As we navigate the evolving landscape of environmental action, the voluntary (verified) carbon market (VCM) stands at a crucial intersection. With 2023 marking a period of significant transition, we’ve witnessed the shift from the Kyoto Protocol’s Clean Development Mechanism (CDM) to the more dynamic Paris Agreement’s Article 6 market. This change brings both challenges and opportunities, reshaping the market’s future. Let’s take a look at the journey through the past year as set out in the Voluntary Carbon Market Developer Overview 2023/2024 report by Abatable and explore what lies ahead for this vital component of our global environmental strategy.

Drone view of a path in the Borneo Jungle, Malaysia. AI generated visual.

Drone view of a path in the Borneo Jungle, Malaysia. AI generated visual.

2023—A year of transition and challenges

The transition phase

The Abatable report highlights that 2023 stood as a testament to the VCM’s ability to adapt and evolve. The shift towards the Paris Agreement’s Article 6 heralded a new era of carbon trading, underpinned by a heightened awareness of both the challenges and opportunities that lie ahead. Despite the uncertainties, the market’s stakeholders have embraced the transition, viewing it as a pivotal step towards more robust, transparent, and impactful carbon trading mechanisms.

Read more: The interconnected world of carbon: exploring key carbon market concepts

Bright spots amidst turbulence

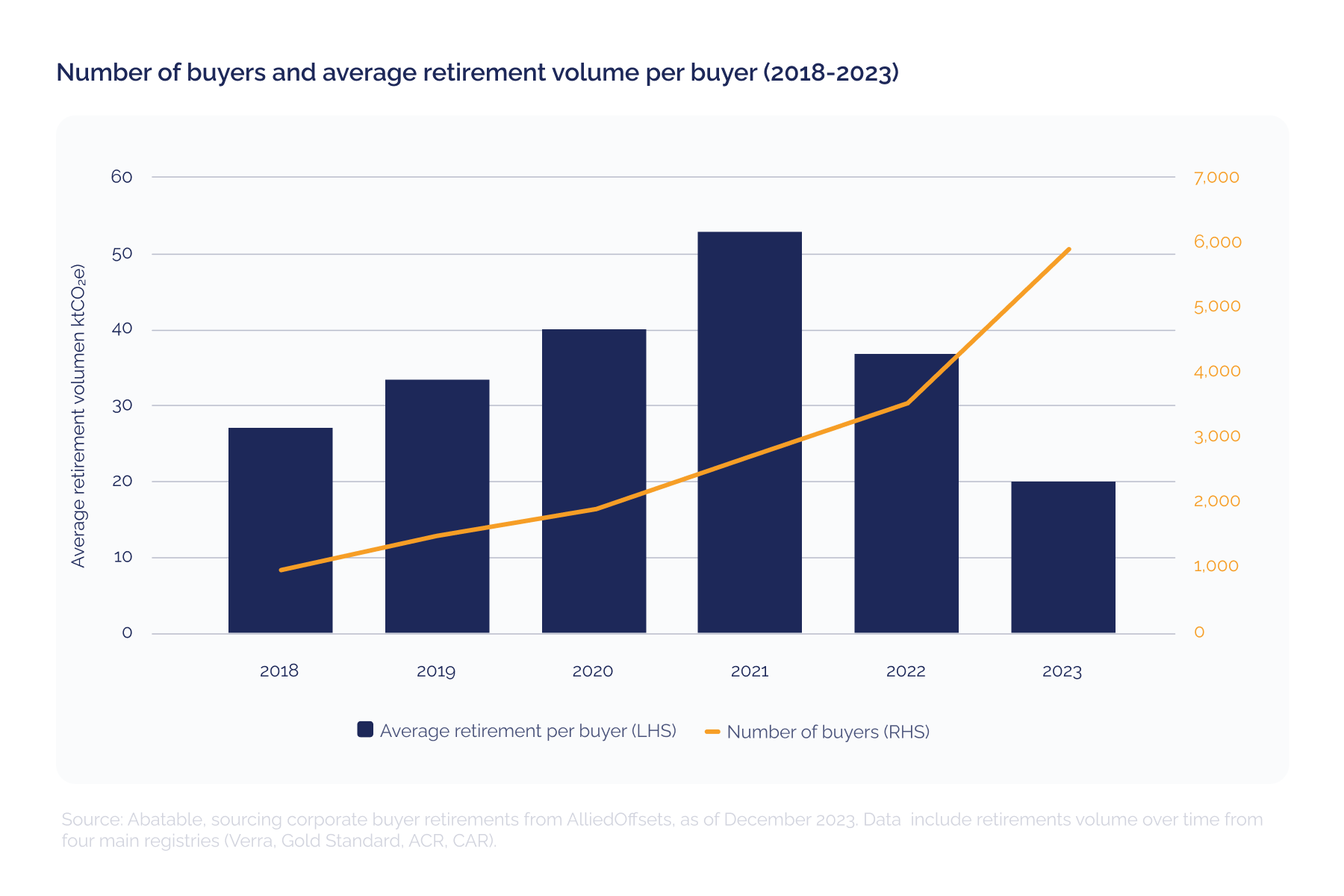

Despite facing challenges, including media scrutiny that questioned the credibility of carbon claims, the Voluntary Carbon Market (VCM) has shown remarkable resilience, states the Abatable report. Investments in the primary market have not only continued but thrived, reflecting a broader acceptance and understanding of its critical role in environmental sustainability. This growth is a testament to the market’s adaptability and the increasing recognition of its role in nature conservation. In 2023, a record number of unique buyers, representing a diverse range of industries, retired carbon credits for the first time, illustrating an expanding interest in the market. These first-time buyers, while starting with smaller transactions, signify a growing awareness and commitment to environmental responsibility. Key developers have responded by expanding their portfolios, diversifying into nature-based solutions, renewable energy, and more. This diversification highlights the dynamic nature of this sector and its ability to innovate and adapt to meet the evolving demands of buyers and the planet.

