News: Suppliers

19 February 2024

For fourth-quarter 2023, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $173.9m, down 2% on $177.4m last quarter but up 13% on $153.8m a year ago. It is also near the top of the guidance range (which had been raised in mid-January from $155–175m to $165–175m), driven by growth in semiconductor applications.

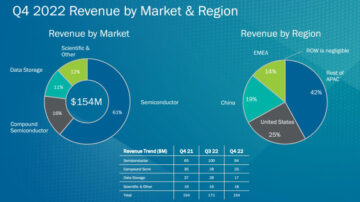

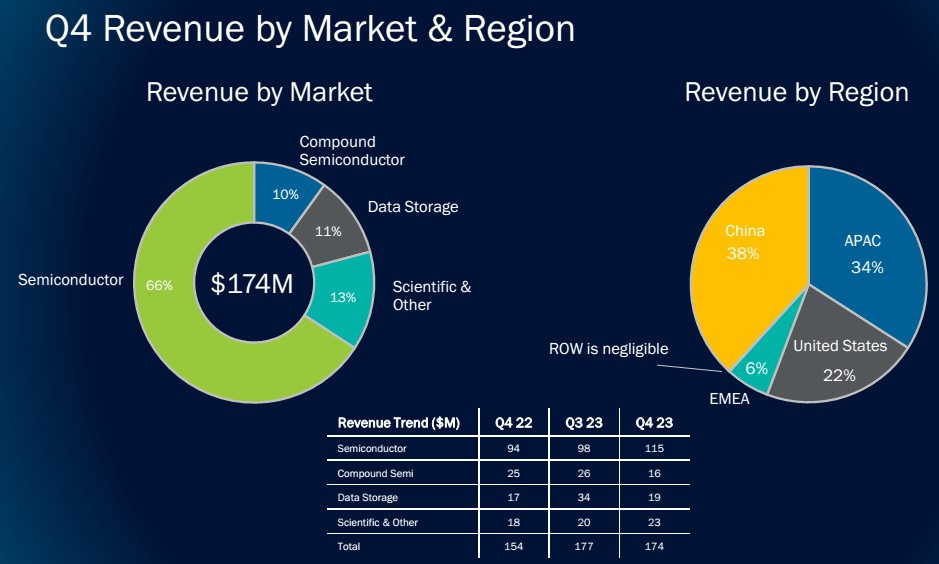

The Semiconductor segment (Front-End and Back-End, as well as EUV Mask Blank systems and Advanced Packaging) contributed a record $115m (66% of total revenue), up 17% on $98m (56% of revenue) last quarter and up 22.3% on $94m a year ago. “Our strong results included multiple laser annealing systems for advanced DRAM devices, despite industry-wide CapEx reductions, as well as our first HVM [high-volume manufacturing] laser annealing systems to our third leading logic customer,” says CEO Bill Miller. “We’ve also experienced increased demand from mature-node customers as they’ve achieved performance benefits from adopting laser annealing technology [at the 28nm node, and even the 40nm node].”

The Compound Semiconductor sector (Power Electronics, RF Filter & Device applications, and Photonics including specialty, mini- and micro-LEDs, VCSELs, laser diodes) contributed $16m (10% of total revenue), down on $26m (14% of revenue) last quarter and $25m (16% of total revenue) a year ago.

The Data Storage segment (equipment for thin-film magnetic head manufacturing) contributed $19m (11% of total revenue), almost halving from $34m (19% of revenue) last quarter but up on $17m a year ago.

The Scientific & Other segment (research institutions and other applications) has grown further, from $18m a year ago and $20m last quarter to $23m (13% of total revenue).

By region, China comprised 38% of revenue (rebounding from 23% last quarter and doubling from 19% a year ago) due to mature-node semiconductor sales. Led by sales to semiconductor customers, the Asia-Pacific (excluding China) rebounded from 29% of revenue last quarter to 34% (although this is still down on 42% a year ago). The USA comprised 22% of revenue (down on 33% last quarter), contributed mainly by data storage and semiconductor customers. Europe, Middle-East & Africa (EMEA) fell from 15% of revenue last quarter to just 6% of revenue.

