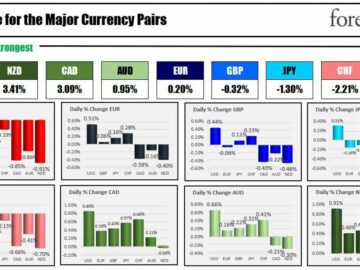

Despite

the late-month rebound, which was oddly supported by pessimistic data from the

United States, the stock market indexes ended August in the red: the S&P

500 fell by 1.52%, the Nasdaq by 1.58%, the Dow Jones by 2.62%, while the

Russell 2000 declined by 4.49%.

Turning

to the fixed-income market, 10-year Treasury yields in the U.S. and Europe

corrected from mid-month levels of +10% to +3.23% and +0.33%, respectively. In

addition, the Dollar Index rose by 1.47%, while EURUSD

fell by 1.37%. It’s not dramatic, but at least some movement.

What

or who is to blame for a short-lived market change?

Considering

the rise in assets since the beginning of the year, the groundwork for the

correction had already been laid. All that was needed was a catalyst, which the

rating agencies provided. First, analysts at Fitch downgraded the U.S. credit

rating from AAA to AA+.

Subsequently,

Moody’s downgraded ten U.S. banks with a delay of several

months and placed giants such as U.S. Bancorp and Truist on review. S&P

Global Rating followed suit with several regional banks in the country. Well,

better late than never.

To

provide some context, the downgrade in the first case was due to expectations

of worsening financial conditions over the next three years, the country’s

growing national debt, and budget deficits.

In

other words, the wave of problems will not dissipate soon.

As for

the banking sector, the sharp rise in interest rates is putting pressure on

many banks’ funding, liquidity, and profits. These factors have also

contributed to the devaluation of bank assets and an increased risk of

deteriorating asset quality.

Finally,

the decline in savings has had repercussions. Over the past two years,

total reserves in the United States have plummeted from $2.1 trillion in August

2021 to less than $200 billion. Simultaneously, household credit card debt

continues to rise, accompanied by increased delinquencies.

However,

not all pessimism has been detrimental to the markets.The decline in the

number of U.S. job openings in July to a 28-month low of 8.827 million, down

from 9.165 million in the previous month, and the downward revision of GDP to

2.1% from the previous 2.4% in the second quarter, have indeed encouraged

investors.

This

is due to the expectation that slowing economic growth will first impact

consumer demand and subsequently affect inflation. As a result, it is assumed

that the Federal Reserve will no longer need to raise interest rates.

Raphael

Bostic, the president of the Federal Reserve Bank of Atlanta, has expressed

opposition to further interest rate hikes in the United States, stating that

monetary policy is already sufficiently restrictive to bring inflation down to

2% within a “reasonable” timeframe.

No one

seems to consider that, even if monetary policy tightening ends, there is

little reason for optimism. Interest rates will remain high until the middle of

next year, while consumption could slow down due to the economic slowdown.

Keep

in mind that monetary policy operates with a long and variable lag. Analysts

believe that since the Fed began tightening policy just over a year ago, the

effects of the 525 basis point rate hikes may still take some time to manifest

themselves in the economy and markets fully.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- ChartPrime. Elevate your Trading Game with ChartPrime. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://www.forexlive.com/Education/the-outlook-for-the-us-economy-remains-uncertain-20230907/

- :has

- :is

- :not

- ][p

- 1

- 10-year Treasury yields

- 2%

- 2000

- 2021

- 500

- 8

- 9

- a

- AAA

- accompanied

- addition

- affect

- agencies

- ago

- All

- already

- also

- an

- Analysts

- and

- AS

- asset

- Assets

- assumed

- At

- Atlanta

- AUGUST

- Bancorp

- Bank

- Banking

- banking sector

- Banks

- basis

- basis point

- been

- began

- Beginning

- believe

- Better

- Billion

- bring

- budget

- but

- by

- card

- case

- Catalyst

- change

- conditions

- Consider

- consumer

- consumption

- context

- continues

- contributed

- corrected

- could

- country

- credit

- credit card

- data

- Debt

- Decline

- delay

- Demand

- Devaluation

- Dollar

- dollar index

- dow

- Dow Jones

- down

- Downgrade

- Downgraded

- downward

- dramatic

- due

- Economic

- Economic growth

- economy

- effects

- encouraged

- ended

- ends

- Europe

- Even

- expectation

- expectations

- expressed

- factors

- Fed

- Federal

- federal reserve

- Federal Reserve Bank

- financial

- First

- fitch

- followed

- For

- from

- fully

- funding

- further

- GDP

- giants

- Global

- groundwork

- Growing

- Growth

- had

- Have

- High

- Hikes

- household

- HTTPS

- if

- Impact

- in

- increased

- indeed

- index

- indexes

- inflation

- interest

- INTEREST RATE

- INTEREST RATE HIKES

- Interest Rates

- Investors

- IT

- Job

- jones

- jpg

- July

- just

- Late

- least

- less

- levels

- Liquidity

- little

- Long

- longer

- Low

- many

- Market

- Markets

- May..

- Middle

- million

- mind

- Monetary

- Monetary Policy

- Month

- months

- movement

- Nasdaq

- National

- Need

- needed

- never

- next

- no

- number

- oddly

- of

- on

- ONE

- openings

- operates

- opposition

- Optimism

- or

- Other

- Outlook

- over

- past

- pessimism

- pessimistic

- plato

- Plato Data Intelligence

- PlatoData

- Point

- policy

- president

- pressure

- previous

- problems

- profits

- provide

- provided

- Putting

- quality

- Quarter

- raise

- Rate

- rate hikes

- Rates

- rating

- Rating agencies

- reason

- reasonable

- rebound

- Red

- regional

- remain

- remains

- repercussions

- Reserve

- reserve bank

- reserves

- Restrictive

- result

- review

- Rise

- Risk

- ROSE

- s

- S&P

- Savings

- Second

- second quarter

- sector

- seems

- several

- sharp

- simultaneously

- since

- slow

- Slowdown

- Slowing

- some

- Soon

- States

- stating

- Still

- stock

- stock market

- Stock Market Indexes

- Subsequently

- such

- Suit

- Supported

- Take

- ten

- than

- that

- The

- the Fed

- themselves

- There.

- These

- three

- tightening

- time

- timeframe

- to

- Total

- TradingView

- treasury

- Treasury yields

- Trillion

- Truist

- two

- u.s.

- U.S. Bancorp

- U.S. economy

- Uncertain

- United

- United States

- until

- variable

- was

- Wave

- WELL

- which

- while

- WHO

- will

- with

- within

- words

- year

- years

- yields

- zephyrnet