The data are clear: the sedan is dead. Or is it? S&P Global

Mobility registration and loyalty data support both sides of this

discussion. First, let’s look at the trends pointing to the sedan’s

demise.

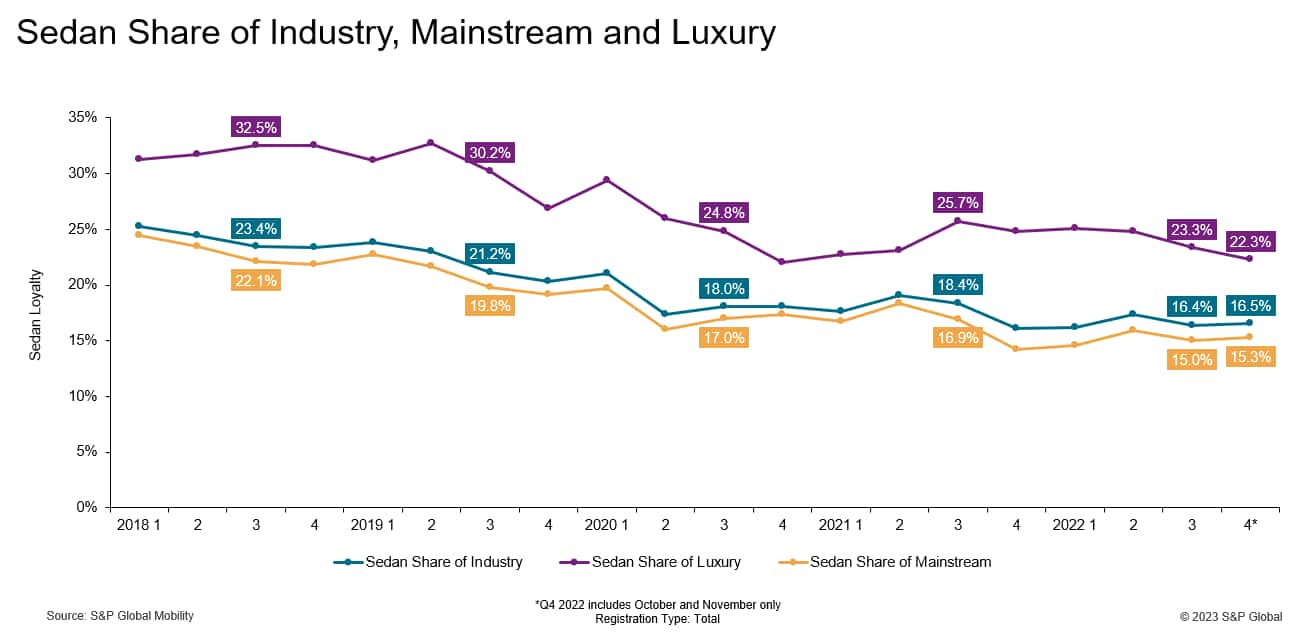

In Q3 2022, the latest quarter for which S&P Global Mobility

has complete data, sedan’s share of the U.S. market dropped to

16.4%, down two percentage points from a year ago and seven points

from four years ago (as a reminder, each percentage point is equal

to total annual Cadillac registrations to individual consumers).

Sedan share of luxury has declined at a faster rate, retreating

more than nine points over the past four years to 23.3% in Q3

2022.

Loyalty to the sedan body style also suggests its days are

numbered. As illustrated below, the percentage of return-to-market

(RTM) sedan households who acquire another one has fallen to 36% in

Q3 2022, down over seven percentage points from 43.6% four years

ago. And, again, luxury sedans have suffered more than mainstream

sedans: the percent of luxury sedan households that acquire another

sedan has fallen more than eleven percentage points to 35.5%. Just

in the past twelve months, luxury sedan loyalty has dropped more

than six points. From 2018 through the start of 2022, luxury sedan

loyalty had consistently been higher than industry or mainstream

sedan loyalty, but these metrics all merged in Q3 2022 and have

remained similar in October and November.

