Reading Time: 5 minutes

Introduction

Vital Farms (NASDAQ: VITL) is a food company focusing on ethically produced dairy products . Its mission is “to bring ethically produced food to the table” by partnering with family farms in the United States.

The company was founded in 2007 by a husband and wife duo in Austin, Texas. The couple held a strong belief that a varied diet and strong animal welfare practices would lead to superior eggs. They started out selling their produce at local farmers markets, got discovered by Whole foods and began to scale a network of family farms. Today, it counts over 200 family farms within its network and its products are sold in more than 13,000 stores nationwide.

Description

The company offers 5 main products, all of which are pasture raised:

-

- Shell Eggs – this is the company’s first and most important product. These pasture-raised eggs purport to be healthier, more sustainable and even tastier by advocates compared to their cage-egged cousins. The company’s pasture eggs require each hen to have at least 108 square feet (appox. 10 meters) of outdoor space. This is a far cry from the minimum 2 square feet required for ‘free range’ hens, least of all caged hens.

-

- Butter – this is the second product the company launched and is highly complementary to shell eggs (the customers of both products overlap in terms of usage and profile). The pasture raised butter is sold in salted and unsalted varieties and contains 85% butterfat.

- Hard boiled eggs – this product was introduced to capture incremental demand from its main product, shell eggs. It aims to capture the ‘snacking market’ with products that are ready to eat.

- Liquid whole eggs – essentially eggs with the shell removed, which is popular for baking

- Ghee – a type of butter that originated in India. Similar to hard boiled eggs capturing incremental demand from shell eggs, ghee does the same from its butter offering.

With its products, the company aims to capture a share of the US natural food and beverage industry that generated total retail sales of approximately $47.2 billion in 2019. This market is growing at roughly a 6.4% CAGR and still only represents about 10% of the total food and beverage industry. This is sure to grow.

Closer to the company’s core offering, the US shell egg market accounted for $5.4 billion in sales in 2019. At the moment, according to SPINS LLC data, the pasture-raised retail egg market only accounts for $177 million in rales but is growing at an incredible 31.7% CAGR (between 2017-2019). This will likely to continue to capture share from the larger speciality egg market (which includes not only pasture raised, but also free-range and cage-free eggs) estimated at $1 billion in sales.

In terms of distribution the company uses three main channels:

-

- Natural Channel – where the company started, these include retailers like Whole Foods and Sprouts Farmers Market. This accounts for roughly 47% of retail sales, which is down from 52% in 2017

- Main Stream Channel – to increase reach, the company sells to Walmart, Target, Publix and their second largest customer, Kroger. The newly IPO’d Albertsons Companies (write up here) is also a customer. This channel was initiated in 2014 and is growing rapidly (now represents 53% of retail sales)

- Food Service Channel – this includes non-retail sales and represents only about 2% of net revenue.

Clearly with a company like Vital Farms, brand is of critical importance. As I learned on a recent podcast of ‘Invest like the Best‘, where Patrick O’Shaughnessy interviewed Kate Cole, brands ultimately live and die on two things 1) Relevance 2) Differentiation.

This is a relatively simple but powerful 2×2 matrix to assess the strength of a company’s brand. In terms of relevance (essentially is the product/service meaningful to customers?), Vital Farms scores high marks. It taps into the overall health and wellness trend and counts customers that are fiercely loyal (they are willing to pay up to 3x more compared to caged eggs). It also looks to have solved an access problem (a part of relevance) by opening and growing its mainstream channel. This is important because if customers can’t access the product easily, it doesn’t really matter how relevant it is.

The company is also very differentiated. It has strict standards in how it defines its pasture raised products (108 square feet versus 2 square feet for ‘free range’ hens). However, its farming techniques are largely the same techniques that were used before the industrial revolution. Meaning, it’s easy to copy and may introduce a number of upstarts that can quickly introduce the same standards (or even stricter standards) and gain a following. If the company loses its differentiation, it may also lose its pricing power and thereby its margins.

Financials

The company generated $140.7 million in sales as of 2019, which has grown by a CAGR of 37.9% between 2017-2019. That is impressive for a food company. It’s gross profit margins are also healthy at 30% in 2019, having grown from 25% in 2017. In the most recent quarter (March 2020) they have creeped up further still to 33% (although this includes some one-time pantry stocking effects). Despite its growth, it has also managed to be profitable in the past 2 years (albeit marginally).

Key Features of the IPO

-

- The IPO priced last night (30th July 2020) at $22 per share.

- A total of 5,040,323 shares are being offered by the company and 4,263,654 shares are being sold by the selling stockholders.

- In total there will be 39,175,767 shares outstanding, which at $22 per share, values the company at $862 million.

- The underwriters also have the option to purchase an additional 1,395,596 shares within 30 days.

- The company estimates it will net approximately $90 million from the offering. With a clean balance sheet (debt is only $10 million), it can use this money for expansion.

- The lead underwriters for the offering are Goldman Sachs, Morgan Stanley and Credit Suisse.

Valuation & Conclusion

There’s a lot to like about this company. It’s growing fast, will benefit from long multi-year trends (such as health and wellness), has solid margins and delivers a strong impact. Like Lemonade (see write up here), it’s also a Certified Class B Corporation, meaning it can consider wider stakeholder needs rather than only profit maximisation for shareholders. This helps lend credibility to the company when recruiting farmers into its network (who may worry that the price of their produce will be relentlessly pushed down year after year).

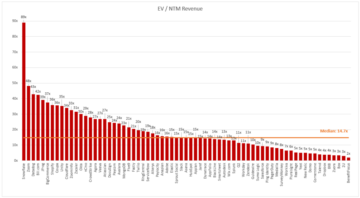

In terms of valuation, its is priced at 6.5 times 2019 sales or roughly 4.5 times projected 2020 sales (using a 37.9% growth rate). Certainly not cheap. But given its low penetration, strong tailwinds and optionality (it can potentially move into other dairy products in future), it should do well.

One to watch closely.

- access

- Additional

- austin

- BEVERAGE

- Billion

- brands

- CAGR

- channels

- Companies

- company

- continue

- Couple

- credit

- credit suisse

- Customers

- Debt

- Demand

- Diet

- discovered

- eat

- Eggs

- estimates

- expansion

- family

- farmers

- farming

- Farms

- FAST

- Features

- Feet

- First

- food

- future

- goldman

- Goldman Sachs

- Grow

- Growing

- Growth

- Health

- here

- High

- How

- HTTPS

- Impact

- Increase

- india

- industrial

- Industrial Revolution

- industry

- IPO

- IT

- July

- lead

- learned

- lemonade

- LEND

- LLC

- local

- Long

- Mainstream

- March

- march 2020

- Market

- Markets

- million

- Mission

- money

- morgan stanley

- move

- Nasdaq

- net

- network

- offering

- Offers

- Option

- Other

- Outdoor

- Pay

- podcast

- Popular

- power

- price

- pricing

- Produced

- Product

- Products

- Profile

- Profit

- purchase

- recruiting

- retail

- retailers

- revenue

- sales

- Scale

- Share

- Shares

- Shell

- Simple

- sold

- Space

- square

- standards

- stanley

- started

- States

- stores

- sustainable

- Target

- texas

- time

- Trends

- United

- United States

- us

- Valuation

- Versus

- Walmart

- Watch

- Welfare

- Wellness

- WHO

- whole foods

- within

- year

- years