For years, the ECB would kill for prices to turn higher and reach, if not surpass, its inflation target of 2.0%. And let’s not even talk about economic growth: ever since the global financial crisis, it seemed as if the old continent is stuck in a slow, miserable debt trap whose eventual outcome is the economic disaster that is Japan.

But things have changed fast, and according to the latest data, the euro zone economy continued to boom over the summer as activity rebounded after coronavirus lockdowns. However, a problem has emerged: inflation has blown past expectations, leaving the European Central Bank with a growing policy headache.

First, the good news: growth soared as consumers return to stores and venues but many businesses have been unable to keep up with demand, putting further pressure on prices already being driven higher by the rising cost of commodities. The economy of the 19 countries sharing the euro expanded by a bigger-than-forecast 2.2% in the third quarter, its fastest pace in a year and putting it on course to reach its pre-crisis size before the end of the year.

Today’s data were marginally stronger than consensus expectations of 2.1%, with stronger prints than expected in France and Italy, but weaker increases in Germany and (especially) Spain. Here is a breakdown of Europe’s strong growth at the regional level:

- Euro area GDP (Q3, first estimate): +2.2% vs. GS +1.8%, consensus +2.1%; previous +2.1% (unrevised)

- German GDP (Q3, first estimate): +1.8% vs. GS +1.9%, consensus +2.2%; previous +1.9% (revised +0.3pp)

- French GDP (Q3, first estimate): +3.0% vs. GS +2.0%, consensus +2.3%; previous 1.3% (revised +0.2pp)

- Italian GDP (Q3, first estimate): +2.6% vs. GS +1.8%, consensus +1.9%; previous +2.7% (unrevised)

- Spain GDP (Q3, first estimate): +2.0% vs. GS +2.9%, consensus +2.7%; previous +1.1% (unrevised)

Unfortunately, in its commentary to the GDP print, Goldman wrote that “looking ahead, we expect the pace of sequential growth to slow in Q4 across the Euro area to around 1%, given less ‘catch-up’ potential, softening survey data, near-term supply-side constraints, and the drag from the energy crisis and lower foreign demand.”

That’s not the bad news.

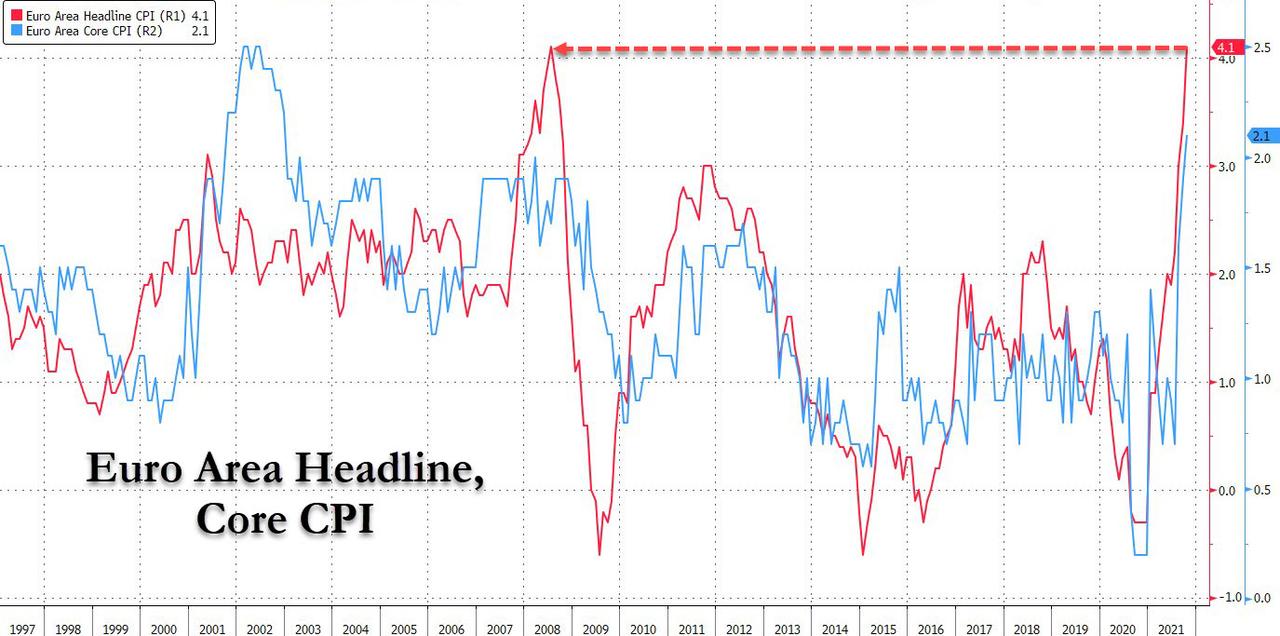

The bigger problem is that while the growth burst is certainly transitory, the roaring inflation may not be. Because between the surge in growth and soaring oil and gas prices, Eurozone headline inflation exploded 4.1% this month, more than twice the European Central Bank’s target and matching the all-time-high for the data series launched in 1997.

While inflation was mostly driven by higher energy prices and tax hikes, growing price pressures from supply bottlenecks were also visible in rising prices for services and industrial goods – a worry for the ECB, which is slowly accepting that price growth may be more durable than once thought. Core inflation, which excludes volatile food and energy costs yet which are just as critical to Europe’s households especially with winter approaching for a continent gripped by a historic energy crisis, rose 2.1%, the highest in two decades.

