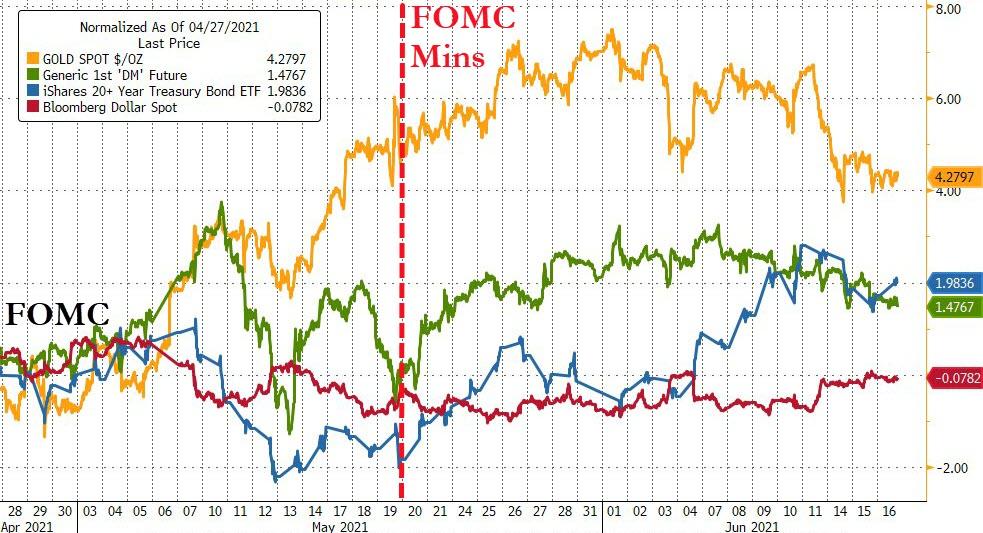

Since the April 28th FOMC meeting, gold is the strong outperformer while the dollar is unchanged. Bonds and stocks are up about the same (1.5-2%)…

