Strong initial results trigger an

upgrade in S&P Global Mobility’s year-over-year forecast,

though economic and emissions headwinds remain.

Mainland China’s medium- and heavy-duty truck

production has surged strongly in early 2023, with double-digit

year-over-year growth seen in the February through April

period.

As a result, S&P Global Mobility has

increased its outlook for mainland China’s medium- and heavy-duty

truck production for 2023 by an additional 4 percentage points to

914,000 units, bringing the forecast year-over-year gain from 2022

to 26%.

The better-than-expected readings and low-base

effect are positive in supporting a solid near-term path to further

improvements in the truck manufacturing industry, but constraints

from both the demand and supply sides remain concerns.

The robust rebound was underpinned by the

broad-based recovery of the domestic economy following the

reopening from tough COVID restrictions and a continuous upturn in

truck exports that seemed to defy the challenging external economic

environment.

Speedy economic restoration unleashes

pent-up demand

Driven by the post-pandemic business resumption

and improved consumer confidence, household consumption, and

industrial output recovered at a fast clip entering 2023,

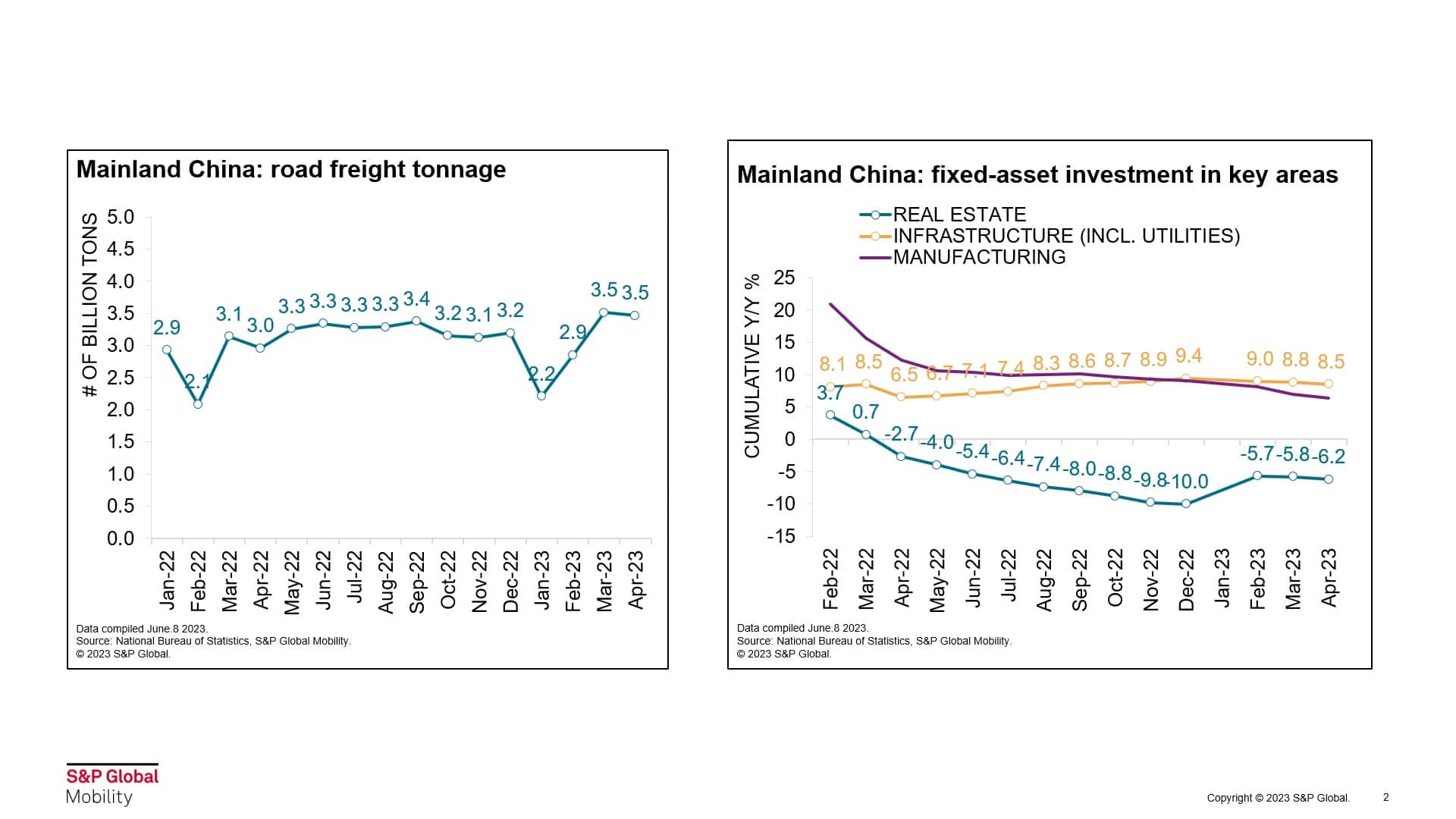

supporting the road freight sector to restart growth. This was seen

in the January through April period when the road freight tonnage –

which supports nearly 75% of domestic freight transport – rose by

8% from a year earlier.

At the same time, fiscal policies have remained

accommodative. Specifically, the local government special-purpose

bond quota, the main source of infrastructure investment, is set at

3.8 trillion yuan (approximately US$530 billion) for 2023 – higher

than the originally planned quota of 3.65 trillion yuan for 2022.

By the end of February 2023, more than 60% of the local government

special-purpose bonds had been pre-launched – compared with around

30% in the same period of 2022.

Under this frontloaded stimulus, infrastructure

investment (excluding utilities) expanded by 8.5% year-over-year

through April. Also, the property market started to show signs of a

restoration amid the ramp-up of bailout packages such as

mortgage-rate reductions, easing credit conditions for developers,

and loosening purchase restrictions for buyers.

With these circumstances, production of

tractor-trailer and construction trucks had a combined market share

of 60% in 2022 and surged by 50% year-over-year in the first four

months of 2023. Riding on this trend, S&P Global Mobility added