Unfortunately for Europe, this economic “golden quarter” is unlikely to last as the economy is hitting speed bumps as supply shortages, a scarcity of labor and the resurgence of coronavirus infections thwarts output.

“Growth will be much slower in the final quarter as supply chain disruption, slowing global demand and some labor shortages hamper production,” Andrew Kenningham at Capital Economics said.

A bigger question is what happens to inflation. According to Reuters “inflation is also likely to ease, although there is growing uncertainty over how fast and how far.” Indicators suggest the decline will be slower than the central bank once thought, raising the risk that high prices, even if temporary, could become entrenched in wages and corporate pricing structures.

ECB President Christine Lagarde acknowledged on Thursday that supply disruptions would persist, but said inflation will fade back below the 2% target over the medium term, so that no policy response is required for now.

And here an even bigger problem has emerged as markets increasingly doubt Lagarde: rates markets are now pricing in a 10 basis point rate hike by July 2022 and another by next October. A week ago, markets were pricing in just one hike within 12 months and the change in expectations came even as Lagarde tried to push back those bets. 3M Euribor Dec 2022 futures have plunged, hinting at a surge in rate hike odds by the end of next year.

This may well be a self-inflicted wound by the ECB head: after all, during yesterday’s dovish ECB presser which Goldman described as “pushing back against inflation pricing”, things suddenly reverse when Yellen said that “it’s not for me to say” if markets are getting ahead of themselves, a comment that sent the euro to its strongest in a month. According to commentators, “this was no longer a rigid attempt to keep the euro and yields in check.” They said that this was reminiscent of “comments by Federal Reserve officials in late May in their initial attempt to carefully communicate the bank’s intent to taper.”

FX strategist such as Bloomberg’s Vassilis Karamanis were stumped by Lagarde’s odd phrasing:

A game-changing moment through a carefully selected choice of words? Or a communication error that dovish-leaning officials will look to talk back in coming days? I would have tended to think the latter, had Lagarde not explicitly said yesterday that she expects PEPP to finish at the end of March. According to officials familiar with the matter, policy makers were cautious about an outright pushback on rate hikes backfiring, given the high uncertainty around the outlook. I’ll buy that for now. But does it also mean that the Governing Council isn’t so sure about their transitory narrative after all? Or that markets have more of a carte blanche to bet their own way?

That said, not everyone is convinced that the ECB is losing control: “Headline inflation will likely recede from its current rate of 4.1% to close to 1.5% again in late 2022 as special factors fade,” Berenberg economist Holger Schmieding said. We thus look for the ECB to start raising rates in late 2023 rather than in 2022 already.”

And yet, adding to inflation concerns, an ECB survey of companies released on Friday showed over 30% of respondents expected supply constraints and higher input costs to last for another year or longer. A slightly lower percentage predicted difficulties would last another six to 12 months. Firms also reported “a scarcity of applicants” for jobs as people changed profession, country or lifestyle, which was likely to result in wage increases.

Other central banks around the world are already tightening policy or plan to do so soon by removing extraordinary stimulus put in place to combat the pandemic. In just the past week, short-term rates in Canada and Australia soared higher as the central banks reversed on their previous defense of low rates, and either pulled forward the date of the first rate hike – in the case of Canada – or effectively ended Yield Curve Control in the case of Australia.

So while the ECB is still refusing to concede that it is behind the curve on inflation, the market has already made up its mind and is pricing in higher rates by the end of 2022. And with the ECB losing control of the front-end, a clash between central banker models and the brutal reality of markets is coming, and it could have calamitous consequences for European asset prices.

Source: https://www.zerohedge.com/markets/ecb-loses-control-front-end-inflation-comes-scorching-hot

- "

- 11

- All

- AREA

- around

- asset

- Australia

- Bank

- Banks

- Bloomberg

- boom

- businesses

- buy

- Canada

- capital

- Central Bank

- Central Banks

- change

- coming

- Commentary

- comments

- Commodities

- Communication

- Companies

- Consensus

- Consumers

- Coronavirus

- Costs

- Council

- countries

- crisis

- Current

- curve

- data

- Debt

- Defense

- Demand

- disaster

- Disruption

- driven

- ECB

- Economic

- Economic growth

- Economics

- economy

- energy

- Euro

- Euro Zone

- Europe

- European

- European Central Bank

- Eurozone

- expects

- FAST

- Federal

- federal reserve

- financial

- financial crisis

- First

- food

- Forward

- France

- Friday

- Futures

- GAS

- GDP

- Germany

- Global

- goldman

- good

- goods

- Growing

- Growth

- head

- here

- High

- How

- HTTPS

- image

- industrial

- Infections

- inflation

- intent

- IT

- Italy

- Japan

- Jobs

- July

- labor

- latest

- Level

- lifestyle

- lockdowns

- March

- Market

- Markets

- medium

- months

- news

- Oil

- Oil and Gas

- Outlook

- pandemic

- People

- policy

- president

- pressure

- price

- pricing

- Production

- Rates

- Reality

- response

- Reuters

- reverse

- Risk

- selected

- Series

- Services

- shortages

- SIX

- Size

- Slowing

- So

- Spain

- speed

- start

- stimulus

- stores

- summer

- supply

- supply chain

- surge

- Survey

- Target

- tax

- temporary

- the world

- wage

- week

- within

- words

- world

- year

- years

- yellen

- Yield