Source: Bloomberg

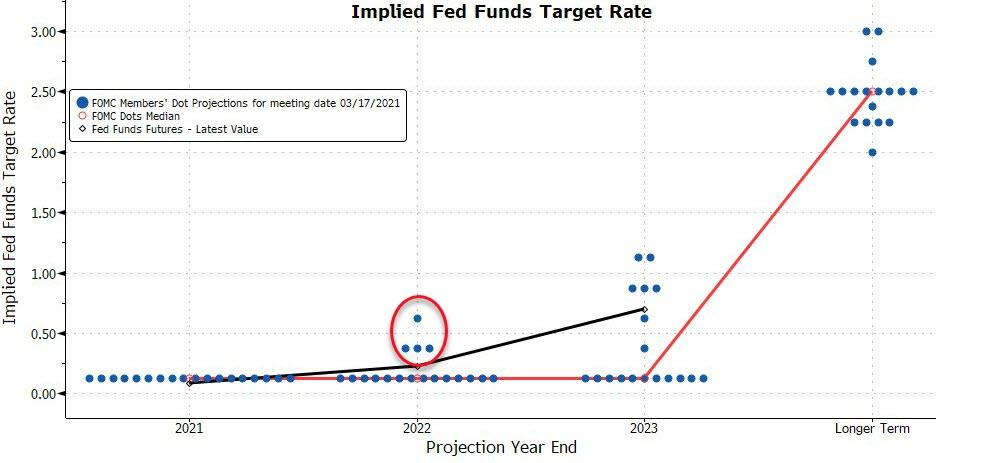

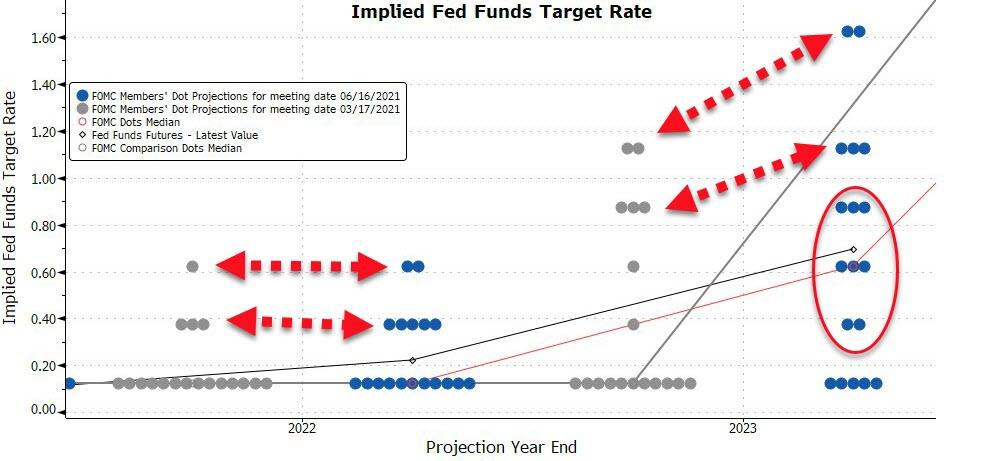

At the March meeting, only 4 FOMC members saw a rate hike in 2022…

Source: Bloomberg

The market is about 50-50 in its guess for a 2022 rate-hike (notably less than at the last April 28th FOMC meeting)…

Source: Bloomberg

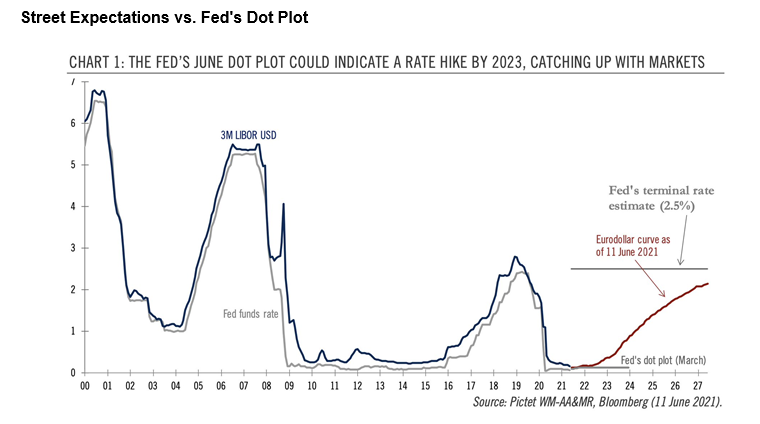

Finally, we note that the longer-term expectations of the market are significantly divergent (and more hawkish) from The Fed’s…

So what will The Fed do?

The big question is the 2023 Fed Funds dot plot (and whether it will be adjusted enough to shift the median expectation to a rate-hike).

The other thing to focus on – frankly ignoring the words of the statement – is whether the 2023 PCE projection is increased from March’s 2.1% forecast, which could spook the market’s faith in The Fed’s view that the inflation spike is transitory.

And what will Powell say about the stagflationary onset that is cornering him?

Source: Bloomberg

We do note that stocks were at the lows of the day ahead of the statement…

And here’s what happened:

The Fed keeps benchmark rates and the pace of bond-buying unchanged but the biggest shift is a hawkish tilt to its rate forecasts as Fed median projections show 2 rate-hikes by end-2023 and 7 FOMC members see a hike in 2022…