Number of buyers and average retirement volume per buyer (2018-2023)

Number of buyers and average retirement volume per buyer (2018-2023)

The two-track market evolution

The report notes that the VCM’s evolution is increasingly characterised by a two-track dynamic, with project developers moving at different speeds to adapt to new standards and market expectations.

The fast track: leading with agility and innovation

On the fast track, we find the trailblazers—developers who are rapidly adapting to the market’s evolving landscape. These developers are at the forefront of aligning their projects with the Carbon Offsetting and Reduction Scheme for International Aviation’s (CORSIA) eligibility requirements and the stringent environmental and social safeguards mandated by the Paris Agreement’s Article 6. Their projects are not just about generating carbon credits (carbon units); they’re about setting new benchmarks for quality, transparency, and impact. These developers are the pioneers, pushing the boundaries of what’s possible in carbon offsetting and in doing so, they are likely to reap the rewards of higher credit prices and stronger demand from discerning buyers seeking high-integrity offsets.

Carbon credit price dispersion across project types in 2023

Carbon credit price dispersion across project types in 2023

The steady track: moving with caution and consistency

Conversely, on the steady track, there are developers who are navigating the transition more cautiously. This group includes those sticking to a ‘business-as-usual’ approach, gradually adjusting to new market conditions and standards. They may not be at the cutting edge of the market’s shift towards higher quality and transparency, but they play an essential role in the ecosystem. These developers work within the frameworks they know, focusing on the steady generation of credits that, while they may not meet the highest new standards, still contribute to emissions reductions. The challenge for this group is to avoid being left behind as the market’s quality bar rises. They face the risk of their credits being valued less as the market increasingly differentiates on the basis of environmental integrity and impact.

