Key Takeaways:

- OCI enhances financial transparency and reveals how a company manages investments.

- It helps assess foreign exchange dynamics and their impact on shareholders’ equity.

- OCI aids in evaluating potential pension liabilities on unrealized profits.

- Distinguishing between P&L and OCI is crucial for understanding financial performance.

Have you recently thought about what other comprehensive income means exactly? How do you understand it as a true professional and start getting it without issues?

In corporate finance, OCI includes unrealized financial elements such as earnings, expenses, profits, and deficits.

Companies intentionally exclude these from the net income on their income statement. OCI serves as the equilibrium between net income and comprehensive income.

A common OCI example involves bonds in an investment portfolio not yet reaching maturity and awaiting redemption. Bond value fluctuations result in uncertain gains or losses, recognized in other comprehensive income until eventual sale.

Now, let’s examine the other comprehensive income and gain a deeper understanding from an expert’s viewpoint.

Exploring Other Comprehensive Income in Financial Reporting

Corporate financial statements offer a multifaceted view of a company’s financial health. FASB requires standardized metrics for investors and analysts to make it clear and understandable.

These metrics indicate a company’s status, including pension plans, earnings, gains and losses, equity, and cash flow hedges.

Understanding Other Comprehensive Income (OCI)

OCI, found on a company’s balance sheet, is akin to retained earnings but encompasses excluded items from net income. This mitigates income volatility due to unrealized gains/losses.

Key components include:

- Gains/Losses from Available-for-sale Investments

- Gains/Losses from Cash Flow Hedge Derivatives

- Foreign Currency Gains/Losses

- Pension Plan Gains/Losses

FASB’s Guideline: Statement of Financial Accounting Standards No. 220

FASB’s Statement No. 220, “Comprehensive Income,” gives guidelines for reporting comprehensive income in a structured way.

One financial statement displays this complete income, comprising two main parts: net income and OCI.

Distinguishing Accumulated Other Comprehensive Income

Within this context, it’s imperative to differentiate “accumulated other comprehensive income.” This component meticulously tracks unrealized gains and losses within OCI as they appear on a company’s balance sheet.

These unrealized gains or losses can originate from diverse sources, including cash flow hedges.

Other Comprehensive Income vs. Comprehensive Income

While “other comprehensive income” and “comprehensive income” may sound akin, they bear unique significance.

Comprehensive income represents a special combination of net income and other income. It provides a complete view of a company’s financial performance and its position in the market.

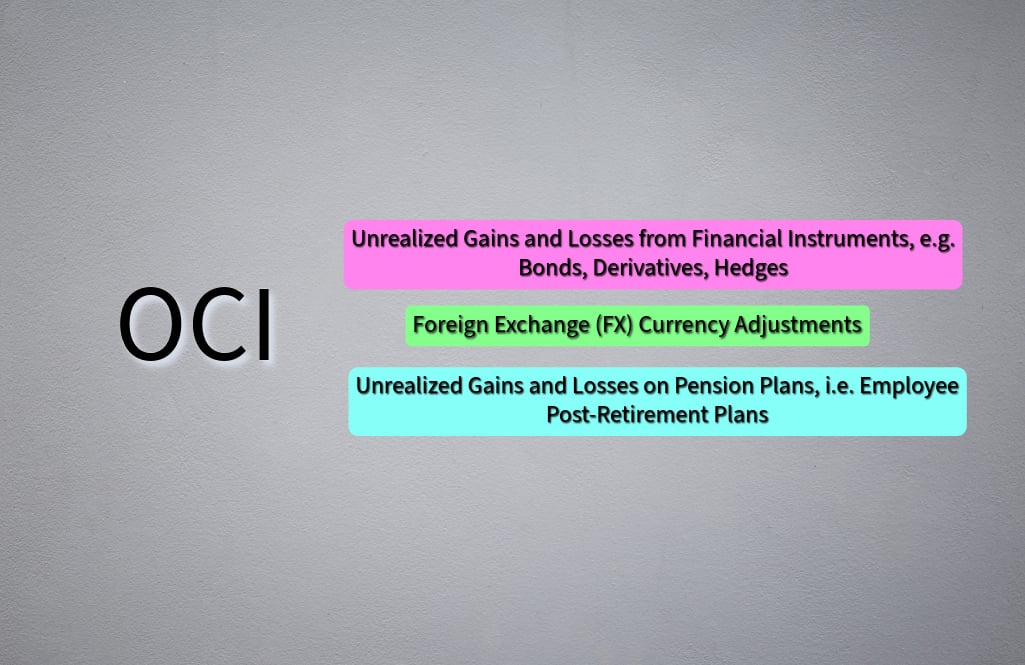

Inclusions in OCI

Common examples of items in OCI:

- Unrealized Gains and Losses from Financial Instruments, like Bonds, Derivatives, and Hedges.