Full-year revenue has grown by 3% from $646.1m in 2022 to $666.4m for 2023, near the top of the guidance range (which had been raised in mid-January from $648–668m to $658–668m).

This was driven primarily by Semiconductor revenue growing by 12% year-on-year – outperforming WFE (wafer fab equipment) market growth for the third consecutive year – from $369m (57% of total revenue) in 2022 to $413m (62% of total revenue) in 2023, led by laser annealing systems.

The Compound Semiconductor segment contributed $87m (13% of total revenue), down 14.7% on 2022’s $121m (19% of revenue), due primarily to a decrease in wet processing systems for 5G RF devices resulting fromsoftness in the handset market.

The Data Storage segment contributed $88m (13% of total revenue), level with 2022.

Scientific & Other contributed $78m (12% of total revenue), up 15% on 2022’s $68m (11% of total revenue) after shipping a large molecular beam epitaxy (MBE) research tool for making qubits for quantum computing applications.

By region, China comprised 33% of revenue (up from 2022’s 19%), driven by mature-node semiconductor sales (especially laser annealing). The Asia-Pacific (excluding China) fell from 36% to 31% of revenue, with most of that coming from semiconductor customers. The USA fell further, from 31% to 24% of revenue, mostly from data storage and semiconductor customers. EMEA fell from 14% to 12% of revenue.

“Veeco reported another year of top and bottom line growth, with results coming in near or above the high end of our updated 2023 guidance,” notes Miller. “Our team’s execution allowed us to grow non-GAAP gross margin, operating income, and EPS.”

Benefitting from higher volume and a favorable product mix, gross margin (on a non-GAAP basis) has risen further, from 42.3% a year ago and 44.2% last quarter to 45.4% (exceeding the expected 43–44%). Full-year gross margin hence rose from 41.9% in 2022 to 43.5% for 2023.

Quarterly operating expenses have increased further, from $41.3m a year ago and $45.7m last quarter to $46.9m. Full-year operating expenses have hence risen by 5% from $171.2m in 2022 to $180.6m in 2023, as Veeco increased R&D investment.

Operating income was $32.1m in Q4/2023, down slightly from $32.7m the prior quarter but up on $23.8m a year ago. Full-year operating income has hence risen by 10% from $99.8m for 2022 to $109.6m in 2023.

Quarterly net income was $29.8m ($0.51 per diluted share), down from $31m ($0.53 per diluted share) last quarter but up from $21.9m ($0.38 per diluted share) a year ago, and exceeding the guidance (which had been raised in mid-January from $0.35–0.45 to $0.40–0.45 per diluted share). Full-year net income has risen from $89.6m ($1.57 per diluted share) in 2022 to $98.3m ($1.69 per diluted share) for 2023, also exceeding the guidance (which had been raised from the initial $1.15–1.35 to $1.30–1.50 then $1.55–1.65, then again, in mid-January to $1.58–1.65).

Cash flow from operations has more than quadrupled from just $7m last quarter to $29m in Q4/2023. CapEx almost doubled from $6m to $11m in Q4 (raising full-year CapEx to $28m). During the quarter, cash and short-term investments hence rose by $19m from $287m to $306m.

Long-term debt remains $275m, representing the carrying value of $282m of convertible notes.

“We successfully grew the business, improved profitability, and most importantly, laid the groundwork for future growth by advancing our product roadmaps,” says Miller. “We achieved a significant milestone by shipping evaluation systems for two important core technologies. First, we launched our next-generation nanosecond annealing [NSA] solution. Second, we launched our ion beam deposition system for low-resistance metals. Each of these technologies enables our customer to fabricate devices with higher performance and lower power consumption,” he adds. “We continue to allocate capital towards organic growth initiatives. In the second half of 2023, we shipped multiple evaluation systems of key technologies [including four evaluation systems shipped in Q4/2023: two ion beam deposition systems for memory, and two nanosecond annealing systems for advanced logic] and expect to further the valuation program in 2024. We believe these investments will lead to significant served available market expansion.”

