Internal audits play a crucial role in assessing a company’s internal controls, corporate governance, and accounting processes. These audits are essential for ensuring compliance with laws and regulations, as well as maintaining accurate and timely financial reporting and data collection. However, the traditional internal audit process is often time-consuming, redundant, and prone to reporting inaccuracies and errors.

To address these challenges and unlock operational efficiency, organizations are turning to internal audit automation. By harnessing the power of advanced technologies such as Robotic Process Automation (RPA), data analytics, and artificial intelligence, businesses can revolutionize their auditing procedures. The implementation of intelligence automation enables auditors to record, track, and monitor both quantitative and qualitative processes, leading to improved accuracy and quality.

As automation in internal audit continues to evolve rapidly, forward-thinking organizations are already embracing predictive models, RPA, and cognitive intelligence in conjunction with conventional analytics. Early adopters have witnessed significant improvements in risk intelligence, quality, and efficiency. Notably, Deloitte’s survey highlights a growing trend, with 43% of surveyed auditors already leveraging advanced analytics and automation in their internal audit functions.

The Institute of Internal Auditors’ 2022 North American Pulse of Internal Audit reveals that if CAEs had additional funds, 48% would prioritize increasing staff, while 25% would focus on technology. Interestingly, as funding sufficiency increased, the percentage choosing technology rose from 20% to 33%, but those opting for staff decreased from 61% to 31%. Among those investing in technology, data analytics software (68%) and audit management software (54%) were the top areas of interest.

Automation technologies for internal audit

Over the years, corporate accounting processes have been gradually integrated into large ERPs (Enterprise Resource Planning systems) and accounting software. However, auditors often utilize technology from various sources to perform verification, archiving, and extrapolating functions, resulting in repetitive and labor-intensive tasks that vary from one engagement to another. As a solution, a core set of automatable functions has emerged, leading to a reengineering of audit procedures that can be customized to suit different clients and partners. Today, the spectrum of internal audit automation software encompasses a wide array of digital technologies, ranging from foundational data integration and analytics to advanced cognitive elements mimicking human behavior. Some commonly used tools include the following:

Audit Management Software: This software helps streamline the entire audit lifecycle, from planning to reporting. It integrates data from various sources to provide a consistent and reliable information foundation for auditors. It allows auditors to manage audit schedules, allocate resources efficiently, and track audit progress in real-time. With a user-friendly interface, auditors can easily collaborate, assign tasks, and track the status of each audit. This automation solution centralizes audit-related data, facilitating seamless communication among team members and enhancing overall audit efficiency.

Data Analytics Tools: Predictive analytics utilizes software with predictive models, such as compliance risk models, to forecast future outcomes and identify potential risks. Data visualization software presents data in a visual context, using GRC (Governance, Risk, and Compliance) dashboards, enhancing understanding and analysis. Advanced data analytics software empowers auditors to swiftly analyze large datasets, enabling the identification of patterns, anomalies, and trends. This technology proves invaluable in detecting potential instances of fraud or non-compliance within the organization, providing deeper insights into business operations, and enabling data-driven decisions to strengthen risk management and compliance measures.

Robotic Process Automation (RPA): Robotic Process Automation (RPA) is a game-changer for internal audit automation. It involves the deployment of software bots to automate repetitive and rule-based tasks, such as data entry and report generation. RPA streamlines laborious processes, significantly improving accuracy and saving valuable auditor time. By relieving auditors of mundane tasks, RPA enables them to concentrate on more strategic and value-added activities, ultimately elevating the overall audit quality.