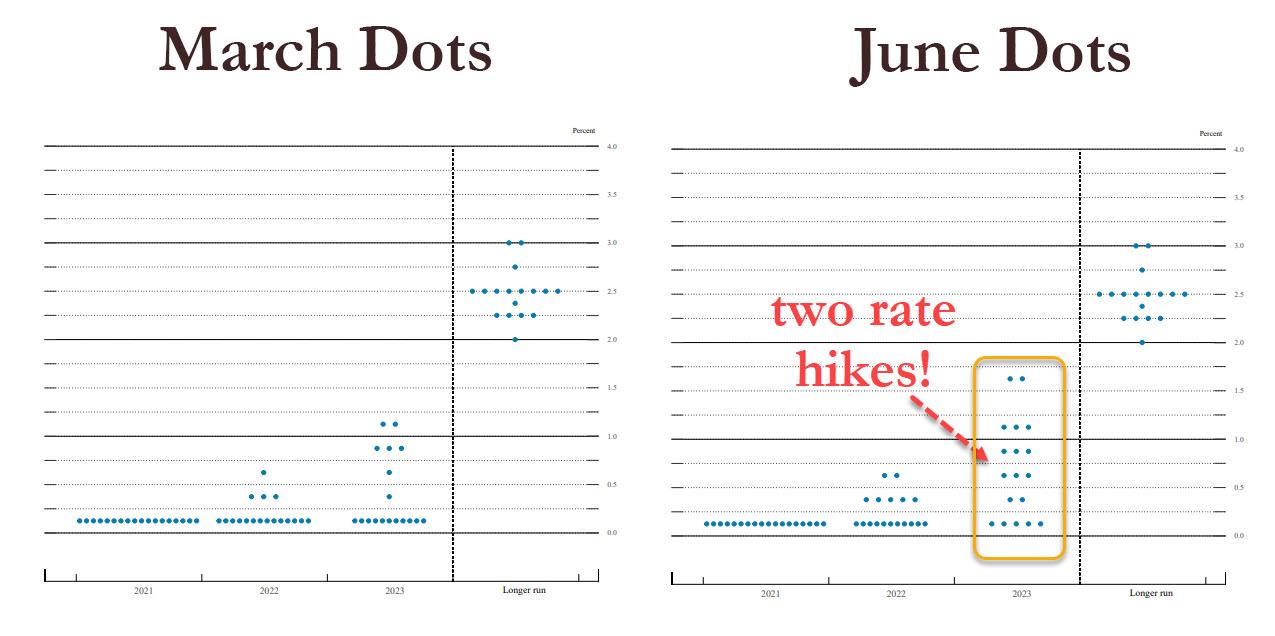

Another way of seeing the critical difference in the dot plot between March and today: from 0 median rate hike in 2023 to two! Guess that inflation was transitory after all…

For those confused by the rorshach above, the 2023 median dot was a lot higher; in fact, only five members had rates unchanged up from 11 in march, and the median is now 0.625%, higher than anyone was reasonably expecting! That said, the sheer dispersion of dots in 2023 suggest that this is a Fed that doesn’t really know what the outlook looks like. In other words, the “median of 2 hikes” in ’23 a byproduct of a lot of different views (on hawkish/dovish side). This is not a clear message to markets, and can easily change as soon as there is a deflationary whiff in the economy.

The fact that the Fed now sees 2 hikes in 2023 suggests FOMC has shifted quite a bit more hawkish. This, as FX strategist Viraj Patel notes, will be seen as dollar positive & sets up Aug Jackson Hole taper announcement. That said, a lot rides on US data (esp next few jobs print), which is why Powell may talk down the hawkish reaction during the Q&A.

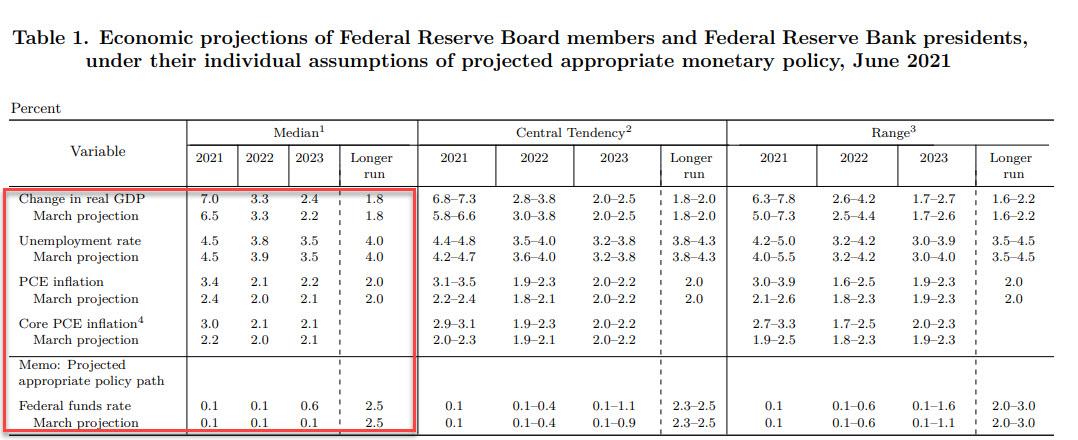

Next, looking at the Fed’s forecast, there was no unnecessarily dovish indication of a higher unemployment in 2023, which was left unchanged in the latest projection. What did change was a slight increase in 2023 GDP, from 2.2% in march to 2.4% in June, while PCE inflation also rose from 2.1% to 2.2%, giving the Fed some leeway to forecast 2 rate hikes in 2023.