- Foreign Exchange (FX) Currency Adjustments

- Unrealized Gains and Losses** on Pension Plans, such as Employee Post-Retirement Plans.

For instance, if a company holds a bond portfolio and its value fluctuates, the difference is recorded in the OCI line on the balance sheet.

Why? Because this gain or loss has yet to materialize, avoid any impact on the income statement or net income.

When the bond investment is sold, any profit or loss is saved in the income statement as non-operating income/expenses.

Common Examples of OCI

Certain investments, excluding loans and receivables, can be considered comprehensive income and must not be repaid.

Other instances of OCI include:

- The previously mentioned bond portfolio qualifies if not held to maturity. Changes in the value of the available-for-sale asset may be included.

- Foreign currency transactions can result in gains or losses, primarily affecting large firms in various currencies.

- Pension plans contribute to comprehensive income; increases in plan value can be recognized.

- Gains and losses from derivatives designated as cash flow hedges are part of OCI.

How to Calculate

If you’ve been wondering how to calculate OCI, here’s what you need to know:

Accumulated Other Comprehensive Income (AOCI): Balance Sheet Illustration

The image displays Amazon’s balance sheet for the fiscal year concluding in 2021, demonstrating OCI

Instead of using “Other Comprehensive Income (OCI),” Amazon utilizes the term “Accumulated other comprehensive income (loss),” a common practice since these two expressions are interchangeable.

Is OCI Included in Retained Earnings?

No, it is separate. Retained earnings represent the remaining funds after expenses and dividends.

Components of Other Comprehensive Income

OCI comprises revenues, expenses, gains, and losses excluded from net income.

Where to Find OCI on Financial Statements?

The income statement displays comprehensive income and OCI. The balance sheet shows AOCI within owners’ equity.

What is the Significance of Other Comprehensive Income?

If you’ve been wondering what is the significance of OCI, we’ll try to explain it the best:

Enhanced Financial Analysis

Other comprehensive income (OCI) plays a vital role in comprehensive financial analysis, offering a deeper evaluation of a company’s earnings and profitability, especially when dealing with defined benefit plans and derivatives.

While the statement of comprehensive income provides insight into profit or loss, OCI significantly enhances the reliability and transparency of financial reporting.

It became particular over fiscal years, where specific line items like defined benefit plans and derivatives are crucial for a comprehensive understanding of a company’s financial health.

Insights Beyond Day-to-Day Operations

The comprehensive income statement looks at daily operations, while OCI focuses on important items that give important information.

A company’s investment management is shown by using unrealized gains or losses. These gains or losses are indicators of the actual gains or losses that will be incurred.

Global Operations and Currency Impact

For globally operating firms, OCI illuminates the intricacies of foreign operations and helps evaluate the effects of currency exchange fluctuations.

This information is particularly beneficial for shareholders regarding their equity in the company.

Pension Liabilities and Financial Health

Moreover, OCI aids in assessing how future pension liabilities might affect unrealized profits, offering stakeholders a comprehensive view of the company’s financial health.

OCI is needed to analyze a company’s finances, showing overall performance and its effect on shareholders’ equity.

How to distinguish between P&L and OCI?

To understand P&L and OCI, it’s important to know the meaning of each item in financial statements. P&L takes centre stage as the primary indicator of financial performance, encompassing all income or expense items.

The decision to display something in OCI should be cautious. It should only be done if it enhances the comprehension of financial performance during the reporting period.

This choice can impact accumulated other comprehensive income (AOCI) in the shareholder equity section, particularly when considering realized gains.

To know a company’s financial health, evaluating when and how to include things in OCI is crucial.

