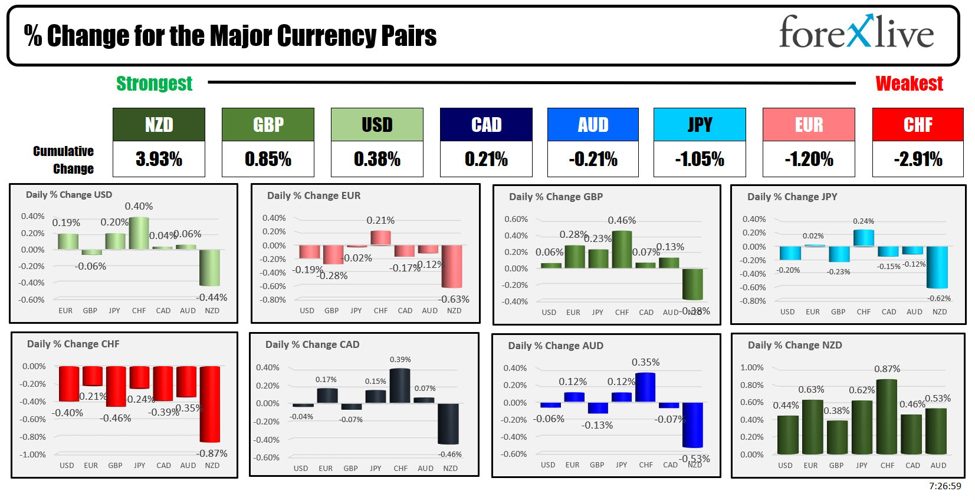

The strongest to weakest of the major currencies

As the North American session begins, the NZD is the strongest and the CHF is the weakest. The USD is mixed to higher with gains vs the CHF (0.40%), JPY (0.20%) and EUR (0.19%) and declines vs the NZD (-0.44%). The greenback is little changed vs the GBP, CAD and AUD.

The NZD is higher after the RBNZ rate decision

Cash Rate Projections:

- 5.61% in September 2024 (previously 5.6%)

- 5.54% in June 2025 (previously 5.33%) +21 bps

- 5.4% in September 2025 (previously 5.15%) +25 bps

- 2.99% in June 2027

The forecast for the cash rate in September 2025 is notably 25 basis points higher than the previous forecast.

Inflation Forecast:

- Inflation is expected to be 2.6% year-over-year by June 2025.

Statement Highlights:

- Monetary policy needs to remain restrictive.

- Restrictive policy has reduced capacity pressures and lowered consumer price inflation.

- Annual consumer price inflation is expected to return to the 1-3% target range by the end of 2024.

- The decline in inflation partly reflects lower prices for imported goods and services.

- Domestic services inflation components persist.

- Wage growth and domestic spending are easing.

- Weaker capacity pressures and an easing labor market are reducing domestic inflation.

Minutes Highlights:

- Members remain confident that monetary policy is effectively restricting demand.

- A further decline in capacity pressure is expected, supporting continued inflation decline.

- Interest rates need to remain restrictive for a sustained period to ensure inflation returns to the 1-3% target range.

- Annual headline CPI inflation is expected to return to the target band in the December quarter of this year.

- Domestic inflation has fallen more slowly than expected, with headline CPI inflation still above the target band.

- Interest rates may need to remain restrictive longer than previously anticipated to meet the inflation target.

- The committee discussed the possibility of increasing the OCR at this meeting.

Conclusion:

The RBNZ adopts a more hawkish stance, suggesting potential for later rate cuts and even the possibility of another rate hike. This reflects a commitment to maintaining restrictive monetary policy until inflation aligns with the target range

At the Reserve Bank of New Zealand (RBNZ) Monetary Policy Statement media conference, Governor Orr’s comments appeared less hawkish than the official statement. Key points from the Q&A session included:

- It will take time for domestic inflation to decline.

- The economy has a lower potential growth rate, though it’s unclear if this is temporary.

- There is limited room for inflation surprises on the upside.

- The RBNZ is pleased that inflation expectations are falling, but they need to decrease further.