Elsewhere, the reverse repo fiasco has finally been addressed by the Fed: given the massive excess in usage in the Fed’s RRP facility – which today saw well over $500BN in usage again – the Fed hiked IOER by 5 bps to 0.15% from 0.10%, as about half the banks had expected it would do. And to keep the corridor parralel, it also raised the Reverse Repo rate by 5bps from 0% to 0.0%.

The Board of Governors of the Federal Reserve System voted unanimously to set the interest rate paid on required and excess reserve balances at 0.15 percent, effective June 17, 2021. Setting the interest rate paid on required and excess reserve balances 15 basis points above the bottom of the target range for the federal funds rate is intended to foster trading in the federal funds market at rates well within the Federal Open Market Committee’s target range and to support the smooth functioning of short-term funding markets.

* * *

Conduct overnight reverse repurchase agreement operations at an offering rate of 0.05 percent and with a per-counterparty limit of $80 billion per day; the per-counterparty limit can be temporarily increased at the discretion of the Chair.

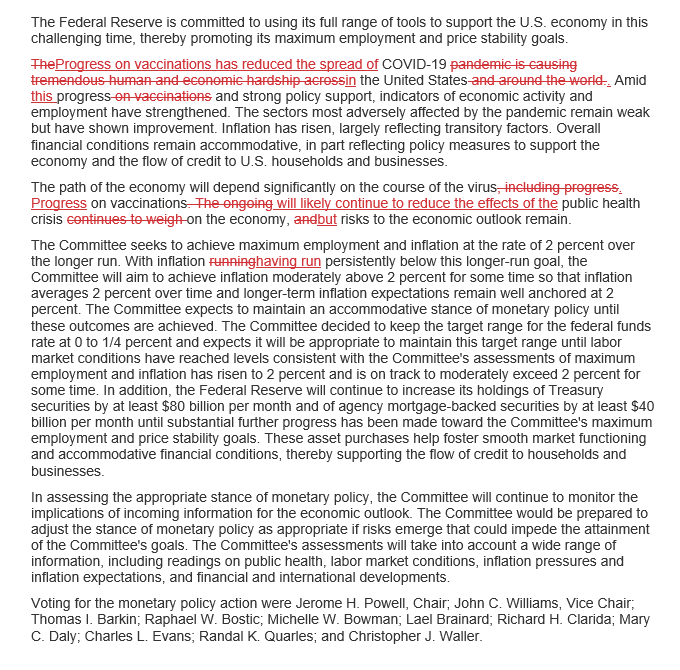

Looking at the Fed’s full statement reveals very few changes from March, although Bloomberg does note a slight change in the language on the pandemic and economic risks — a slightly more positive tone.

Today:

“Progress on vaccinations will likely continue to reduce the effects of the public health crisis on the economy, but risks to the economic outlook remain.”

April:

“The ongoing public health crisis continues to weigh on the economy, and risks to the economic outlook remain.”

Here is the full statement redlined:

What happens next?

- &

- 11

- 2021

- 7

- Agreement

- All

- Announcement

- April

- Banks

- Benchmark

- Biggest

- Billion

- Bit

- Bloomberg

- board

- Bonds

- change

- continue

- continues

- crisis

- data

- day

- DID

- Dollar

- Economic

- economy

- Facility

- Fed

- Federal

- federal reserve

- Finally

- Focus

- full

- funding

- funds

- FX

- GDP

- Giving

- Gold

- Health

- here

- HTTPS

- image

- Increase

- inflation

- interest

- IT

- Jobs

- language

- latest

- March

- Market

- Markets

- Members

- offering

- open

- Operations

- Other

- Outlook

- pandemic

- public

- public health

- Q&A

- range

- Rates

- reaction

- reduce

- reverse

- sees

- set

- setting

- shift

- Statement

- Stocks

- support

- system

- Target

- Trading

- unemployment

- us

- View

- weigh

- within

- words