Reading Time: 2 minutes

An update from a previous post on Rocket Companies that you can find: here

The company has had to significantly downsize its IPO by cutting both the price and the number of shares it is selling. It now plans to:

- Cut the price from $21 (mid point of the range it targeted) to $18.

- Cut the shares offered by 50,000,000. It now plans to offer 100,000,000 shares.

At $18 per share, the new implied valuation for the company is $35.7 billion, down approximately $6 billion from the valuation a few days ago.

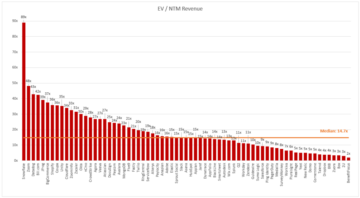

Despite signs of a frothy IPO market (such as a 200% increase in BigCommerce yesterday, write up here), it’s good to see the market differentiating between high quality offerings (such as Vertex, nCino, Shift4 Payments) and unappealing offerings (such as RackSpace Technology, Albertsons’ Companies and Casper).

A quick recap on reasons why I would avoid Rocket Companies (more detail here):

- A large part of its recent growth has been triggered by a refinancing wave and decreasing costs of home ownership which has been driven by falling rates. Given that many customers have already re-financed, the sustainability of this growth is questionable.

- It relies heavily on wholesale funding in order to originate loans from large banks. This type of funding is not as stable as, say, retail deposits. Sudden stops in liquidity, perhaps triggered from a crisis, can put the company in peril.

- The federal stimulus of $600 per week ended last week which has previously helped some borrowers remain current on their loans. This creates future uncertainty in terms of the demand for loan origination and to a much lesser extent credit risk on the loans it still warehouses on its books. (From the time the company originates a loan, it takes about 20 days for it to turn it around and sell it onto investors). This creates a window (albeit very small) for loans to deteriorate.

- The ownership structure is complicated (see diagram on previous post) and voting power concentrated in the hands of one person.

- Finally the proceeds of the IPO will be used to partially cash out existing shareholders rather than fund future growth. Although, this is fine and happens at many other IPOs that have gone on to be successful, it is the confluence of this fact and the timing of the IPO (which coincides with record origination levels) that is unappealing (at least to me).

If you have a different view and I’m missing something here, please comment below!

- around

- Banks

- Billion

- Bloomberg

- Books

- Cash

- Companies

- company

- Costs

- credit

- crisis

- Current

- Customers

- Demand

- detail

- driven

- Federal

- fine

- fund

- funding

- future

- good

- Growth

- here

- High

- Home

- HTTPS

- Increase

- Investors

- IPO

- IPOs

- IT

- large

- Liquidity

- loan

- Loans

- Market

- offer

- order

- Other

- power

- price

- quality

- range

- Rates

- reasons

- recap

- retail

- Risk

- sell

- Share

- Shares

- Signs

- small

- stimulus

- Sustainability

- Technology

- time

- Update

- Valuation

- View

- Voting

- Wave

- week

- wholesale