- The Official Cash Rate (OCR) track is a central projection and not an absolute prediction.

During the press conference, the NZD/USD exchange rate declined, reflecting Orr’s less hawkish tone compared to the earlier statement.

NZDUSD retracing gains off the RBNZ rate decision

In the UK today, the CPI data was a disappointment. The MoM CPI rose by 0.3% vs 0.2% estimate, and the YoY fell to 2.3% from 3.2% last month but above the 2.1% expected. The Core CPI was much higher at 0.9% vs 0.7% estimate with the YoY up to 3.9% vs 3.6% estimate and 4.2% last month. Service inflation continues to be an issue. The first cut moved to November vs September before the CPI release.

In other news there were rumblings of a snap election being called in the UK.

Meanwhile, ECBs Rehn says there is a strong case for a ECB easing in June but not pre-commited on a rate path.

Today in the US, existing sales are expected to rise to 4.21M versus 4.19M last month. The EIA inventory is expected to show a drawdown of -2.547M barrels compared to a drawdown of -2.508M last month. Gasoline inventories are expected to show a drawdown of -0.729M. The private inventory data showed a surprise build of 2.48M oil inventories with gasoline also showing a surprise build of 2.088M:

Yields are higher. Stocks are mixed/lower with the Nasdaq up modestly and the S&P down modestly ahead of key Nvidia earning after the close. Yesterday, Ethereum continued to move higher on hopes of approval of an Ethereum ETF. Today the price is off of the high price from yesterday

A snapshot of the other markets as the North American session begins shows

- Crude oil is trading down $-0.66 at $78. At this time yesterday, the price was at $77.96

- Gold is trading down -$11.36 or -0.46% at $2409.43.. At this time yesterday, the price was higher at $2422.82

- Silver is trading down -$0.40 or -1.28% at $31.55. On yesterday the price surged to the highest level since 2012.At this time yesterday, the price was at $31.79

- Bitcoin currently trades at $69,993. At this time yesterday, the price was trading at $71,125.Ethereum is trading at $3690. Extremely high price extended to $3836

In the premarket, the snapshot of the major indices employed with futures are lower. Both the S&P and NASDAQ index closed at record levels yesterday. The Dow Industrial Average average backed off from its record close level earlier this week at 40,003.60

- Dow Industrial Average futures are implying a decline of -80.25 points. Yesterday, the index fell -196.82 points or -0.49% at 39806.76

- S&P futures are implying a decline of -6.7 points. Yesterday, the index rose 4.86 points or 0.09% at 5308.12

- Nasdaq futures are implying a decline of -1.80 points. Yesterday, the index rose 108.91 points or 0.65% at 16794.87

European stock indices are trading lower today in the morning snapshot:

- German DAX, -0.33%

- France CAC , -0.64%

- UK FTSE 100, -0.48%

- Spain’s Ibex, -0.26%

- Italy’s FTSE MIB, -0.27% (delayed 10 minutes).

Shares in the Asian Pacific markets were lower across the board:

- Japan’s Nikkei 225, -0.85%

- China’s Shanghai Composite Index, +0.02%

- Hong Kong’s Hang Seng index, -0.13%

- Australia S&P/ASX index, -0.05%

Looking at the US debt market, yields are little changed

- 2-year yield 4.871%, +3.8 basis points. At this time yesterday, the yield was at 4.832%

- 5-year yield 4.481%, +4.6 basis points. At this time yesterday, the yield was at 4.448%

- 10-year yield 4.453% + 3.9 basis points. At this time yesterday, the yield was at 4.431%

- 30-year yield 4.582%, +2.9 basis points. At this time yesterday, the yield was at 4.572%

Looking at the treasury yield curve spreads they are fairly steady:

- The 2-10 year spread is at -42.0 basis points. At this time yesterday, the spread was at -40.1 basis points.

- The 2-30 year spread is at -29.0 basis points. At this time yesterday, the spread was at -26.1 basis points.

