The global flirtation with Buy Now Pay Later (BNPL) services seems to be coming undone, as new data on consumer payments unveils a significant drop in the appetite for this contentious credit payment approach.

BNPL experienced a surge and became the favourite of venture capitalists during lockdowns as e-commerce shoppers, idle at home, seized the opportunity of short-term finance to distribute the expense of both impromptu and deliberate online buys across several payments. Typically, the attraction of BNPL services were not charging any interest — a highly attractive offer for consumers who might otherwise bypass a discretionary online purchase, particularly amidst uncertain economic conditions.

In essence, BNPL services profit by levying charges on merchants for transaction processing and occasionally by imposing late fees or interest on customers who fail to pay punctually. This model enables them to provide versatile payment solutions to consumers whilst still earning income — and simplifying significant acquisitions.

Over recent years, this appealing proposition has underpinned a surge in BNPL companies globally, proving enticing in both advanced economies with high credit card usage looking for alternative finance, and in emerging nations where access to conventional credit was harder, particularly for the young and those in rural areas.

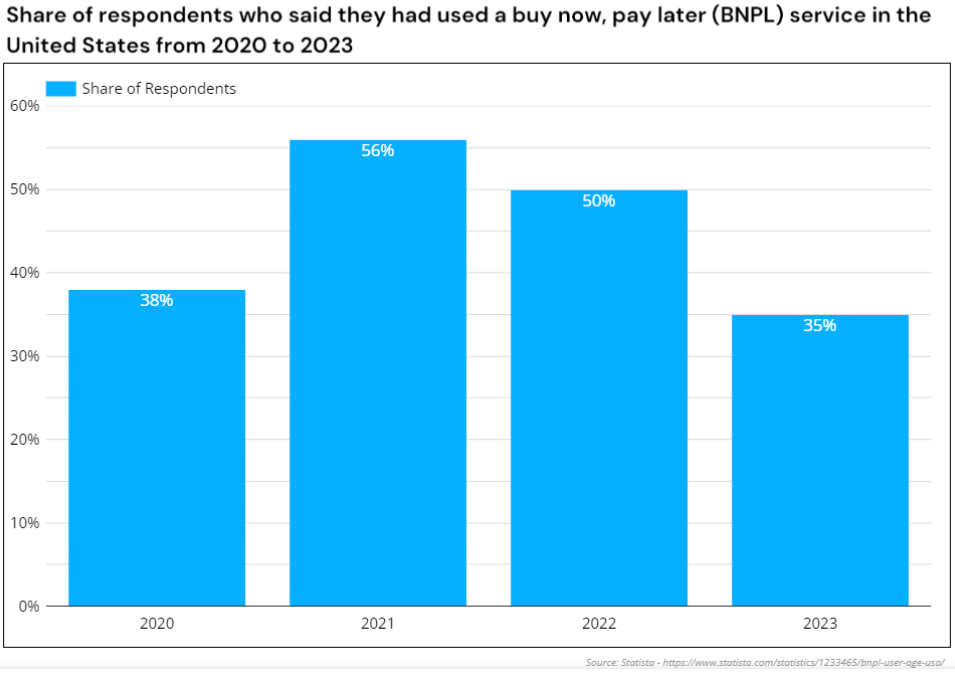

US BNPL users declined more in 2023 than the preceding years. Source: Statista

The Downslide for Asia Pacific’s BNPL Operators

However, the BNPL sector now seems to be in decline, with numerous BNPL services either retracting or ceasing operations altogether. Australia, hosting one of the globe’s foremost BNPL services, Afterpay, has observed this downturn since 2023.

Following the early February 2023 downfall of Australia’s Openpay, which left debts of AU$18.2 million, ZIP kicked off March 2023 by deciding to tighten financial controls and declared its withdrawal from India, the Philippines, Turkey, the Czech Republic, South Africa, Poland, Singapore, the UK, Mexico, and the Middle East.

Indeed, they withdrew from 10 of the 14 international markets they served. This decision, amid news of an AUD$240 million loss in 2022, was followed by a share value that nosedived 95% since Feb 2021 (previously trading at AU$12 compared to AU$0.5 in 2023).

The scenario appears equally bleak in Asia, where the adoption of BNPL and the emergence of new BNPL services seemed to occur practically overnight. For instance, Malaysian BNPL IOUpay was introduced on the Australian Stock Exchange (ASX) and proclaimed market dominance almost before its service commenced.

Within under two years, accusations of substantial fraud led to financial turmoil and a significant tarnish on its reputation. The saga intensified when IOUpay found that its former chief financial officer, Kenneth Kuan, had allegedly tampered with the company’s funds.

A suspected US$19 million was found to have been embezzled from the company between 2022 and 2023. Subsequently, IOUpay was forced into administration and has yet to recover.

The shopping and rewards platform ShopBack announced it would be terminating its BNPL offering, which was established in the wake of the firm’s acquisition of BNPL hoolah in November 2021, effective from March 2024 in Singapore and Malaysia.