Third, the sedan’s loyalty decline has not only mirrored that of

passenger vans (whose market share November 2022 CYTD is 2.1%),

sedan loyalty has actually dropped at a slightly faster rate than

the van decrease. As shown below, the slope of the line indicating

sedan body style loyalty is a little steeper than the slope of the

passenger van line*, and the table on the right includes the data

supporting this finding (amazingly, the total six-year declines of

the two groups are remarkably similar to one another, with sedan

down 14.6 percentage points and passenger vans off 13.7

points).

Lastly, the number of sedan models on sale has dropped sharply

over the past four years to just 28 mainstream vehicles (only three

of which are from legacy domestic brands). Admittedly, the luxury

sedan count has remained steady, but bear in mind that the luxury

market accounts for only about 17% of the industry.

But there are at least two data sets suggesting sedans still

have some life left in them. First, a review of monthly sedan

loyalty since 2016 (see below) shows that sedan loyalty in the

first eleven months of 2022 has been going against the trend (of

the results in any of the other years) and is going up. November

2022 sedan loyalty of 37.4% was 2.7 percentage points higher than a

year ago.

Second, a closer look at sedan loyalty in just the two most

recent years, reveals that this metric’s pattern in 2022 has been

different from that a year earlier. Industry-wide sedan loyalty in

the January-November 2022 time period has been steady, in contrast

to the more uneven pattern a year ago.

Regardless of one’s opinion about the future of the sedan,

everyone is in agreement that this body style has been

marginalized. And, with this movement has come a similar decline in

couples and convertibles, which usually are derived from the

traditional sedan body style. But ingenuity remains alive and

kicking – we now are seeing more and more coupe derivatives of the

traditional sport utility body style (although convertible

utilities remain a work in progress).

*Passenger vans are used in this discussion, as opposed to

total vans, because the latter include vans used mostly for

commercial purposes.

—————————————————-

Top 10 Industry Trends Report

This automotive insight is part of our monthly Top 10

Industry Trends Report. The report findings are taken from

new and used registration and loyalty data.

The January report is now available, incorporating November 2022

CFI and LAT data. To download the report, please click below.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/the-sedan-debate.html

- 10

- 2016

- 2018

- 2022

- 28

- 7

- a

- About

- Accounts

- acquire

- actually

- against

- Agreement

- All

- Although

- and

- annual

- Another

- article

- automotive

- available

- Bear

- because

- below

- body

- Both Sides

- brands

- Cadillac

- clear

- closer

- come

- commercial

- complete

- Consumers

- contrast

- data

- data sets

- Days

- dead

- debate

- Decline

- Declines

- decrease

- Derivatives

- Derived

- different

- discussion

- Division

- Domestic

- down

- download

- dropped

- each

- Earlier

- eleven

- everyone

- Fallen

- faster

- finding

- First

- from

- future

- Global

- going

- Group’s

- higher

- households

- HTML

- HTTPS

- in

- include

- includes

- incorporating

- individual

- industry

- insight

- IT

- January

- latest

- Legacy

- Life

- Line

- little

- Look

- Loyalty

- Luxury

- Mainstream

- managed

- Market

- metric

- Metrics

- mind

- mobility

- models

- monthly

- months

- more

- most

- movement

- New

- November

- number

- numbered

- october

- ONE

- Opinion

- opposed

- Other

- part

- past

- Pattern

- percent

- percentage

- period

- plato

- Plato Data Intelligence

- PlatoData

- please

- Point

- points

- Progress

- published

- purposes

- Q3

- q3 2022

- Quarter

- Rate

- ratings

- recent

- Registration

- remain

- remained

- remains

- report

- Results

- Reveals

- review

- RTM

- S&P

- S&P Global

- sale

- sedans

- seeing

- separately

- Sets

- seven

- Share

- shown

- Shows

- Sides

- similar

- since

- Since 2016

- SIX

- Slope

- some

- Sport

- start

- steady

- Still

- style

- Suggests

- support

- Supporting

- table

- The

- The Future

- three

- Through

- time

- to

- Total

- traditional

- Trend

- Trends

- u.s.

- usually

- utilities

- utility

- Vehicles

- which

- WHO

- Work

- year

- years

- zephyrnet