Outlook — investment in evaluation systems

For first-quarter 2024, Veeco expects revenue of $160–180m, down about 2% sequentially at the mid-point. The Semiconductor segment is expected to fall back slightly from Q4/2023’s record $115m to about $105m. Veeco is looking for “a bit of a rebound” in Compound Semiconductors, to about $25m, shipping a couple more systems, with some strength in photonics applications. Data Storage revenue is expected to rise to about $25m, due to shipping one more system. After shipping the very large research tool in Q4/2023, there should be a sizable drop off in Scientific & Other revenue in Q1/2024, to about $15m.

Gross margin is expected to fall back to 43–44%. “Gross margin improvement continues as a focus, with actions targeted to achieving our 45% target model in the future,” notes senior VP & chief financial officer John Kiernan.

With operating expenses of $46–48m, operating income should be $24–41m. Net income is expected to fall to $21–27m ($0.36–0.46 per diluted share).

Based on its current visibility, Veeco reiterates its full-year 2024 revenue outlook of $680–740m (about 6.5% growth on 2023, driven by 5–10% growth in both the Semiconductor and Compound Semiconductor segments, with the Data Storage segment flat to up 10%). China is expected to contribute about 30% of total revenue. “We expect revenue in the second half of the year to exceed revenue in the first half, based upon timing of scheduled shipments from our backlog, as well as forecasted orders,” notes Kiernan. “Mix might shift a little more towards the leading edge from the lagging edge in China,” adds Miller.

“With the Semiconductor market, we’re growing our served available market by investing in advanced-node logic and memory applications and winning new customers because LSA [laser spike annealing] technology is gaining share at customers’ advanced nodes as new device architectures and shrinking geometries require precise annealing to increase performance,” says Miller.

“Compound Semi this year in 2024 is going to be a year of investment for evaluations. We have four going out in Compound Semi: two in silicon carbide, one in GaN-on-silicon 300mm, and one in micro LED.… Veeco is focused on several long-term opportunities within power electronics and photonics,” says Miller.

“In power electronics, we’re actively working with a number of tier-1 customers in silicon carbide and are planning to place two evaluation systems in the field in 2024. We believe our unique system design and extensive go-to-market infrastructure position us well to capture share in this high-growth market. For GaN power, we are working with tier-1 power device customers and positioning ourselves at 200mm and 300mm wafer sizes for GaN-on-silicon solutions. We expect to ship a 300mm evaluation system to a power device customer in 2024. The fourth evaluation system we’re planning is actually in micro-LED, probably in the second half of 2024. So, we have a fair amount of new products we’re planning to put into the field in 2024.”

“We are making a significant investment with this evaluation program,” notes Kiernan. “Investments we’re making ahead of revenue is about 50–75 basis points [of gross margin] in 2024.” Full-year 2024’s gross margin is expected to be similar to 2023’s. “We are making margin improvements in other areas, but we are turning around and reinvesting that ahead of revenue in our evaluation program.”

Veeco continues to forecast diluted EPS of $1.60–1.90 for full-year 2024.

Veeco ships GEN20-Q MBE system to Taiwan’s Hermes-Epitek

Veeco’s Q3 revenue and profits exceed guidance

Veeco’s Q2 record semiconductor revenue drives growth

Veeco’s semiconductor-related revenue up 20% year-on-year in Q1

Veeco grows revenue 11% in 2022, despite 10.5% dip in Q4 driven by smartphone-related 5G RF weakness

Veeco acquires silicon carbide CVD system maker Epiluvac

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.semiconductor-today.com/news_items/2024/feb/veeco-190224.shtml

