Reading Time: 5 minutes

Introduction

BigCommerce Holdings (NASDAQ: BIGC), based in Austin, is an e-commerce SaaS (software as a service) platform. Its mission is to ‘help merchants sell more at every stage of business growth.’

The company was founded in 2009 in Australia by co-founders Eddie Machaalani and Mitchell Harper (who apparently met in a chat room in 2003). By 2014, the company received backing from firms such as General Catalyst, Revolution Growth and importantly, SoftBank (an early backer of Alibaba). Today, it has grown to about 600 employees and services approximately 60,000 online stores across 120 countries.

Description

Its ‘open SaaS’ platform allows for the creation and hosting of shopper-facing customer experiences as well as backend, business facing store management functionality:

For customers creating a new storefront, it offers 100 free and paid theme templates. These require no-coding experience and can be created using simple drag and drop features similar to those provided by Wix .

However, many merchants already have pre-existing storefronts that may have been created in, say, WordPress or Adobe. For these customers, it offers a ‘headless storefront’, which means it connects its back end functionality to the customer’s pre-existing storefront. This functionality is important as it has allowed the company to target larger merchants that may already use an agency to handle their online presence.

Additionally, the platform allows for free integrations into popular marketplaces such as Amazon and Ebay. Merchants can connect to these sales channels in order to access a deeper pool of customers or gain access to fulfilment networks such as Amazon FBA.

Importantly, the company aims to strategically partner, rather than compete, with leading SaaS providers in adjacent categories. For example, it would rather expose its platform to a third party API rather than compete head to head, with say, Shift4 Payments that provides payment processing (write up here) or Vertex that provides tax solutions for e-commerce (write up here). This is a slightly different approach to competitor Shopify that has put a strategic focus on Shopify Payments (which competes with third party payment processors).

In terms of its business model, the company generates revenue from two main sources:

- Subscription Revenues – these are generally charged per online store and dependent on the subscription plan. Subscription plans offered include:

- Standard Plan – its entry level plan for $29.95 per month

- Plus Plan – targeting merchants with up to $150,000 in sales, this costs $79.95 per month

- Pro Plan – targets merchants that want to scale up a business that might already be making $150,000 or more in sales. This costs $299.95 per month.

- Enterprise Plan – this targets customers with more than $1 million in sales. The pricing of this plan is tailored to the complexities of the merchant on an individual basis.

- Partner and Services Revenue – these are mainly revenue sharing agreements with its partners, technology integrations and partner marketing and promotion. As with any SaaS company, it also earns fees from educational services, solution architecting and implementation consulting.

A snapshot of the types of customers it has on its platform and range of industries is shown below:

Financials

Looking at the financials, total revenue for 2019 was $112 million of which approximately 74% were subscription revenues and 26% from partner and services revenue. Total revenue grew at a 22% clip between 2018-2019 and has increased to ~30% when comparing Q1 2020 to the year ago period. The acceleration in growth is mainly a result of increased demand for digital services that many companies have experienced as a result of COVID-19. Gross profit margins are a very healthy ~76% and even creeps up to ~79% when backing out stock based compensation.

Key Features of the IPO

-

- The IPO is expected to price tonight (Monday 3rd August) and begin trading on Tuesday 4th August. Its price range is between $18 and $20 per share.

- 6,850,000 shares of Series 1 common stock are being offered of a total 60,792,991 shares.

- In addition, there are 5,050,55 shares of Series 2 common stock. Series 1 and Series 2 stock are identical, except with respect to voting rights. The Series 2 are not entitled to a vote but can convert to Series 1 under certain circumstances.

- So, in total there will be 65,843,546 shares of Series 1 and Series 2 outstanding. Using the mid point of the range, this values the company at $1.25 billion.

- In addition, the underwriters have an option to purchase 1,027,500 shares of Series 1 common stock within 30 days.

- The company is expected to net about $117 million from the offering, of which it will use $16.4 million to pay off accumulated dividends on its Series F shares and the rest for working capital.

- The founders will retain a 10% beneficial ownership each, but the largest single shareholder will be General Catalyst Group that will own approximately 15.5% of the company.

Comparison to Shopify

There are a lot of parallels between BigCommerce and the wildly successful Shopify. Although Shopify is much larger today, Shopify was a similar size when it went IPO in 2015.