Artificial Intelligence (AI): AI is transforming the landscape of internal audit, empowering auditors with intelligent tools that revolutionize risk assessment, anomaly detection, and predictive modeling. Leveraging AI-powered solutions, auditors can analyze historical data to identify potential risks and prioritize their efforts effectively. The integration of natural language generation allows for structured data inputs to be transformed into seemingly unstructured narratives, streamlining reporting and analysis. Natural language processing enables the processing of unstructured data, such as text, facilitating data querying and the generation of structured information. Machine learning applications further enhance audit capabilities by continuously improving predictability and operational efficiency through data-driven insights. Ultimately, AI applications mimic human behavior, encompassing visual perception, speech recognition, decision-making, and language translation, facilitating the proactive identification of emerging risks and the implementation of preventative measures. This transformation enhances risk management capabilities and adds substantial value to organizations, propelling internal audit into a new era of efficiency and effectiveness.

Blockchain Technology: Blockchain technology offers significant advantages for internal audit, particularly in enhancing audit trail transparency and accuracy. By providing an immutable record of transactions and activities, blockchain ensures the integrity and authenticity of critical audit information. This technology bolsters the reliability of audit evidence, reinforcing the trustworthiness of the audit process and facilitating seamless verification of financial records and transactions.

Cloud-Based Solutions: Cloud-based solutions are invaluable for facilitating remote audits and seamless data sharing among audit teams. With secure storage and collaboration capabilities, cloud platforms enable auditors to access and work on audit-related information from anywhere, promoting flexibility and agility in the audit process. This technology empowers geographically dispersed audit teams to collaborate efficiently, fostering a cohesive and well-coordinated internal audit function.

Benefits of internal audit automation

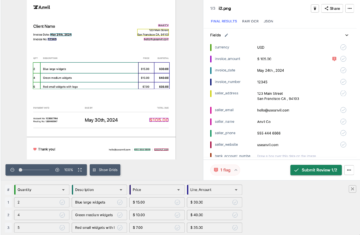

Automation in internal audit brings a myriad of benefits, enhancing efficiency and effectiveness in various aspects of the audit life cycle. One of the notable advantages is faster and more comprehensive data collection and cleaning. Whether for internal or external audits, auditors often gather evidence from diverse sources, such as process documents, invoices, system logs, or reports. Manual data collection from unstructured sources can be time-consuming and burdensome. However, with intelligent automation tools equipped with Natural Language Processing (NLP) and intelligent document processing technologies, auditors can automate tasks such as converting unstructured data into structured formats, performing calculations with extracted data, and combining data from different sources into a target file. As a result, auditors can review the entire population instead of just a sample, significantly reducing the time required for manual audits.

Another key advantage of automation of internal audit is better risk assessment. In addition to statistical analysis and visualizations, intelligent bots can employ machine learning algorithms to analyze gathered data and identify anomalies, such as potential fraud or suspicious IT logs, based on predetermined rules. By flagging these anomalies, auditors can focus on high-risk areas throughout the population, enabling more effective risk management.

Furthermore, AI-enabled bots continuously learn and adapt to datasets, improving the accuracy of anomaly detection over time. For example, researchers from Rutgers University implemented an RPA bot for a public accounting firm, which efficiently detected anomalies, including overstated loan amount balances in transactions.

Automation of internal audit also facilitates more frequent audits, as the reduction in manual work allows auditors to conduct audits at a higher frequency. This adaptability to the ever-changing business environment provides businesses with a higher level of assurance.

Intelligent bots can also contribute to continuous monitoring of determined controls in real-time, flagging issues for further examination by auditors. This proactive approach enables auditors to promptly address potential risks and ensure the organization’s adherence to compliance requirements.

How to get started with internal audit automation?

Getting started with internal audit automation involves a systematic approach to ensure a smooth and successful implementation. Here are the essential steps to initiate the process:

Step 1: Identify Automation Opportunities Begin by identifying processes and tasks within the internal audit function that are suitable for automation. Look for repetitive, rule-based, and time-consuming activities that can be streamlined through automation. Also, consider areas that require human judgment, as certain aspects of these processes can be automated while still involving human oversight.

Step 2: Define the Vision and Strategy Clearly articulate the vision for internal audit automation and define the strategy for its implementation. Understand the goals you wish to achieve through automation, whether it’s improving efficiency, accuracy, risk assessment, or providing more valuable insights to the organization. Communicate the strategy to all stakeholders, including audit teams, management, and IT.

