head

- highest

- historic

- How

- HTTPS

- if

- Impact

- Impacts

- importance

- impose

- in

- Including

- increased

- increasing

- influence

- information

- informed

- initially

- insights

- International

- introduced

- Investors

- issuers

- ITS

- Keep

- Key

- landscape

- Lane

- Last

- Last Year

- Lee

- Legislation

- little

- losses

- made

- Main

- Making

- managing

- mandates

- mandating

- mandatory

- material

- max-width

- May..

- meeting

- milestone

- million

- mind

- minimum

- model

- more

- most

- must

- Natural

- Need

- New

- newly

- note

- noted

- now

- of

- official

- officials

- offsets

- on

- ONE

- Operations

- opposed

- or

- original

- Other

- out

- Outlook

- over

- pages

- particular

- particularly

- passed

- past

- period

- plans

- plato

- Plato Data Intelligence

- PlatoData

- potential

- praise

- Prepare

- prevent

- private

- proposal

- provide

- provided

- public

- public companies

- publicly

- purchased

- purchases

- reactions

- received

- recent

- reduction

- refers

- Regardless

- registered

- regulatory

- regulatory landscape

- related

- removing

- report

- Reporting

- required

- requirement

- Requirements

- requires

- revenue

- risks

- Room

- Rule

- rules

- scope

- SEC

- SEC Commissioner

- sector

- Securities

- Securities and Exchange Commission

- severe

- Shares

- Sides

- significant

- significantly

- smaller

- spanning

- specific

- specifically

- stand

- standard

- standardization

- standardized

- start

- statements

- Status

- strategies

- Strategy

- subject

- such

- suppliers

- supporters

- Sustainability

- targets

- that

- The

- the information

- their

- Them

- they

- this

- thoroughly

- those

- titled

- to

- traded

- transition

- Transparency

- true

- Ultimately

- underscores

- understand

- unfortunately

- untested

- us

- use

- used

- validity

- valued

- vital

- votes

- was

- Weather

- were

- whereas

- which

- while

- will

- with

- would

- year

- years

- zephyrnet