In the table below, I compare Big Commerce to Shopify at IPO and Shopify today:

| Metric | BigCommerce today | Shopify at IPO (’15) | Shopify today |

|---|---|---|---|

| No. of Merchants | 60,000 | 162,261 | 600,000 |

| Total Revenue | $112m (FY ’19) | $105m (FY ’14) | $1.58b (FY ’19) |

| Revenue Growth Rate (YoY %) | 29.6% (Mar’20 to Mar ’19) | 98.6% (Mar ’15 to Mar ’14) | 97.3% (Jun ’20 to Jun’19) |

| Gross Profit Margin | 76% (FY ’19) | 58.8%* (FY ’14) | 54.8% (FY ’19) |

| Share of subscription revenue | 74% (FY ’19) | 64% (FY ’14) | 40.7% (FY ’19) |

| ARR** | $137m (Mar ’20) | $89m (Mar ’15) | $565m (Jun ’20) |

| Sales and Marketing as a % of revenue | 54.1% (FY ’19) | 43.7% (FY ’14) | 30.0% (FY ’19) |

| R&D as a % of revenue | 38.5% (FY ’19) | 24.7% (FY ’14) | 22.5% (FY ’19) |

| Market Capitalisation | $1.25 billion | $1.27 billion | $129 billion |

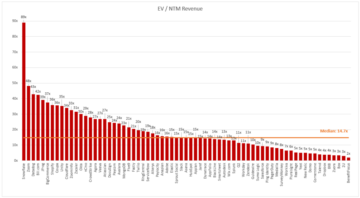

| Valuation (xTTM sales) | 10.4x (Mar ’20 to Mar ’19) | 10.2x (Mar ’15 to Mar ’14) | 62x (Jun ’20 to Jun ’19) |

** Shopify reports a monthly reoccuring revenue – figures here are multiplied by 12 to get an annual figure.

Shopify was relatively more attractive at its IPO compared to BigCommerce mainly from a revenue growth perspective. Additionally, the fact that it spent a lower share of its revenue on sales & marketing to achieve this growth compared to BigCommerce is impressive.

In terms of margins, BigCommerce has a higher gross margin (76% versus 58.8%) on a total level. However, this is due to the inclusion of Shopify payments that is a much lower margin business. (You can’t charge sky high margins for payment processing without antagonising merchants). Backing out the payment processing margins, gives a 74.8% margin for Shopify’s subscription business at IPO which is very similar to BigCommerce.

On the other hand, BigCommerce has a slightly higher ARR than Shopify at IPO, with a greater share of its revenue from subscriptions. (Again, the impact of payment processing revenues at Shopify).

Valuation and Conclusion

It appears that BigCommerce’s IPO valuation is remarkably similar to Shopify’s IPO back in 2015. Both were valued at approximately 10x trailing twelve month (TTM) sales and both at a market capitalisation of roughly $1.25 billion. This is odd, given the larger disparity in growth rates. This suggests that either BigCommerce is overvalued today or Shopify was undervalued at IPO. Looking at the recent performance of Shopify, it seems the market believes the latter was at least true. We’ll get the verdict on the former tomorrow.

On balance, there is a lot to like about the company and given the recent performance of SaaS companies, this one should do well.

- access

- Adobe

- agreements

- Alibaba

- Amazon

- api

- austin

- Australia

- Billion

- business

- business model

- capital

- channels

- charge

- charged

- co-founders

- Commerce

- Common

- Companies

- company

- Compensation

- consulting

- Costs

- countries

- COVID-19

- Creating

- Customers

- Demand

- digital

- digital services

- dividends

- Drop

- e-commerce

- Early

- eBay

- educational

- employees

- Experiences

- facing

- Features

- Fees

- Figure

- financials

- Focus

- founders

- Free

- General

- General Catalyst

- Group

- Growth

- head

- here

- High

- hosting

- HTTPS

- Impact

- inclusion

- industries

- integrations

- IPO

- IT

- leading

- Level

- Making

- management

- Market

- Marketing

- Merchant

- Merchants

- million

- Mission

- model

- Monday

- Nasdaq

- net

- networks

- offering

- Offers

- online

- online store

- Option

- order

- Other

- partner

- Pay

- payment

- payment processing

- payment processor

- payments

- performance

- perspective

- platform

- pool

- Popular

- price

- pricing

- Profit

- promotion

- purchase

- Q1

- range

- Rates

- Reports

- REST

- revenue

- SaaS

- sales

- Sales & Marketing

- Scale

- sell

- Series

- Services

- Share

- shareholder

- Shares

- Shopify

- Simple

- Size

- Snapshot

- SOFTBANK

- Software

- Solutions

- Stage

- stock

- store

- stores

- Strategic

- subscription

- successful

- Target

- tax

- Technology

- theme

- time

- Trading

- Valuation

- valued

- Versus

- Vote

- Voting

- within

- WordPress

- Yahoo

- year