Read more: Carbon pricing: global solutions for a global challenge

The implications of a two-speed market

This bifurcation presents both challenges and opportunities. For buyers, it means a more complex landscape to navigate, with a greater onus on due diligence and a focus on quality over quantity. For the market as a whole, this evolution could drive a push towards innovation, as developers on the steady track observe the benefits accrued by their fast-track counterparts and are thus incentivised to elevate their projects’ standards.

The transition towards a two-track market underscores the need for clear and accessible information on credit quality, project impact, and developer practices. This transparency is crucial for buyers and stakeholders to make informed decisions that align with their sustainability goals and values.

To bridge the gap between the two tracks, there’s a growing recognition of the need for collaboration across the market. Knowledge sharing, partnerships, and technological innovation can help elevate project standards across the board, ensuring that the market’s growth is both inclusive and sustainable.

As we look to the future, the VCM’s two-track evolution is a reflection of its dynamic nature. It’s a market that is both responding to and driving global efforts for nature conservation. The fast track highlights the market’s potential for innovation and high-integrity solutions, while the steady track represents the foundational role of carbon markets in supporting a broad range of emissions reduction projects. Together, these tracks form a diverse market landscape, one that is evolving to meet the complex challenges of our time.

The VCM’s journey through 2023 has laid bare the complexities and potential of carbon trading in a world that is increasingly focused on quality, transparency, and tangible impact. As we move into 2024, the market’s adaptability, driven by the innovative spirit of fast-track developers and the steady contributions of their counterparts, will continue to shape its trajectory, ensuring its vital role in the global climate action agenda.

Key themes and expectations for 2024

The Abatable report emphasises that the coming year is expected to see a significant divide in carbon credit pricing and quality. Credits meeting the Core Carbon Principles (CCP) and CORSIA criteria are likely to command a premium, reflecting their higher quality and compliance. This divergence underscores the market’s evolution towards emphasising quality and integrity in carbon trading.

Read more: Bullish growth projections in the carbon market

In 2021, according to BCG, the value of the VCM quadrupled from 2020, hitting the $2 billion mark. This surge underscores the growing significance of the VCM, which is expected to swell to a value of $10 billion to $40 billion by 2030. Such anticipated expansion reflects the market’s adaptation to growing carbon unit demands, driven by a rise in corporate commitments to net-zero emissions and the recognition of voluntary carbon units in regulatory frameworks like CORSIA.

2024 is poised to witness a surge in corporate commitments to biodiversity, driven by new regulations and the Task Force on Nature-related Financial Disclosures (TNFD). This trend highlights the growing recognition of the interconnectedness of environmental action and biodiversity preservation. Companies are increasingly looking to integrate carbon crediting with biodiversity initiatives, marking a significant shift in how we approach environmental sustainability.

Over the past decade, investments in carbon credit projects have gained significant traction, with a total of $36 billion funnelled into more than 7,000 projects from 2012 to 2022. This surge in investment, especially evident with $17 billion poured in from 2021 to 2023, illustrates the corporate sector’s growing dedication to carbon offsetting as a strategy to meet their environmental goals. In 2022 alone, the market received a boost of $7.5 billion, highlighting the rapid expansion pace.

Expectations are high for increased cooperation between developers and authorities, aiming for clearer regulations and streamlined authorisation processes. This collaboration, as emphasised in the Abatable report, is crucial for the market’s efficiency and integrity, facilitating smoother international trading and bolstering the market’s credibility.