Step 3: Build the Necessary Infrastructure To support automation, establish a robust infrastructure that includes the required technology, tools, and resources. Ensure that your team possesses the necessary skills and training to leverage automation effectively. Develop a governance framework that defines roles, responsibilities, and approval processes for automation initiatives.

Step 4: Choose the Right Automation Tools. Select the appropriate automation tools that align with your automation strategy and the specific needs of your internal audit processes. These may include robotic process automation (RPA), data analytics software, natural language processing (NLP), and artificial intelligence (AI) applications.

Step 5: Pilot and Test Automation Before fully implementing automation across all internal audit processes, conduct a pilot or proof-of-concept to test the selected automation tools in a controlled environment. This helps identify any potential challenges or adjustments needed for successful implementation.

Step 6: Monitor and Optimize Once automation is deployed, continuously monitor its performance and gather feedback from auditors and other stakeholders. Regularly assess the impact of automation on audit processes and outcomes. Identify areas for improvement and make necessary adjustments to optimize the automation’s effectiveness.

Step 7: Expand Automation Gradually As confidence and experience with internal audit automation grow, expand its implementation gradually to cover more processes and tasks. This phased approach allows auditors to adapt to the changes effectively while realizing the benefits of automation.

Conclusion

Internal audit automation stands as a transformative force within organizations, revolutionizing traditional audit processes and paving the way for enhanced efficiency, accuracy, and strategic insights. By leveraging advanced technologies such as robotic process automation, data analytics, artificial intelligence, and natural language processing, auditors can streamline repetitive tasks, gain deeper insights from vast datasets, and proactively identify potential risks. As internal audit teams embrace automation, they become well-equipped to focus on higher-value activities, contribute strategically to the organization’s success, and navigate the ever-changing business landscape with greater agility. The integration of automation technologies empowers internal audit to serve as a trusted advisor, ensuring robust risk management, compliance, and sound decision-making for a sustainable and competitive future.

FAQs

Can internal audits be automated?

Internal audits can be automated to a significant extent. Automation technologies such as robotic process automation, data analytics, artificial intelligence, and natural language processing (NLP) can streamline repetitive and rule-based audit tasks, enhance data analysis, and identify anomalies or potential risks. By automating these processes, internal audit teams can improve efficiency, accuracy, and audit coverage, allowing auditors to focus on higher-value activities and strategic decision-making. While complete automation may not be feasible for all aspects of internal audit, adopting automation technologies can significantly enhance the effectiveness and value of the audit function.

How is automation used in auditing?

Robotic Process Automation (RPA) can automate repetitive tasks like data entry and report generation, improving efficiency and accuracy. Data analytics tools utilize automation to analyze large datasets, identifying patterns and anomalies for risk assessment and fraud detection. Natural Language Processing (NLP) enables auditors to process unstructured data, like text, for easier querying and analysis. Additionally, Artificial Intelligence (AI) is employed for predictive modeling and anomaly detection, providing valuable insights. By leveraging automation technologies, auditors can optimize audit procedures, increase coverage, and focus on higher-value activities to deliver more strategic and valuable outcomes.

What are the 3 types of internal audits?

The three predominant types of internal audits are compliance audit, operational audit, and financial audit. A compliance audit entails inspecting and ensuring adherence to policies, laws, and regulations governing a specific area, process, or system under review. An operational audit primarily centers on evaluating internal controls in key processes to enhance productivity and efficiency. A financial audit is an unbiased assessment of an organization’s financial statements to verify their accuracy and fairness in representing the claimed transactions. The increasing prevalence of digital tools in business has led to the emergence of information technology audits. These audits involve examining management controls in IT applications, operating systems, databases, and infrastructure. They can be conducted independently for IT or in conjunction with compliance, operational, or financial audits. The aim is to ensure the integrity and efficiency of IT systems and processes, safeguarding data and optimizing IT resources in alignment with organizational objectives.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://nanonets.com/blog/internal-audit-automation/