When queried about remaining instalments, ShopBack highlighted the necessity of prompt payments for customers to avoid late fees. This response illustrates the fragility of the BNPL revenue model, and the thin profit margins when elevated investor estimations dissipate.

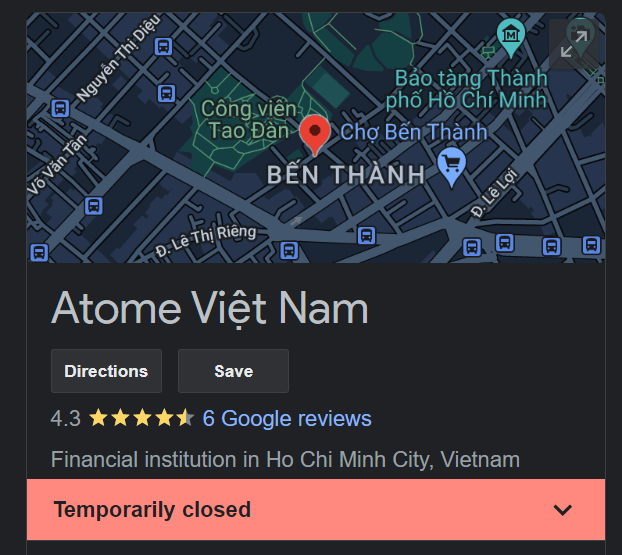

Atome Vietnam’s closure is likely for good. Source: Google

Concurrently, Atome launched in Vietnam in April 2022 to much acclaim, commencing with a trial involving over 20 retail partners. Within a year, Atome ceased its Vietnam operations, and local BNPL Ree-pay did not manage to bridge the void left by Atome as its offerings are inaccessible on numerous Vietnamese e-commerce platforms.

In May 2023, Trasy Lou Walsh, Atome’s regional general manager, resigned to become a co-founder and CEO at Fluid, a B2B payment firm. This was followed by CEO David Chen’s resignation in February 2024 to become Head of Consumer Lending at Indonesia’s GoTo Financial. Both ex-leaders of the once prominent Atome chose to exit the sector altogether — confidence in the BNPL services model appears to be low among key operators as it is among investors.

Singapore BNPL firm Pace also opted for voluntary dissolution in August 2023, attributing escalating debts as its rationale. Similar to Atome’s parent Advanced Intelligence Group and Temasek-backed ShopBack, Pace had previously secured 8-figure investments, yet these capital injections were insufficient to sustain the dwindling BNPL services.

Despite predictions of a 450% surge in usage by 2027 in the India BNPL market, ZestMoney, previously valued at $445 million, announced its closure after failing to secure a purchaser. After its founders left when acquisition talks with Indian fintech PhonePe fell through, ZestMoney was eventually sold to financial services firm DMI Group in January 2024 for rock bottom prices, with every investor losing money and DMI essentially using the buyout to poach Zest talent.

How Did BNPL Services Go Wrong?

The basic premise of BNPL in the developing world, which is to underwrite small ticket loans to emerging digital finance customers and thereby attracted many high-profile investors in process, was red-hot during stay-at-home periods and to onboard fledgling users to the digital economy.

But as interest rates rose, the status quo of BNPL rates was challenged, and unable to sustain in a less optimistic economic outlook. And it was not just in developing regions, with BNPL startups like Klarna, Affirm and Afterpay all facing substantial losses and loss of liquidity when investors pulled back from their earlier evaluations that were in the millions and billions of dollars.

The competition from traditional banking as well as financially well-resourced digital giants like Grab and Shopee in Southeast Asia, or Apple and PayPal in the US, also threatened the solvency of a lot of dedicated BNPL services who were unable to compete with their platform reach, outsized capital reserves, instantly recognisable brands, and large customer bases when they began integrating their own instalment payment programmes.

These platforms and super apps captured much of the market share that was the domain of BNPL-only startups, and could afford to offer loss-making ‘pay later’ features, which ultimately the dedicated providers could not keep up with.

Coupled with regulatory pressures in the nascent space, declining demand from users on tightening budgets, and increasingly diminishing returns from a business model that is ultimately based on impulse purchases, the momentum appears to be against BNPL startups and towards the consolidated platform operators who might be the true future of ‘buy now, pay later’.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/93168/lending/the-rise-and-fall-of-bnpl-is-the-due-date-near-for-pay-later-services/

- :has

- :is

- :not

- :where

- $UP

- 10

- 14

- 2%

- 20

- 2021

- 2022

- 2023

- 2024

- 250

- 300

- 32

- 5

- 95%

- a

- About

- access

- Accusations

- acquisition

- acquisitions

- across

- administration

- Adoption

- advanced

- Affirm

- afford

- africa

- After

- against

- All

- allegedly

- almost

- also

- alternative

- alternative finance

- altogether

- Amid

- amidst

- among

- an

- and

- announced

- any

- appealing

- appears

- appetite

- Apple

- approach

- apps

- April

- ARE

- areas

- AS

- asia

- ASX

- At

- Atome

- attracted

- attraction

- attractive

- AUGUST

- Australia

- Australian

- avoid

- B2B

- back

- Banking

- based

- basic

- BE

- became

- become

- been

- before

- began

- between

- billions

- BNPL

- both

- Bottom

- brands

- BRIDGE

- Budgets

- business

- business model

- buy

- buy now pay later

- buy now pay later (BNPL)