The voluntary carbon market in numbers

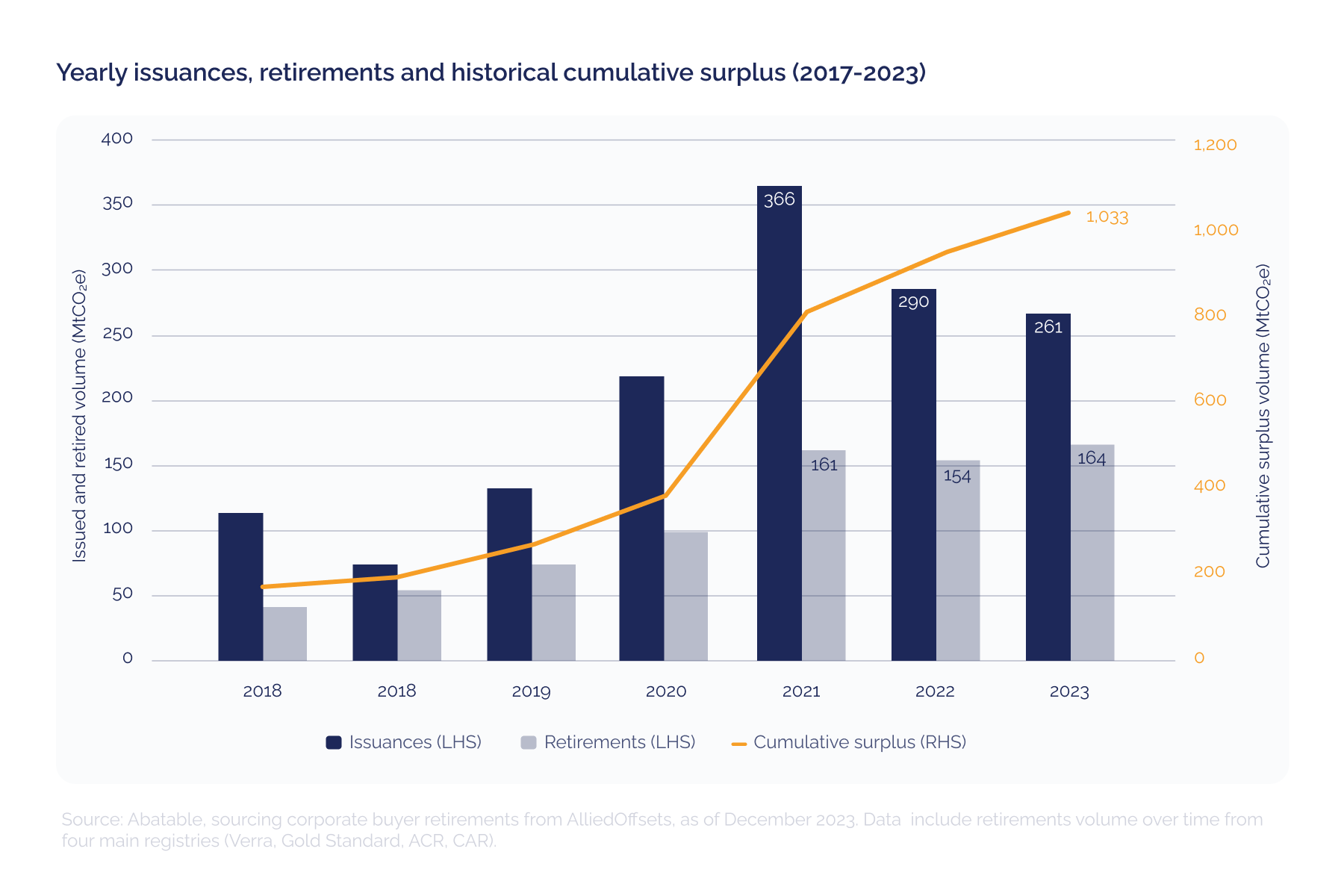

The Abatable report shows that the VCM in 2023 was characterised by a complex interplay of supply and demand factors, which together painted a nuanced picture of the market’s health and trajectory. A notable increase in the surplus of carbon credits was observed, a continuation of trends from previous years. This surplus, while indicating a robust pipeline of projects capable of generating credits, also led to a softening of prices across certain categories of credits, especially those associated with avoidance projects.

Yearly issuances, retirements and historical cumulative surplus (2017-2023)

Yearly issuances, retirements and historical cumulative surplus (2017-2023)

However, the narrative was not uniform across the board. Nature-based removal credits, which include projects like reforestation or improved forest management, bucked the trend by experiencing a price uptick. This was largely attributed to their limited supply coupled with strong demand, driven by buyers’ preference for credits with a direct impact on carbon removal from the atmosphere. The heightened demand for these credits underscores the market’s evolving preferences, with an increasing value placed on high-quality, impactful projects.