- :has

- :is

- :not

- 1

- 12

- 13

- 24

- 25

- 7

- 75

- a

- access

- Accounting

- accounting software

- accuracy

- accurate

- Achieve

- across

- activities

- adapt

- adaptability

- addition

- Additional

- Additionally

- address

- Adds

- adjustments

- adopters

- Adopting

- advanced

- ADvantage

- advantages

- advisor

- AI

- AI-powered

- aim

- algorithms

- align

- All

- allocate

- Allowing

- allows

- already

- also

- American

- among

- amount

- an

- analysis

- analytics

- analyze

- and

- and infrastructure

- anomaly detection

- Another

- any

- anywhere

- applications

- approach

- appropriate

- approval

- ARE

- AREA

- areas

- Array

- articulate

- artificial

- artificial intelligence

- Artificial intelligence (AI)

- AS

- aspects

- assess

- Assessing

- assessment

- assurance

- At

- audit

- auditing

- auditors

- audits

- authenticity

- automate

- Automated

- automating

- Automation

- balances

- based

- BE

- become

- been

- before

- begin

- behavior

- benefits

- Better

- blockchain

- blockchain technology

- bolsters

- Bot

- both

- bots

- Brings

- business

- business operations

- businesses

- but

- by

- CAN

- capabilities

- Centers

- certain

- challenges

- Changes

- choosing

- claimed

- Cleaning

- clearly

- clients

- Close

- Cloud

- cognitive

- cohesive

- collaborate

- collaboration

- collection

- COM

- combining

- commonly

- communicate

- Communication

- company

- competitive

- complete

- compliance

- compliance measures

- comprehensive

- concentrate

- conclusion

- Conduct

- conducted

- confidence

- conjunction

- Consider

- consistent

- context

- continues

- continuous

- continuously

- contribute

- controlled

- controls

- conventional

- converting

- Core

- Corporate

- corporate governance

- cover

- coverage

- critical

- crucial

- customized

- cycle

- dashboards

- data

- data analysis

- Data Analytics

- data entry

- data integration

- data sharing

- data visualization

- data-driven

- databases

- datasets

- Decision Making

- decisions

- deeper

- define

- Defines

- deliver

- deloitte

- deployed

- deployment

- detected

- Detection

- determined

- develop

- different

- digital

- digital technologies

- dispersed

- diverse

- document

- documents

- each

- Early

- early adopters

- easier

- easily

- Effective

- effectively

- effectiveness

- efficiency

- efficiently

- efforts

- elements

- elevating

- embrace

- embracing

- emerged

- emergence

- emerging

- employed

- empowering

- empowers

- enable

- enables

- enabling

- encompasses

- encompassing

- engagement

- enhance

- enhanced

- Enhances

- enhancing

- ensure

- ensures

- ensuring

- Enterprise

- Entire

- entry

- Environment

- equipped

- Era

- Errors

- essential

- establish

- evaluating

- ever-changing

- evidence

- evolve

- examination

- Examining

- example

- Expand

- experience

- extent

- external

- facilitates

- facilitating

- fairness

- faster

- feasible

- feedback

- File

- financial

- Firm

- Flexibility

- Focus

- following

- For

- Force

- Forecast

- forward-thinking

- fostering

- Foundation

- Framework

- fraud

- fraud detection

- Frequency

- frequent

- from

- fully

- function

- functions

- funding

- funds

- further

- future

- Gain

- game-changer

- Gartner

- gather

- gathered

- generation

- get

- Goals

- governance

- governing

- gradually

- greater

- Grow

- Growing

- had

- Harnessing

- Have

- helps

- here

- high-risk

- higher

- highlights

- historical

- However

- HTML

- HTTPS

- human

- Identification

- identify

- identifying

- if

- immutable

- Impact

- implementation

- implemented

- implementing

- improve

- improved

- improvement

- improvements

- improving

- in

- include

- includes

- Including

- Increase

- increased

- increasing

- independently

- information

- information technology

- Infrastructure