10,000 units to the May production forecast.

Booming exports provide a boost to

production

Mainland China’s medium- and heavy-truck

exports have entered a fast track since 2021 when pandemic-led

supply chain disruptions crimped overseas manufacturing activities.

With truck makers stepping up efforts in global expansion to

counter the domestic industry downturn, exports from Mainland China

have extended their rally into 2023 – increasing 57% to 97,000

units through April.

The headline growth was led by heavy

tractor-trailers, which more than doubled in export volumes from a

year ago. Supported by the government’s Belt and Road initiatives,

Southeast Asia, the Middle East, Africa, and South America have

remained core export destinations – with market share staying above

70% of total exports over the years.

In addition, exports to Russia and Mexico

became new bright spots in recent years. The exodus of Western

automakers from Russia since early 2022, in response to the

invasion of Ukraine, allowed Chinese brands to seize market share

in the Russian MHCV market. In the first four months of 2023,

exports to Russia continued explosive growth and amounted to 34,000

units, a level close to the entire 2022 total. The year-to-date

share of Chinese brands in the market has grown to nearly 60%.

Meanwhile, exports to Mexico recorded a

double-digit increase under the growing local demand for

construction trucks. In the coming months, the run rate of MHCV

exports is expected to hold steady, driving up the production

forecast by 20,000 units compared to our outlook released in

February.

Economic and emissions headwinds

remain

A potential future upgrade of our production

outlook is under assessment, with the domestic economic resurgence

building momentum. However, reaching the peak level of 2020 is

unlikely, as structural unemployment and still-tepid household

income prospects could blunt pro-growth measures’ ability to fully

materialize. Meanwhile, aggressive economic stimulus policies could

be restrained by the government’s fiscal de-risking, as well as

budget scarcity.

On the emissions front, although more cities

doubled down on the fight to remove CN4-compliant trucks from roads

starting in 2023, many areas lacked specific targets and subsidy

plans – curbing the effect of policies. In addition, despite the

healthy recovery of road freight transport, freight rates have

remained in depression, reflecting an oversupply of trucking. These

factors may lead truckers and fleet operators to postpone purchase

decisions or shift towards used trucks for cost-saving

purposes.