Read more: The rising demand for nature-based credits

The market also witnessed the entrance of over 100 new project developers in 2023, marking the fourth consecutive year of significant new entrant activity. This influx of developers not only reinforces the market’s vibrancy but also its diversity, introducing fresh ideas, methodologies, and projects into the mix. These new entrants are expanding the market’s reach, exploring untapped potentials for carbon reduction and removal across various sectors and geographies.

2023 marked a significant shift towards transparency within the VCM. A record number of buyers, ranging from multinational corporations to smaller entities, began disclosing their carbon credit purchases. This move towards openness is a critical step in building trust and accountability within the market, enabling stakeholders to better assess the real-world impact of carbon credit transactions. Such disclosures are pivotal in ensuring that the market’s growth aligns with its foundational goal of contributing to global environmental action.

The dynamics between buyers and developers have also been evolving, characterised by an increasing emphasis on transparency and diversity. The market’s growth has been accompanied by a broader recognition of the need for high-quality, verifiable credits that deliver tangible environmental benefits. Buyers are becoming more discerning, seeking credits that not only help offset emissions but also contribute to broader sustainability goals, including biodiversity conservation and social wellbeing.

The report shows that this increasing scrutiny and demand for quality are influencing developers, pushing them to innovate and adhere to higher standards of project development and reporting. As a result, the market is seeing a proliferation of projects that not only aim to reduce or remove carbon but also provide additional environmental and social benefits.

Explore the co-benefits of DGB’s nature-based projects

Looking forward to new avenues of innovation with DGB Group

Through the turbulence of 2023, the VCM has demonstrated its resilience and adaptability. As we move into 2024, the outlook is positive, with the market poised to play an even more crucial role in global environmental efforts. The agility and innovation of developers will be key in shaping the future of the market, underscoring the importance of quality, sustainability, and collaboration in driving forward our collective environmental goals. The journey of the VCM is far from over, but its direction is clear: towards a more integrated, effective, and sustainable approach to carbon trading and environmental action.

Read more: How to use DGB Group’s carbon footprint calculator on your journey to net zero

Initiatives rooted in nature are crucial for reaching net-zero goals as they capture and store carbon and are essential for ecosystem conservation and empowering communities. These efforts lead to sustainable and resilient solutions that greatly contribute to the global effort to protect the environment, playing a key role in the broadening scope and influence of carbon markets.

As the carbon markets expand and mature, the significance of nature-based solutions (NBS) becomes more pronounced. This expansion is fueled by an increasing demand for carbon credits, often produced by initiatives like reforestation. Such projects not only aid in meeting environmental objectives but also provide a practical means for individuals, organisations, and governments to participate in worldwide carbon reduction efforts. They are vital for rejuvenating ecosystems, protecting biodiversity, and improving the health and wellbeing of communities and the planet alike.

This positions DGB Group on the fast track as a leading carbon project developer. We are geared for substantial growth and impact. Through our NBS projects, we offer individuals, organisations, and investors the chance to tap into the carbon market and the escalating demand for quality carbon credits. We provide services to help you quantify, reduce, and compensate for your carbon footprint using verified, top-quality carbon credits.

Highlighting the transformative power of NBS and its role in enriching carbon markets can spark a shift towards a more sustainable and greener future. It’s crucial to recognise the significant impact these initiatives have, not just in reaching environmental targets but also in driving the growth of carbon markets. Investing in NBS with DGB allows you to minimise your environmental footprint and leverage the expanding carbon market, all while contributing positively to nature.