- Buyout

- Buys

- by

- bypass

- capital

- capitalists

- caps

- captured

- card

- ceo

- challenged

- charges

- charging

- chief

- chief financial officer

- chose

- closure

- Co-founder

- coming

- commencing

- Companies

- company

- Company’s

- compared

- competition

- conditions

- confidence

- consumer

- Consumers

- contentious

- controls

- conventional

- could

- credit

- credit card

- customer

- Customers

- Czech

- czech republic

- data

- Date

- David

- Deciding

- decision

- declared

- Decline

- Declining

- dedicated

- Demand

- developing

- developing world

- DID

- digital

- Digital economy

- digital finance

- diminishing

- discretionary

- distribute

- dollars

- domain

- Dominance

- downfall

- Drop

- due

- during

- e-commerce

- e-commerce platforms

- Earlier

- Early

- Earning

- East

- Economic

- Economic Conditions

- economies

- economy

- either

- elevated

- emergence

- emerging

- enables

- enticing

- equally

- escalating

- essence

- essentially

- established

- Ether (ETH)

- evaluations

- eventually

- Every

- exchange

- Exit

- expense

- experienced

- FAIL

- failing

- Fall

- Features

- Feb

- February

- Fees

- finance

- financial

- financial services

- financially

- Finextra

- fintech

- Firm

- followed

- For

- For Consumers

- forced

- foremost

- Former

- found

- founders

- fragility

- fraud

- from

- funds

- future

- General

- giants

- Global

- Globally

- Go

- good

- GoTo

- Group

- had

- harder

- Have

- head

- High

- high-profile

- Highlighted

- highly

- Home

- hosting

- HTTPS

- Idle

- illustrates

- imposing

- in

- inaccessible

- Income

- increasingly

- india

- Indian

- Indonesia’s

- injections

- instance

- instantly

- insufficient

- Integrating

- Intelligence

- intensified

- interest

- Interest Rates

- International

- into

- introduced

- investor

- Investors

- involving

- IT

- ITS

- January

- jpg

- just

- Keep

- kenneth

- Key

- Klarna

- large

- Late

- later

- launched

- Led

- left

- lending

- less

- like

- likely

- Loans

- local

- lockdowns

- looking

- losing

- loss

- losses

- lou

- Low

- Malaysian

- manage

- manager

- many

- March

- March 2024

- margins

- Market

- Market Dominance

- market share

- Markets

- max-width

- May..

- Merchants

- Mexico

- Middle

- Middle East

- might

- million

- millions

- model

- Momentum

- money

- more

- much

- nascent

- Nations

- Near

- necessity

- New

- news

- November

- November 2021

- now

- numerous

- observed

- occasionally

- occur

- of

- off

- offer

- offering

- Offerings

- Officer

- on

- Onboard

- once

- ONE

- ongoing

- online

- Operations

- operators

- Opportunity

- Optimistic

- or

- otherwise

- Outlook

- over

- overnight

- own

- Pace

- particularly

- partners

- Pay

- payment

- payment solutions

- payments

- PayPal

- periods

- Philippines

- platform

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- Poland

- practically

- Predictions

- pressures

- previously

- Prices

- process

- processing

- Profit

- programmes

- prominent

- proposition

- provide

- providers

- proving

- purchase

- purchaser

- purchases

- Rates

- rationale

- reach

- recent

- recognisable

- Recover

- regional

- regions

- remaining

- Republic

- reputation

- reserves

- resigned

- response

- retail

- returns

- revenue

- Rewards

- rewards platform

- Rise

- Rock

- ROSE

- Rural

- Rural Areas

- saga

- scenario

- sector

- secure

- seemed

- seems

- seized

- served

- service

- Services

- several

- Share

- Shopback

- Shopee

- Shoppers

- Shopping

- short-term

- significant

- similar

- simplifying

- since

- Singapore

- small

- Solutions

- Solvency

- Source

- South

- South Africa

- southeast

- Southeast Asia

- Startups

- Status

- Still

- stock

- Stock Exchange

- Subsequently

- substantial

- Super

- super apps

- surge

- suspected

- Talent

- Talks

- than

- that

- The

- The Philippines

- the UK

- their

- Them

- thereby

- These

- they

- thin

- this

- those

- Through

- ticket

- tighten

- tightening

- to

- towards

- Trading

- traditional

- traditional banking

- transaction

- trial

- true

- Turkey

- two

- typically

- Uk

- Ultimately

- unable

- Uncertain

- under

- underpinned

- Unveils

- us

- Usage

- users

- using

- value

- valued

- venture

- versatile

- Vietnam

- vietnamese

- voluntary

- Wake

- was

- WELL

- were

- when

- which

- Whilst

- WHO

- with

- withdrawal

- within

- world

- would

- Wrong

- year

- years

- yet

- young

- zephyrnet

- zest

- Zip