CHINA TO BECOME #1

LIGHT-VEHICLE EXPORTER THIS YEAR

CAN BRAZIL’S COMMERCIAL

TRUCK FLEET TURN ELECTRIC?

MHCV ALTERNATIVE

PROPULSION FORECAST

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/mainland-china-commercial-truck-production-starts-2023-with-a-.html

- :has

- :is

- :not

- ][p

- $UP

- 000

- 10

- 20

- 2020

- 2021

- 2022

- 2023

- 65

- 8

- a

- ability

- above

- activities

- added

- addition

- Additional

- africa

- aggressive

- ago

- allowed

- also

- alternative

- Although

- america

- Amid

- an

- and

- approximately

- April

- ARE

- areas

- around

- article

- AS

- asia

- assessment

- At

- automakers

- bailout

- BE

- became

- become

- been

- Billion

- bond

- Bonds

- boost

- both

- brands

- Brazil

- Bright

- Bringing

- broad-based

- budget

- Building

- business

- but

- buyers

- by

- Capacity

- chain

- challenging

- China

- chinese

- circumstances

- Cities

- Close

- combined

- coming

- commercial

- compared

- Concerns

- conditions

- confidence

- constraints

- construction

- consumer

- consumption

- continued

- continuous

- Core

- could

- Counter

- Covid

- credit

- decisions

- Demand

- depression

- Despite

- destinations

- developers

- disruptions

- Division

- Domestic

- doubled

- down

- DOWNTURN

- driving

- Earlier

- Early

- easing

- East

- Economic

- economy

- effect

- efforts

- Electric

- Emissions

- end

- entered

- entering

- Entire

- Environment

- excluding

- Exodus

- expanded

- expansion

- expected

- export

- exports

- external

- factors

- FAST

- February

- fight

- First

- Fiscal

- FLEET

- following

- For

- Forecast

- four

- freight

- from

- front

- fully

- further

- future

- Gain

- Global

- global expansion

- Government

- Growing

- grown

- Growth

- had

- Have

- headline

- headwinds

- healthy

- heavy

- heavy-duty

- higher

- hold

- household

- However

- HTML

- HTTPS

- improved

- improvements

- in

- Income

- Increase

- increased

- increasing

- industrial

- industry

- Infrastructure

- initial

- initiatives

- into

- invasion

- investment

- ITS

- January

- jpg

- lead

- Led

- Level

- local

- Local Government

- Main

- mainland

- mainland china

- Makers

- managed

- manufacturing

- manufacturing industry

- many

- Market

- May..

- Meanwhile

- measures

- Mexico

- Middle

- Middle East

- mobility

- Momentum

- months

- more

- nearly

- New

- of

- on

- operators

- or

- originally

- our

- Outlook

- output

- over

- overseas

- packages

- path

- Peak

- percentage

- period

- planned

- plans

- plato

- Plato Data Intelligence

- PlatoData

- points

- policies

- positive

- post-pandemic

- potential

- powerful

- Production

- property

- propulsion

- prospects

- provide

- published

- purchase

- purposes

- rally

- Rate

- Rates

- ratings

- reaching

- rebound

- recent

- recorded

- recovery

- reductions

- released

- remain

- remained

- remove

- response

- restoration

- restrictions

- result

- Results

- riding

- road

- roads

- robust

- ROSE

- Run

- Russia

- russian

- s

- S&P

- S&P Global

- same

- Scarcity

- sector

- seemed

- seen

- Seize

- separately

- set

- Share

- shift

- show

- Sides

- Signs

- since

- solid

- Source

- South

- South America

- Southeast Asia

- specific

- specifically

- started

- Starting

- starts

- steady

- stepping

- stimulus

- strongly

- structural

- subsidy

- such

- supply

- supply chain

- Supported

- Supporting

- Supports

- Surged

- targets

- than

- that

- The

- their

- These

- this

- though?

- Through

- time

- to

- Total

- tough

- towards

- track

- transport

- Trend

- trigger

- Trillion

- truck

- Trucking

- Trucks

- TURN

- Ukraine

- under

- underpinned

- unemployment

- units

- unleashes

- unlikely

- upgrade

- used

- utilities

- volumes

- was

- WELL

- Western

- when

- which

- with

- XML

- year

- years

- Yuan

- zephyrnet