Bottom line

OCI is a vital financial metric, enhancing transparency and offering deeper insights. It complements P&L statements, providing a comprehensive view of a company’s earnings and financial health.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.financebrokerage.com/other-comprehensive-income/

- :has

- :is

- :not

- :where

- 1

- 14

- 2%

- 2021

- 220

- 24

- 4

- 5

- 6

- 7

- 8

- 9

- a

- About

- Accounting

- Accumulated

- actual

- affect

- affecting

- After

- aids

- All

- Amazon

- an

- analysis

- Analysts

- analyze

- and

- any

- appear

- ARE

- AS

- assess

- Assessing

- asset

- At

- avoid

- awaiting

- Balance

- Balance Sheet

- BE

- Bear

- became

- because

- been

- beneficial

- benefit

- BEST

- between

- Beyond

- bond

- Bonds

- but

- by

- calculate

- CAN

- Cash

- cash flow

- cautious

- centre

- Changes

- choice

- clear

- combination

- Common

- company

- Company’s

- complete

- component

- components

- comprehensive

- comprises

- comprising

- considered

- considering

- content

- context

- contribute

- Corporate

- corporate finance

- crucial

- currencies

- Currency

- daily

- data

- day-to-day

- dealing

- decision

- deeper

- defined

- demonstrating

- Derivatives

- designated

- difference

- differentiate

- Display

- displays

- distinguish

- diverse

- dividends

- do

- does

- done

- due

- during

- dynamics

- each

- Earnings

- effect

- effects

- elements

- Employee

- encompasses

- encompassing

- Enhances

- enhancing

- Equilibrium

- equity

- especially

- evaluate

- evaluating

- evaluation

- eventual

- exactly

- examine

- example

- examples

- exchange

- excluded

- excluding

- expense

- expenses

- Explain

- expressions

- FASB

- finance

- Finances

- financial

- financial health

- Financial Instruments

- financial performance

- financial transparency

- Find

- firms

- Fiscal

- flow

- fluctuates

- fluctuations

- focuses

- For

- For Investors

- foreign

- foreign exchange

- found

- from

- funds

- future

- FX

- Gain

- Gains

- getting

- Give

- gives

- Globally

- guidelines

- Health

- hedge

- Held

- helps

- holds

- How

- How To

- http

- HTTPS

- if

- image

- Impact

- imperative

- important

- in

- In other

- include

- included

- includes

- Including

- Income

- Increases

- incurred

- indicate

- Indicator

- Indicators

- information

- insight

- insights

- instance

- instances

- instruments

- intentionally

- into

- intricacies

- investment

- investment portfolio

- Investments

- Investors

- involves

- issues

- IT

- items

- ITS

- jpg

- Know

- large

- liabilities

- like

- Line

- Loans

- LOOKS

- loss

- losses

- Main

- make

- management

- manages

- Market

- materialize

- maturity

- May..

- meaning

- means

- mentioned

- meticulously

- metric

- Metrics

- might

- multifaceted

- must

- Need

- needed

- net

- no

- None

- of

- offer

- offering

- on

- only

- operating

- Operations

- or

- Other

- over

- overall

- part

- particular

- particularly

- parts

- pension

- performance

- period

- plan

- plans

- plato

- Plato Data Intelligence

- PlatoData

- plays

- portfolio

- position

- potential

- practice

- previously

- primarily

- primary

- professional

- Profit

- profitability

- profits

- provides

- providing

- reaching

- realized

- recently

- recognized

- recorded

- redemption

- regarding

- reliability

- remaining

- Reporting

- represent

- represents

- requires

- result

- Reveals

- revenues

- Role

- sale

- saved

- Section

- separate

- serves

- shareholder

- Shareholders

- sheet

- should

- showing

- shown

- Shows

- significance

- significantly

- since

- sold

- something

- Sound

- Sources

- special

- specific

- Stage

- stakeholders

- standardized

- standards

- start

- Statement

- statements

- Status

- structured

- such

- table

- Takeaways

- takes

- term

- that

- The

- their

- These

- they

- things

- this

- thought

- tiny

- to

- tracks

- Transactions

- Transparency

- true

- try

- two

- Uncertain

- understand

- understandable

- understanding

- unique

- until

- using

- utilizes

- value

- various

- View

- vital

- Volatility

- vs

- W3

- Way..

- webp

- What

- What is

- when

- while

- will

- with

- within

- without

- wondering

- year

- years

- yet

- you

- zephyrnet