- initiate

- initiatives

- inputs

- insights

- instead

- Institute

- integrated

- Integrates

- integration

- integrity

- Intelligence

- Intelligent

- Intelligent Automation

- Intelligent document processing

- interest

- Interface

- internal

- into

- invaluable

- investing

- involve

- involves

- involving

- issues

- IT

- ITS

- just

- Key

- landscape

- language

- large

- Laws

- Laws and regulations

- leading

- LEARN

- learning

- Led

- Level

- Leverage

- leveraging

- Life

- lifecycle

- like

- loan

- Look

- machine

- machine learning

- maintaining

- make

- manage

- management

- management software

- manual

- manual work

- May..

- measures

- Members

- modeling

- models

- Monitor

- monitoring

- more

- myriad

- narratives

- Natural

- Natural Language

- Natural Language Generation

- Natural Language Processing

- Navigate

- necessary

- needed

- needs

- New

- nlp

- North

- notable

- notably

- objectives

- of

- Offers

- often

- on

- once

- ONE

- operating

- operating systems

- operational

- Operations

- opportunities

- Optimize

- optimizing

- opting

- or

- organization

- organizational

- organizations

- Other

- outcomes

- over

- overall

- Oversight

- particularly

- partners

- patterns

- Paving

- percentage

- perception

- perform

- performance

- performing

- Phased

- pilot

- planning

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- Play

- policies

- population

- potential

- power

- Predictive Analytics

- presents

- primarily

- Prioritize

- Proactive

- procedures

- process

- Process Automation

- processes

- processing

- productivity

- Progress

- promoting

- propelling

- proves

- provide

- provides

- providing

- public

- pulse

- qualitative

- quality

- quantitative

- ranging

- rapidly

- real-time

- realizing

- recognition

- record

- records

- reducing

- reduction

- regular

- regularly

- regulations

- reliability

- reliable

- remote

- repetitive

- report

- Reporting

- Reports

- representing

- require

- required

- Requirements

- researchers

- resource

- Resources

- responsibilities

- result

- resulting

- Reveals

- review

- revolutionize

- Revolutionizing

- right

- Risk

- risk assessment

- risk management

- risk models

- risks

- Robotic

- Robotic Process Automation

- robust

- Role

- roles

- ROSE

- rpa

- rules

- Rutgers University

- s

- safeguarding

- saving

- seamless

- secure

- seemingly

- selected

- serve

- set

- sharing

- significant

- significantly

- skills

- smooth

- Software

- Software bots

- solution

- Solutions

- some

- Sound

- Sources

- specific

- Spectrum

- speech

- Speech Recognition

- Staff

- stakeholders

- stands

- started

- statements

- statistical

- Status

- Steps

- Still

- storage

- Strategic

- Strategically

- Strategy

- streamline

- streamlined

- streamlining

- Strengthen

- structured

- substantial

- success

- successful

- such

- sufficiency

- Suit

- suitable

- support

- Survey

- surveyed

- suspicious

- sustainable

- swiftly

- system

- Systems

- Target

- tasks

- team

- Team members

- teams

- Technologies

- Technology

- test

- that

- The

- The Landscape

- their

- Them

- These

- they

- this

- those

- three

- Through

- throughout

- time

- time-consuming

- to

- today

- tools

- top

- track

- traditional

- trail

- Training

- Transactions

- Transformation

- transformative

- transformed

- transforming

- Translation

- Transparency

- Trend

- Trends

- trusted

- trustworthiness

- Turning

- types

- Ultimately

- under

- understand

- understanding

- university

- unlock

- used

- user-friendly

- using

- utilize

- utilizes

- Valuable

- value

- various

- Vast

- Verification

- verify

- vision

- visualization

- Way..

- WELL

- were

- What

- What is

- whether

- which

- while

- wide

- with

- within

- witnessed

- Work

- would

- years

- you

- Your

- zephyrnet