Partner with DGB and ignite real and meaningful change for nature

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.green.earth/blog/the-voluntary-carbon-markets-journey-through-2023-and-beyond

- :has

- :is

- :not

- 000

- 1

- 100

- 1800

- 2012

- 2020

- 2021

- 2022

- 2023

- 2024

- 2030

- 5

- 6

- 7

- 800

- a

- ability

- About

- acceptance

- accessible

- accompanied

- According

- accountability

- across

- Action

- activity

- adapt

- adaptability

- adaptation

- adapting

- Additional

- adhere

- adjusting

- agenda

- Agreement

- ahead

- AI

- Aid

- aim

- Aiming

- align

- aligning

- Aligns

- alike

- All

- allows

- alone

- also

- amidst

- an

- and

- Anticipated

- approach

- ARE

- article

- AS

- assess

- associated

- At

- Atmosphere

- authorisation

- Authorities

- avenues

- average

- aviation

- avoid

- awareness

- bar

- basis

- BCG

- BE

- becomes

- becoming

- been

- began

- behind

- being

- benchmarks

- benefits

- Better

- between

- Beyond

- Billion

- board

- bolstering

- boost

- both

- boundaries

- BRIDGE

- Brings

- broad

- broader

- Building

- but

- BUYER..

- buyers

- by

- CAN

- capable

- capture

- carbon

- carbon credits

- carbon footprint

- Carbon Reduction

- carbon trading

- categories

- caution

- cautiously

- ccp

- certain

- challenge

- challenges

- Chance

- change

- characterised

- claims

- clean

- clear

- clearer

- Climate

- climate action

- collaboration

- Collective

- coming

- commitment

- commitments

- Communities

- Companies

- compensate

- complex

- complexities

- compliance

- component

- conditions

- consecutive

- CONSERVATION

- continuation

- continue

- continued

- contribute

- contributing

- contributions

- cooperation

- Core

- Corporate

- Corporations

- could

- counterparts

- coupled

- Credibility

- credit

- Credits

- criteria

- critical

- crucial

- cutting

- decade

- decisions

- dedication

- deliver

- Demand

- demands

- demonstrated

- Despite

- Developer

- developers

- developers work

- Development

- DGB

- different

- diligence

- direct

- direction

- Disclosing

- Disclosures

- Dispersion

- Divergence

- diverse

- diversification

- Diversity

- divide

- doing

- drive

- driven

- driving

- due

- dynamic

- dynamics

- ecosystem

- Ecosystems

- Edge

- Effective

- efficiency

- effort

- efforts

- ELEVATE

- eligibility

- embraced

- Emissions

- emphasis

- emphasised

- emphasising

- empowering

- enabling

- energy

- enriching

- ensuring

- entities

- entrance

- entrants

- Environment

- environmental

- Environmental Sustainability

- Era

- escalating

- especially

- essential

- Even

- evident

- evolution

- evolve

- evolving

- Expand

- expanding

- expansion

- expectations

- expected

- experiencing

- explore

- Exploring

- Face

- facilitating

- facing

- factors

- far

- FAST

- financial

- Find

- First

- first time

- Focus

- focused

- focusing

- Footprint

- For

- Force

- forefront

- forest

- form

- Forward

- foundational

- Fourth

- frameworks

- fresh

- from

- from 2021

- fueled

- future

- gained

- gap

- geared

- generated

- generating

- generation

- geographies

- Global

- goal

- Goals

- Governments

- gradually

- greater

- greatly

- Green

- greener

- Group

- Growing

- Growth

- Have

- Health

- heightened

- help

- High

- high-quality

- higher

- highest

- highlighting

- highlights

- historical

- hitting

- How

- HTTPS

- ideas

- Ignite

- illustrates

- illustrating

- Impact

- impactful

- implications

- importance

- improved

- improving

- in

- include

- includes

- Including

- Inclusive

- Increase

- increased

- increasing

- increasingly

- indicating

- individuals

- industries

- influence

- influencing

- influx

- information

- informed

- initiatives

- innovate

- Innovation

- innovative

- integrate

- integrated

- integrity

- interconnected

- interest

- International

- intersection

- into

- introducing

- investing

- investment

- Investments

- Investors

- IT

- ITS

- journey

- just

- Key

- Know

- knowledge

- Kyoto Protocol

- laid

- landscape

- largely

- lead

- leading

- Led

- left

- less

- let

- Leverage

- lie

- lies

- like

- likely

- Limited

- Look

- looking

- make

- Malaysia

- management

- marked

- Market

- market conditions

- Markets

- marking

- mature

- max-width

- May..