In the European debt market yields in the benchmark 10 year yields are marginally lower:

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.forexlive.com/technical-analysis/the-as-the-na-session-begins-the-nzd-is-the-strongest-and-the-chf-is-the-weakest-20240522/

- :has

- :is

- :not

- ][p

- $UP

- 003

- 1

- 10

- 100

- 125

- 15%

- 2%

- 2012

- 2024

- 2025

- 225

- 25

- 26

- 36

- 4

- 40

- 5

- 55

- 6

- 66

- 7

- 8

- 80

- 9

- 91

- a

- above

- Absolute

- across

- After

- ahead

- Aligns

- also

- American

- an

- and

- Another

- Anticipated

- appeared

- approval

- ARE

- AS

- asian

- At

- AUD

- average

- backed

- BAND

- Bank

- barrels

- basis

- BE

- before

- begins

- being

- Benchmark

- board

- both

- build

- but

- by

- CAD

- called

- Capacity

- case

- Cash

- central

- changed

- chf

- Close

- closed

- comments

- commitment

- committee

- compared

- components

- Conference

- confident

- consumer

- continued

- continues

- Core

- CPI

- CPI data

- Currently

- curve

- Cut

- cuts

- data

- dax

- Debt

- December

- Decline

- Declines

- decrease

- Delayed

- Demand

- disappointment

- discussed

- Domestic

- dow

- down

- Earlier

- Earning

- easing

- ECB

- ECBs

- economy

- effectively

- EIA

- Election

- employed

- end

- ensure

- estimate

- ETF

- ethereum

- EUR

- European

- Even

- exchange

- Exchange rate

- existing

- expectations

- expected

- extended

- extremely

- fairly

- Fallen

- Falling

- First

- For

- Forecast

- from

- FTSE

- further

- Futures

- Gains

- gasoline

- gasoline inventories

- GBP

- goods

- Governor

- Greenback

- Growth

- Hang

- Hang Seng

- Hawkish

- headline

- High

- higher

- highest

- highlights

- Hike

- hopes

- HTTPS

- IBEX

- if

- in

- included

- increasing

- index

- Indices

- industrial

- inflation

- Inflation expectations

- inventory

- inventory data

- issue

- IT

- ITS

- jpg

- JPY

- june

- Key

- Kong

- labor

- labor market

- Last

- later

- less

- Level

- levels

- Limited

- little

- longer

- lower

- lowered

- maintaining

- major

- marginally

- Market

- Markets

- May..

- Media

- Meet

- minutes

- mixed

- mom

- Monetary

- Monetary Policy

- Month

- more

- morning

- move

- moved

- much

- Nasdaq

- Need

- needs

- New

- New Zealand

- news

- Nikkei 225

- North

- notably

- November

- Nvidia

- NZD

- NZD/USD

- OCR

- of

- off

- official

- Oil

- on

- or

- orr

- Other

- Pacific

- path

- period

- plato

- Plato Data Intelligence

- PlatoData

- pleased

- points

- policy

- possibility

- potential

- prediction

- press

- pressure

- pressures

- previous

- previously

- price

- Prices

- private

- Projection

- projections

- Q&A

- Quarter

- range

- Rate

- Rate Hike

- Rates

- RBNZ

- record

- Reduced

- reducing

- reflecting

- reflects

- release

- remain

- Reserve

- reserve bank

- Reserve Bank of New Zealand

- restricting

- Restrictive

- return

- returns

- Rise

- Room

- ROSE

- s

- S&P

- sales

- says

- September

- service

- Services

- session

- shanghai

- Shanghai Composite

- show

- showed

- showing

- since

- Slowly

- Snap

- Snapshot

- Spending

- spread

- Spreads

- Statement

- steady

- Still

- stock

- Stocks

- strong

- strongest

- Supporting

- Surged

- surprise

- surprises

- sustained

- Take

- Target

- temporary

- than

- that

- The

- the UK

- There.

- they

- this

- this week

- this year

- though?

- time

- to

- today

- TONE

- track

- trades

- Trading

- treasury

- Uk

- unclear

- until

- Upside

- us

- US Debt

- USD

- Versus

- vs

- was

- week

- were

- will

- with

- year

- yesterday

- Yield

- yield curve

- yields

- yoy

- Zealand

- zephyrnet