- :has

- :is

- $UP

- 10

- 14

- 15%

- 1M

- 2%

- 2022

- 2023

- 2024

- 22

- 35%

- 41

- 42

- 45

- 46

- 50

- 51

- 5G

- 6

- 65

- 90

- a

- About

- above

- achieved

- achieving

- Acquires

- actions

- actively

- actually

- Adds

- Adopting

- advanced

- advancing

- africa

- After

- again

- ago

- ahead

- allocate

- allowed

- almost

- also

- Although

- amount

- and

- Another

- applications

- architectures

- ARE

- areas

- around

- AS

- At

- available

- back

- Back-end

- based

- basis

- BE

- Beam

- because

- been

- believe

- benefits

- Bill

- Bill Miller

- Bit

- both

- Bottom

- business

- but

- by

- capital

- capture

- carrying

- Cash

- ceo

- chief

- chief financial officer

- China

- coming

- Compound

- Comprised

- computing

- consecutive

- consumption

- continue

- continues

- contribute

- contributed

- Core

- Couple

- Current

- customer

- Customers

- data

- data storage

- Debt

- decrease

- Demand

- Design

- Despite

- device

- Devices

- diluted

- Dip

- doubled

- doubling

- down

- driven

- drives

- Drop

- due

- during

- each

- Edge

- Electronics

- EMEA

- enables

- end

- equipment

- especially

- Ether (ETH)

- Europe

- evaluation

- evaluations

- Even

- exceed

- exceeding

- excluding

- execution

- expansion

- expect

- expected

- expects

- expenses

- experienced

- extensive

- fair

- Fall

- favorable

- February

- field

- filter

- financial

- First

- flat

- flow

- Focus

- focused

- For

- Forecast

- four

- Fourth

- from

- further

- future

- future growth

- gaining

- Go-To-Market

- going

- grew

- gross

- groundwork

- Grow

- Growing

- grown

- Grows

- Growth

- guidance

- had

- Half

- Halving

- Have

- he

- head

- hence

- High

- high-growth

- higher

- http

- HTTPS

- important

- importantly

- improved

- improvement

- improvements

- in

- In other

- included

- Including

- Income

- Increase

- increased

- Infrastructure

- initial

- initiatives

- institutions

- instruments

- into

- investing

- investment

- Investments

- IT

- items

- ITS

- John

- jpg

- just

- Key

- lagging

- laid

- large

- laser

- Last

- launched

- lead

- leading

- Led

- Level

- Line

- little

- logic

- long-term

- looking

- lower

- mainly

- maker

- Making

- manufacturing

- Margin

- Market

- mask

- Memory

- Metals

- micro

- might

- milestone

- Miller

- mix

- model

- molecular

- more

- most

- mostly

- multiple

- Near

- net

- New

- new products

- next-generation

- node

- nodes

- Notes

- nsa

- number

- NY

- of

- off

- Officer

- on

- ONE

- operating

- operating expenses

- Operations

- opportunities

- or

- orders

- organic

- Organic Growth

- Other

- our

- ourselves

- out

- Outlook

- outperforming

- packaging

- per

- performance

- Place

- planning

- plato

- Plato Data Intelligence

- PlatoData

- points

- position

- positioning

- power

- precise

- primarily

- Prior

- probably

- process

- processing

- Product

- Products

- profitability

- profits

- Program

- put

- Q2

- Q3

- quadrupled

- Quantum

- quantum computing

- quantum computing applications

- Quarter

- qubits

- R&D

- raised

- raising

- range

- record

- reductions

- region

- related

- remains

- Reported

- representing

- require

- research

- Research Institutions

- resulting

- Results

- revenue

- Rise

- Risen

- roadmaps

- ROSE

- s

- sales

- says

- scheduled

- scientific

- Second

- sector

- segment

- segments

- Semi

- semiconductor

- Semiconductors

- senior

- served

- several

- Share

- shift

- shipped

- Shipping

- ships

- short-term

- should

- significant

- Silicon

- silicon carbide

- similar

- sizable

- sizes

- slightly

- So

- solution

- Solutions

- some

- Specialty

- spike

- Still

- storage

- strength

- strong

- Successfully

- system

- Systems

- Target

- targeted

- team

- Technologies

- Technology

- than

- that

- The

- The Future

- then

- There.

- These

- they

- Third

- this

- this year

- timing

- to

- tool

- top

- Total

- towards

- Turning

- two

- unique

- updated

- upon

- us

- USA

- Valuation

- value

- Ve

- very

- visibility

- volume

- vp

- was

- we

- WELL

- which

- will

- winning

- with

- within

- working

- year

- zephyrnet