- meaningful

- means

- mechanism

- mechanisms

- Media

- Meet

- meeting

- methodologies

- minimise

- mix

- more

- move

- moving

- multinational

- NARRATIVE

- Nature

- Navigate

- navigating

- Need

- net

- net-zero

- New

- New Market

- notable

- Notes

- nuanced

- number

- objectives

- observe

- observed

- of

- offer

- offset

- offsets

- offsetting

- often

- on

- ONE

- only

- onus

- Openness

- opportunities

- or

- Organisations

- our

- out

- Outlook

- over

- overview

- Pace

- paris

- Paris Agreement

- participate

- partnerships

- past

- path

- per

- period

- picture

- pioneers

- pipeline

- pivotal

- placed

- planet

- plato

- Plato Data Intelligence

- PlatoData

- Play

- playing

- poised

- portfolios

- positions

- positive

- positively

- possible

- potential

- potentials

- poured

- power

- Practical

- practices

- preferences

- Premium

- presents

- preservation

- previous

- price

- Prices

- pricing

- primary

- principles

- processes

- Produced

- project

- projections

- projects

- proliferation

- pronounced

- protect

- protecting

- protocol

- provide

- provide services

- purchases

- Push

- Pushing

- quadrupled

- quality

- quantity

- Questioned

- range

- ranging

- rapid

- rapidly

- RE

- reach

- reaching

- real

- real world

- reap

- received

- recognise

- recognition

- record

- reduce

- reduction

- reductions

- reflecting

- reflection

- reflects

- regulations

- regulatory

- reinforces

- remarkable

- removal

- remove

- Renewable

- renewable energy

- report

- Reporting

- representing

- represents

- Requirements

- reshaping

- resilience

- resilient

- responding

- responsibility

- result

- retirement

- Rewards

- Rise

- Rises

- rising

- Risk

- robust

- robust pipeline

- Role

- rooted

- s

- safeguards

- scheme

- scope

- scrutiny

- sector

- Sectors

- see

- seeing

- seeking

- Services

- set

- setting

- Shape

- shaping

- sharing

- shift

- shown

- Shows

- significance

- significant

- signify

- smaller

- smoother

- So

- Social

- Solutions

- Spark

- speeds

- spirit

- spots

- stakeholders

- standards

- stands

- Starting

- States

- steady

- Step

- sticking

- Still

- stood

- store

- Strategy

- streamlined

- stringent

- strong

- stronger

- substantial

- such

- supply

- Supply and Demand

- Supporting

- surge

- surplus

- Sustainability

- sustainable

- Take

- tangible

- Tap

- targets

- Task

- task force

- technological

- testament

- than

- that

- The

- The Future

- their

- Them

- themes

- There.

- These

- they

- this

- those

- Through

- Thus

- time

- to

- together

- Total

- towards

- track

- tracks

- traction

- Trading

- trajectory

- Transactions

- transformative

- transition

- Transparency

- transparent

- Trend

- Trends

- Trust

- turbulence

- two

- types

- uncertainties

- underpinned

- underscores

- understanding

- unique

- unit

- units

- untapped

- use

- using

- value

- valued

- Values

- various

- Ve

- verifiable

- verified

- View

- viewing

- visual

- vital

- volume

- voluntary

- was

- we

- wellbeing

- What

- which

- while

- WHO

- whole

- will

- with

- within

- witness

- witnessed

- Work

- world

- worldwide

- year

- yearly

- years

- you

- Your

- zephyrnet